Chris Richardson from Deloitte-Access Economics has penned an interesting article in The AFR explaining why the Budget has turned from a perennial ‘good news story’ during the 2000s to a ‘bad news story’ now, despite the economy seemingly being in reasonable health.

Essentially, Richardson argues that the federal government took the revenue windfall from a temporary commodity price boom and blew it on a raft of permanent promises aimed at families, pensioners and wage earners, in turn creating a large structural Budget deficit:

The resources boom of the past decade was good for the economy, but stunningly good for the budget. That’s because the boom:

- Pushed up commodity prices… in turn sending profits soaring. And profits are the most heavily taxed bit of our incomes.

- Pushed up sharemarkets and underpinned earlier gains in housing prices, with those capital gains also turbocharging the tax take.

- Encouraged families to spend, thanks to higher wealth resulting from healthy share and housing prices, boosting spending taxes…

Yet coal and iron ore prices peaked back in 2011, and capital gains remain elusive…

The bonanza delivered by the economy to the budget has gone… it turned out to be temporary.

…the nation’s politicians – both sides – took the temporary boom of the past decade and spent it all on an orgy of permanent promises such as family benefits and income tax cuts.

I have long argued the same essential points and firmly believe that without fundamental reform to both taxation and expenditure policy, the Australian Budget will remain in deficit for decades to come.

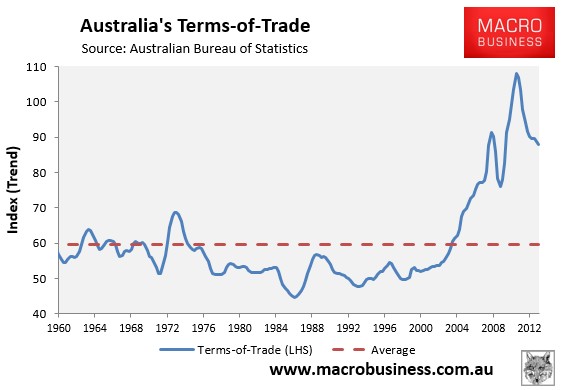

The fact is, the surpluses achieved during the Howard Government were due mostly to extreme good luck, rather than sound fiscal management. Budget revenues ballooned under the Howard Government, who presided over the most lucrative part of the resources boom when commodity prices and the terms-of-trade exploded (see next chart), not to mention rapidly rising household debt.

The next chart tells the story. Nominal GDP is the dollar value of what’s produced and earned across the economy and is also the measure that drives federal taxation revenue. Due in part to the inexorable rise in the terms-of-trade, the Howard Government experienced ever growing nominal GDP growth as commodity prices surged, whereby it reaped the benefits of growing personal and company taxes, not to mention increased capital gains taxes as asset markets boomed.

However, as pointed out by Richardson, much of this temporary revenue windfall was wasted. First by the Howard Government, via ballooning entitlement spending aimed at middle class families, the aged, and wealthy retirees, not to mention generous tax breaks granted for superannuation. Then augmented by the Rudd and Gillard Governments.

Now Australia faces a prolonged period where the terms-of-trade will likely trend down towards its historical norm (see next chart), crimping the nation’s disposable income and reducing the personal and company tax tax.

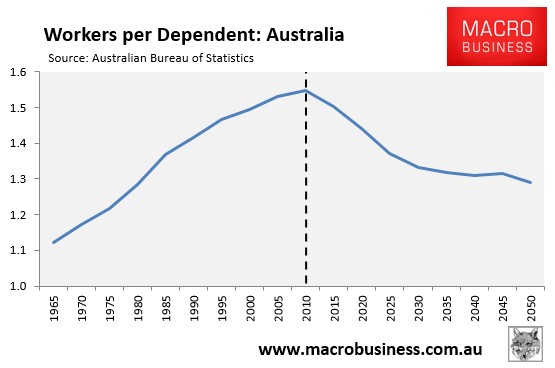

Added to this, demographic headwinds are building as the large baby boomer cohort retires, leaving a shrinking pool of workers to collect taxes from and rising bills for health and age-related welfare (see next chart).

Gone are the good old days of happy Budgets and widespread giveaways, soon to be replaced by an annual program of cutbacks and tax increases.

unconventionaleconomist@hotmail.com