The statistics of key cities and our forecasts for key developers both concluded that the physical market remained lackluster in May. Investors appear unlikely to see the expected rebound, which was anticipated following more local gov’ts fine-tuning policy & the PBoC’s supportive speech to first-home mortgage buyers. This aligned with our view that just a mild twist on policy rather than a comprehensive loosening “combo” can hardly resolve the challenges in the physical market now. Without a clear message from the central gov’t on a stance supportive of the property market, the wait-and-see attitude will prevail and powerful measures will be needed to prevent more slippage.

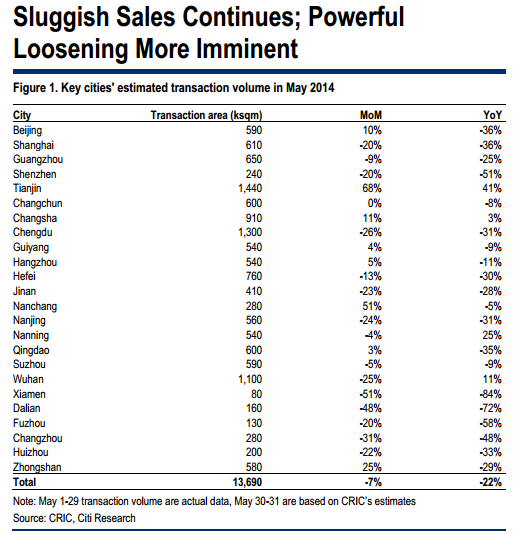

24 Key cities’ May sales declined 7%MoM: According to CRIC, the 24 key cities tracked recorded on average 7% decline MoM and 21% decline YoY in May’s sales. Although May is traditionally a lower season than Mar/Apr, given the weak Mar/Apr figures this year, a MoM sales decline in May is somewhat disappointing in our view. We believe many developers that previously held up the launches started to cut price but the impact is yet to be reflected. Among key cities (except Tianjin, Nanning, Wuhan, and Changsha which posted YoY gain), 20 cities recorded YoY decline, with Xiamen (-82%yoy), Dalian (-74%), and Fuzhou (-58%) the weakest.

…More loosening must be powerful and timely to catalyze any rebound: Thelack of notable improvement in May Sales suggests the physical market’s pressure could be even greater than the FY08/11 downcycle. To avert a potentially serious correction, powerful measures will need to be adopted in a timely fashion (in Jun/Jul), in our view, including 1) HPR relaxation – we expect more key cities (except Tier 1) to relax the HPR from now until Jun/July; 2) Credit easing – more favorable terms for mortgage costs/ down payments; 3) Improving buyers’ sentiment with less negative media reporting. We believe the sector to remain volatile in the short term driven by mixed news flow about price cuts and lackluster volume, while more policy loosening may be unveiled. Current valuation indicates the market’s expectations are seemingly low but the market’s assumption shall unavoidably turn down if the downtrend worsens.

Chinese authorities’ mettle is about to be tested, and our metal.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.