by Chris Becker

No this article is not about calling a market top – its just revealing an inconvenient truth.

The share market is not a place for investing – i.e. somewhere to get a return ON and OF your savings – its a speculators paradise. The main reason?

The shares that are being exchanged already exist – it’s a secondary market. This point is often lost on most analysts and spectators. The share market is just like the housing market, where a mere fraction of exchanges are purchase of new stock through IPOs or secondary issues, hence speculation turns to ascertaining the value of existing stock.

Indeed in recent years the net equity raisings on the ASX have been pathetic, mainly just financial:

While the timeframes are different between houses and shares, the inputs, sentiments, role of the credit impulse/margin lending etc, “high frequency trading” or “flipping” are the same. It’s humans ascertaining how much they reckon another human will pay for an already existing thing.

In and of itself, having volatile markets is no bad thing. In fact, its how I make my living, speculating each day on the directions and levels of securities, mainly foreign exchange but also shares. Indeed, its been a great strategy for many, particularly in rampant bull markets. But as I’ve shown before, get the timing wrong on your entire “investment” portfolio – and its all been for nought.

The problem is not about protecting individuals from having a punt – it’s when whole institutions, government policies and an entire cohort of society – i.e those saving for and in retirement – conflate this speculation with investment.

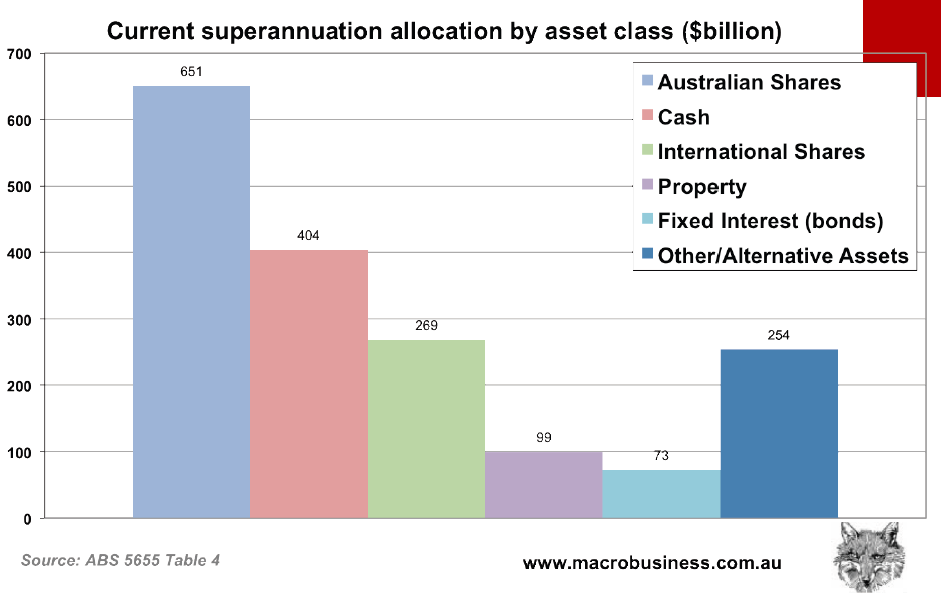

I’m looking at you, the Australian $1.84 trillion superannuation sector.

I’ve argued for a long time that the exposure to stocks (mainly Australian stocks) within superannuation funds is far too high, alongside an obscene amount of idle cash and far too low exposure to bonds, which are actual investments:

A cracking read at the FT highlights the differences between bonds and stocks and asks the question about why the former is considered dull:

Both equities and bonds promise regular future payments to the holder, and in the short term, contractual payments on bonds (interest coupons, principal) are much more predictable than discretionary payments on equities (dividends, buybacks)

So what makes bonds seem dull and equities exciting?

First, because economies are unstable in the short term, the same is true of earnings and dividends/buybacks. Second, individual companies have wildly different prospects. Third, by having different maturities, the bond market has an “inductive anchor chain of reference”: bonds are priced with reference to others of shorter maturity. Fourth, equities, unlike most bonds, are perpetual, and when yields are low, simple maths shows that price fluctuations for a given yield shift are vastly magnified.

Faced with a myriad discretionary dividend streams that are volatile in the short run, and without an anchor chain, all but the most patient equity investors give up on the longer term. They fall back on forecasting 18 months ahead at most, speculating on events in that timeframe or simply on momentum. In comes the craziness.

Indeed. The rest of the article points to an interesting potential solution and may have merit when the biggest shareholder – baby boomers – demand steady income, not double digit capital growth.

The craziness actually may not be in the market structures, but the almost total lack of risk management. There is nothing wrong with having over half of your portfolio in shares, IF you understand and realise the risk involved and have some modicum of tools (time stops, index filters, technical stops, correlation filters, profit targets, etc) at your disposal. Oh, and the guts to implement them when the fertilizer hits the ceiling fan.

For the individual, the usual management is hope and pray for another rally to get back to break even. For fund managers, it’s wait for the next quarterly superannuation contributions to flood in and ticket clip, and if it gets real tough, goose your local central bank into easing rates and do some bond swaps. For the speculators, we’ve already moved on to the next trade and hope the craziness continues.

The real answer to “the shares must be crazy” is who needs investments in a world with zero interest rates and equities to the moon?