Consensus forecasts for earnings growth for the next financial year are too optimistic, reckon strategists at Bank of America-Merrill Lynch.

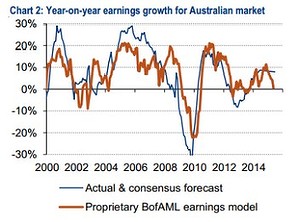

While “The Street” predicts around 10 per cent earnings per share expansion in FY15, the broker’s models suggests no EPS growth for the market (ASX 200) at all (see chart).

Consumer sentiment is a key input into BoA-ML’s model and “unless we see a rebound in sentiment there could be material downgrades ahead”, the analysts write.

Indeed, we’ve already seen some evidence of this just this morning, including footwear retailer RCG Corp and Funtastic this morning releasing profit warnings (the former explicitly blamed the budget), as well as Southern Cross Media on Friday.

The strategists “biggest concern” is the implicit margin expansion for many companies, given sales growth lags EPS growth estimates in many cases.

And they add the iron ore price to the list of worries.

Domestic cyclical earners are in for “a challenging period”, and they see “no compelling reason” to pile into miners, given the weak and weakening iron ore price.

So “where do you hide?” ask the strategists.

So for now the analysts favour yield plays – Telstra, Westfield and Transurban.

“Our highest conviction is that some US earners like QBE, ResMed and Bluescope will outperform for top-down and bottom-up reasons,” they write.

I said it all last year and I’ll say it again now: dollar-exposed industrials are the growth play for this cycle. Never more so than right now with the dollar miles above fair value and “unexpected” rate cuts looming.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.