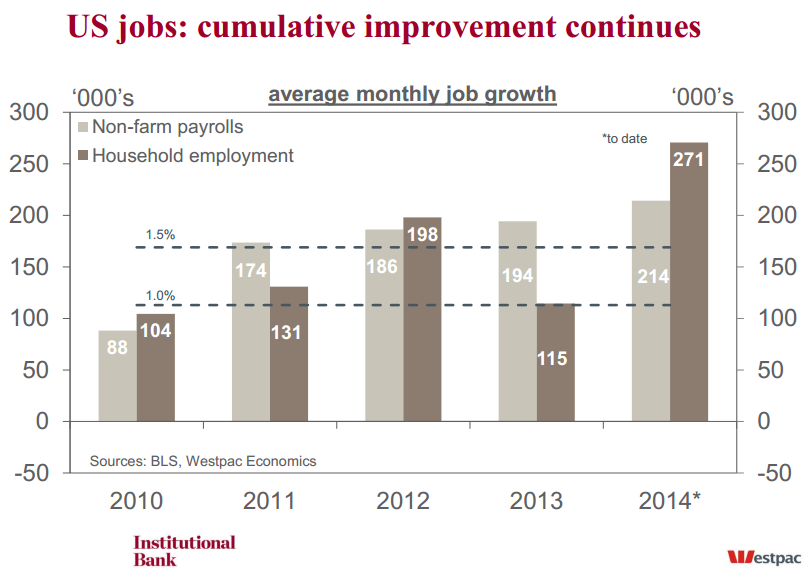

Friday’s employment report certainly got the market’s attention. April’s 288k increase in nonfarm payroll employment was well above the market expectation of 192k. What’s more, as has typically been the case recently, the previous two monthly outcomes were also revised up by 36k. The net result is that the past three months have all reported gains of over 200k. For the year to date, the monthly average pace stands at 214k, 10k more than 2013. Albeit marginal, the rise in the monthly-average pace of payroll job creation will be welcomed by the FOMC, particularly after the very poor Q1 GDP outcome. The April result leaves the level of non-farm payrolls just 27k below its pre-recession peak, reached in February 2008.

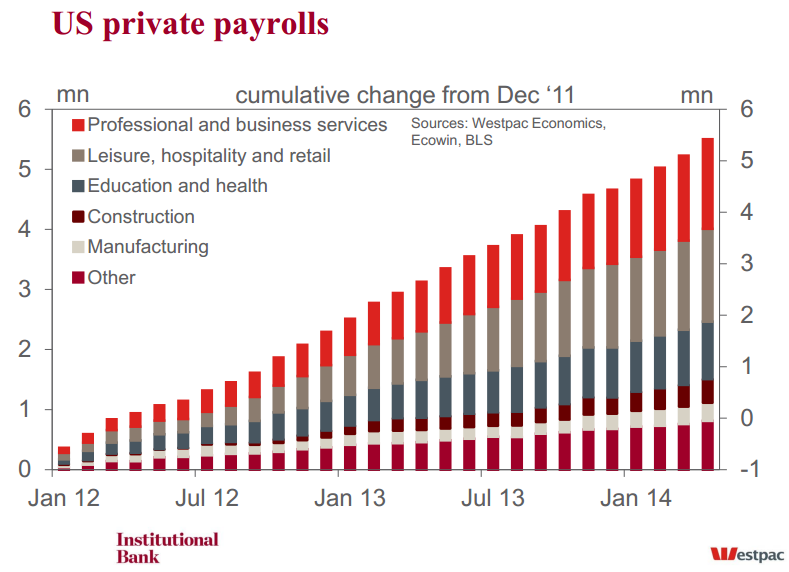

Relative to 2013, so far in 2014, job creation continues to be driven by professional & business services (65k per month from 56k in 2013; a third of which are temporary positions), leisure & retail (39k per month from 67k in 2013), and education & health (31k from 28k per month). At the margin, construction has improved (31k per month from 13k in 2013), despite the weather.

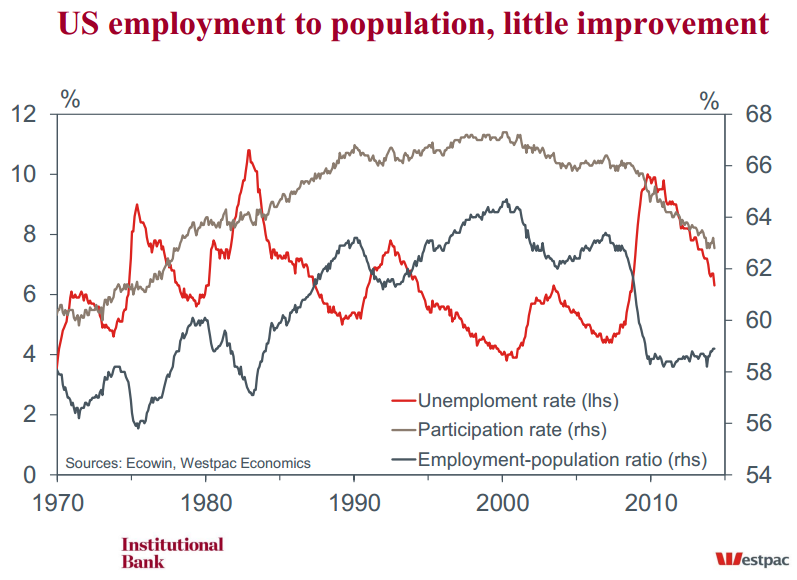

The other side of the employment report also provided a strong headline, with the unemployment rate falling from 6.7% to 6.3% in April. At that level, the unemployment rate is below the upper threshold that the FOMC previously had said would trigger discussion of an increase in the Fed Funds rate – this was before the introduction of the qualitative guidance framework in March.

The curious thing about the household survey result was that the fall in the unemployment rate was not driven by job gains, but rather by people leaving the workforce. Specifically, in April, the household survey reported the loss of 73k jobs and 733k unemployed. As such, 806k individuals chose to leave the workforce in one month.

This outcome is not a complete surprise. We have, on many occasions, highlighted the persistent downtrend apparent in the participation rate over the past few years, in part due to the ageing population. Further, we have also noted that an abrupt drop in participation in early 2014 was a risk owing to the expiry of long-term unemployment benefits, first introduced in the wake of the GFC. No longer qualifying for financial help, and seemingly unable to find another position, many individuals have decided to stop looking for work.

If the detached workers were all nearing retirement age, then the flow-on impact on aggregate demand could be buffered by their existing stock of assets and any potential pension. But, as highlighted by the detail of the household survey, this is not the case. Yes the ageing of the population is weighing on the participation rate, but there is also a very clear (negative) cyclical story impacting prime-aged workers and youth.

While we had seen an improvement in participation among the 16-to-24 age group in recent months, the gains were reversed in April as this group’s participation rate fell back to be near its historic low. This is also true of the 25-to-34 and 35-to-44 age groups, both of which continue to see record-low levels of participation. For 45-to-54 year olds, participation is a little above its 2013 low, but still well below pre-GFC levels. All told, the attachment of workers to the labour force is much weaker in the current period than has historically been the case.

Part of the reduction in participation amongst the young is likely a result of more time spent in education, but the lack of jobs growth for this group in recent months clearly points to demand remaining an issue. So far in 2014, 48% of the total growth in jobs across all age groups has occurred for those aged 55 and older. The balance of the job creation has been equally split between those aged between 25 and 54. This is a stark contrast to the latter part of 2013 when we finally began to see some reversal of GFC-induced decline in prime-age and youth employment, with 71% of available jobs going to those aged between 16 and 34.

All told, the April employment report does give a strong signal on the state of the US economy, albeit one that is not one dimensional. There is clearly solid momentum in aggregate job creation. However, whether many of these jobs can be relied upon to build a career is an open question. Young and prime-aged workers are clearly finding making headway in the labour market difficult. And, of the jobs in retail & leisure, education & health and professional & business services, many are lower-paid support and administrative positions which hold little (if any) chance of career progression. In contrast, IT and financial services (industries which have typically provided higher wages and career progression) have seen only minimal job creation over the past 16 months. On the whole, what we are currently seeing is an economy in which immediate needs are the focus, not the nation’s long-term productive capacity. As outlined in the last edition of Northern Exposure, this is an economy strong enough here and now, but highly susceptible to the ‘unforseen events’ that often come with the passage of time.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.