Deloitte has released a new report, which argues that Australians need to begin contributing an extra 5.5% to 7.5% of their salary to super if they are to enjoy a comfortable retirement. From The AFR:

Deloitte superannuation adviser Wayne Walker said it was important Australians not get too complacent about the compulsory retirement savings system, which now accounts for $1.8 trillion…

The ‘Adequacy and the Australian Superannuation system’ paper forecasts that 75 per cent of retirees will still be eligible for all or some of the aged pension in 20 years time.

Central to the improvements flagged by the paper was a recommendation that concessional contributions be amended from yearly limits to a lifetime cap.

It is astonishing that despite the tens-of-billions of dollars worth of budgetary concessions provided to super, that most Australians will still fail to save enough to fund their retirements and will instead fall back on the aged pension.

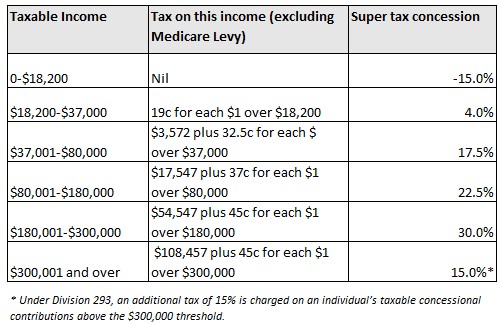

As argued many times before, a key failing of the Australian superannuation system is that concessions are very poorly targeted, with higher income earners receiving the lion’s share of concessions when they contribute to super, whereas lower income earners actually incur a tax penalty (see below table).

As noted by former federal Liberal leader, John Hewson, back in April:

As a result of this poorly targeted tax concession, 36.1 per cent of the benefits go to the top 10 per cent of income earners, whereas the bottom 10 per cent don’t receive any assistance at all, but are instead penalised…

Treasury estimates that from the combined support of superannuation tax concessions and the age pension, most people (about 80 per cent) receive around $270,000 support over their lifetime. In contrast, the top 1 per cent of male income earners receives about $520,000 support over their lifetime, because of significant tax concessions to high-income earners.

Accordingly, by providing massive taxation concessions to those on the highest incomes, the Budget is losing many billions of dollars of forgone revenue each and every year. Meanwhile, super is failing to relieve pressure on the aged pension, since those that are most likely to need it – lower and middle income earners – receive minimal concessions (or get penalised), which both hinders their ability to build-up a retirement nest egg and discourages them from making additional contributions.

Then there is the problem is that superannuation can be accessed well before the Aged Pension (i.e. tax free at 60) – a problem that will be exacerbated if the Pension access age is pushed-out to 70, but the superannuation access age remains the same.

And to add insult to injury, Australians are being gouged by excessive superannuation fees, which further hinders their ability to build up a retirement nest egg.

Rather than relaxing contribution limits – in turn providing another free kick to older higher income earners contributing to super – surely a better solution would be to address the distortions at the source, for example by providing everyone with the same superannuation concession (e.g. 15%), rather than skewing concessions towards the wealthy? This way, contributions would be lifted where it is most needed – for those at the lower end of the income scale – all the while reducing overall costs to the Budget.

Talk of increasing super contributions is pointless until the fundamental distortions afflicting the system are fixed. Of course, this won’t stop the rent seekers in the financial services industry continuing to advocate policies that further feather their own nests.