If you’re looking for a reason why the Australian dollar is holding up in the face of the great iron ore crunch, European inflation is a good bet. It dramatically undershot expectations last night

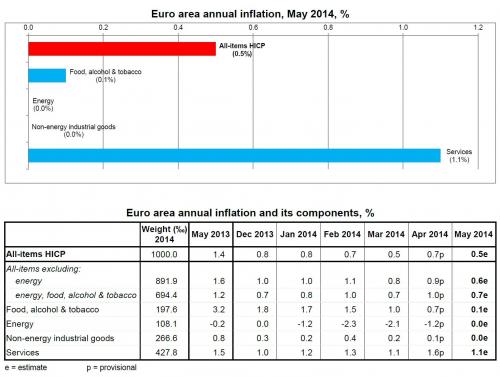

In recent months the ECB has been dismissing reports showing declining inflation in the Eurozone. Officials have been calling the situation “transient”. “Just wait until after Easter,” and all will be well… (see story). But today’s inflation report out of Germany shows that there is nothing transient about euro area’s disinflationary pressures.

The ECB has little choice but to act at this point, and unless we see “shock and awe” from the central bank, global markets will be quite disappointed.

Goldman has more:

Advertisement

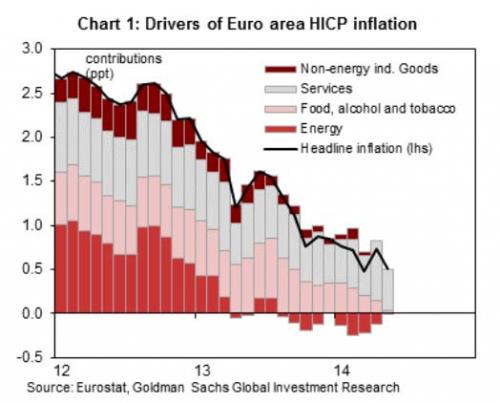

That is an entrenched trend and it is broad based:

Back to Sober Look:

Advertisement

On a related note, the chase for yield and the anticipation of fresh monetary stimulus in the Eurozone has created a rather distorted global rates environment. Spanish 5-yr government bond yield is now below the 5-yr treasury yield. Real (inflation-adjusted) yields in Spain are of course still higher than in the US. But just to put things into perspective, almost exactly 2 years ago Spain was staring down a potential collapse of its banking system and was actively seeking bailout funds (see post).

Once again, without a “show of force” from the ECB, this is not going to end well.

The Australian 5 year is yielding 3% offering spectacular carry from Europe. The Australian dollar threatened 93 cents again last night on the European inflation figure and if the ECB launches QE on Thursday more upwards pressure can be expected.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.