As summarised by Houses & Holes earlier, the Australian Bureau of Statistics (ABS) today released the national accounts for the March quarter, which registered a 1.1% increase in real GDP over the quarter and a 3.5% rise over the year. The result smashed market expectations for 0.8% growth over the quarter and 3.1% growth over the year.

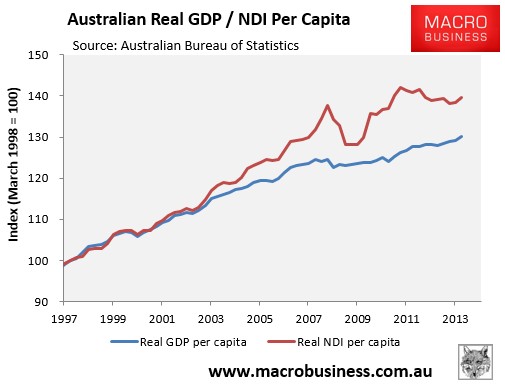

On a per capita basis, however, real GDP increased by 0.7% and by 1.8% over the year. Further, real national disposable income per capital rose by 0.9% over the quarter and 0.4% over the year.

According to the ABS, seasonally adjusted growth for the quarter was driven by:

- a 1.4% contribution from net exports;

- a 0.3% contribution from final consumption expenditure;

- a 0.2% contribution from Private gross fixed capital formation; partly offset by

- a 0.6% change in inventories.

Over the year, Mining (0.9 percentage points) and Financial and insurance services (0.2 percentage points) and construction (0.2 percentage points) were the largest contributors to growth.

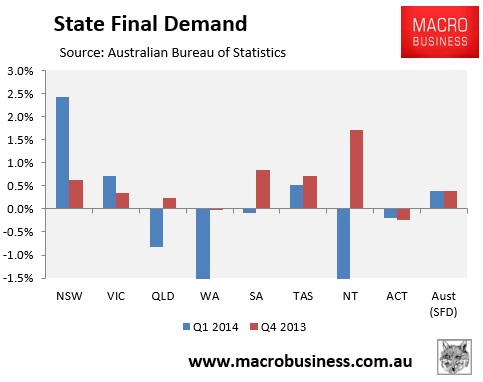

Results were mixed at the state and territory level, with final demand growing strongly in the New South Wales (2.4%) and solidly in Victoria (+0.7%) and Tasmania (+0.5%), but falling in Queensland (-0.8%), Western Australia (-1.5%), South Australia (-0.1%), the Northern Territory (-6.5%), and the ACT (+0.2%). Final demand nationally was also quite soft, coming in at just 0.4%.[Note: state final demand does not include exports, so is markedly different to GDP]:

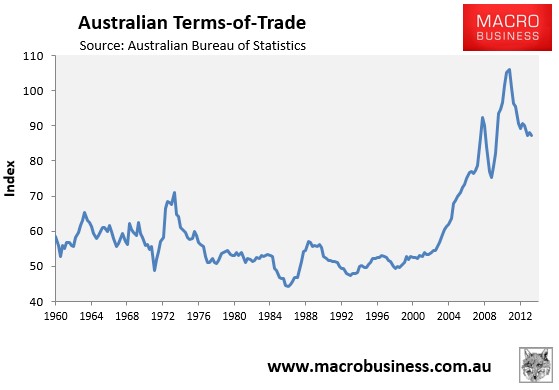

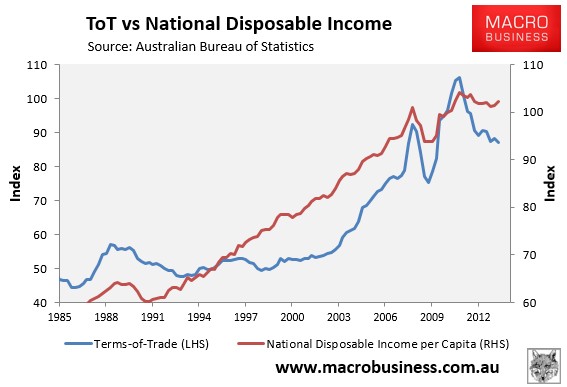

The terms-of-trade fell by a seasonally-adjusted 1.2% over the quarter and by 3.9% over the year:

Curiously, the falling terms-of-trade did not drag on income growth, with real per capital national disposable income (NDI) rising by 0.9% over the quarter, beating the 0.7% rise in per capita GDP over the quarter.

Nevertheless, given the ongoing large falls in commodity prices (particularly iron ore) since the March quarter, income growth is likely to slump over the June and December quarters, particularly as contract prices are adjusted downwards, and will continue to be weak as long as the terms-of-trade unwinds from its current very high level (see below charts).

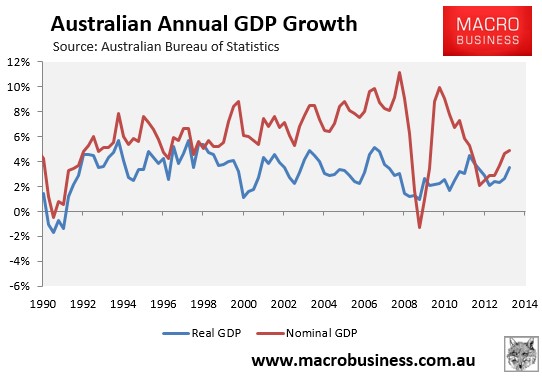

The rise in national disposable income helped nominal GDP to rise strongly, which is a positive for government finances:

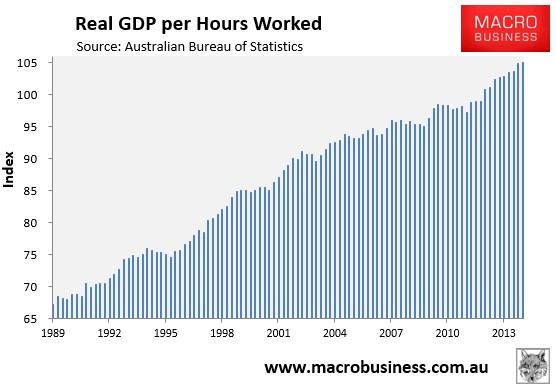

Real GDP per hour worked also rose by 0.2% over the March quarter and was up 2.1% over the year, suggesting improved labour productivity as the structural adjustment under way continues to create greater efficiencies in the weaker sectors:

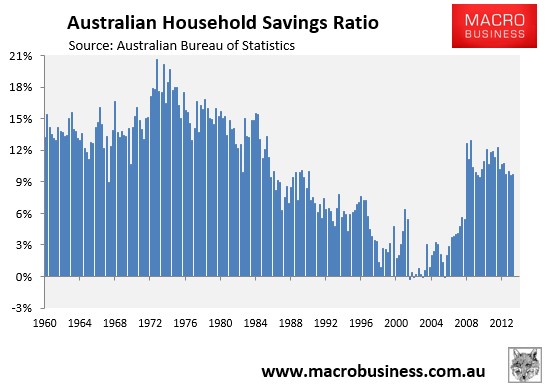

Finally, the household savings ratio rose marginally over the quarter to 9.7% from 9.6%:

Overall this is a strong result, with headline GDP recording a pick-up in growth, and both real per capita GDP and NDI improving.

The real test is ahead, however, with recent sharp falls in commodity prices (particularly iron ore) likely to drag down per capita NDI in the June and September quarters – a trend that is likely to continue as the terms-of-trade retraces back towards its long-run average.

Moreover, the upcoming expected falls in mining capital expenditures will provide headwinds to growth over coming years, which will likely keep headline GDP below its longer-term trend, and ultimately at an insufficient level to prevent unemployment from rising, despite rising net exports. There is also the recent hit to consumer sentiment following the Budget, which if maintained could stifle consumption and the nascent housing construction mini-boom.

unconventionaleconomist@hotmail.com