Australia’s hopes of a falling dollar on US tightening look weaker again today. The Fed tapered again last night but markets bid up everything in sight on the bearish data flow instead. Here’s what our Janet had to say:

Information received since the Federal Open Market Committee met in March indicates that growth in economic activity has picked up recently, after having slowed sharply during the winter in part because of adverse weather conditions. Labor market indicators were mixed but on balance showed further improvement. The unemployment rate, however, remains elevated. Household spending appears to be rising more quickly. Business fixed investment edged down, while the recovery in the housing sector remained slow. Fiscal policy is restraining economic growth, although the extent of restraint is diminishing. Inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace and labor market conditions will continue to improve gradually, moving toward those the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for the economy and the labor market as nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term.

The Committee currently judges that there is sufficient underlying strength in the broader economy to support ongoing improvement in labor market conditions. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions since the inception of the current asset purchase program, the Committee decided to make a further measured reduction in the pace of its asset purchases. Beginning in May, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $20 billion per month rather than $25 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $25 billion per month rather than $30 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee’s sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy remains appropriate. In determining how long to maintain the current 0 to 1/4 percent target range for the federal funds rate, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

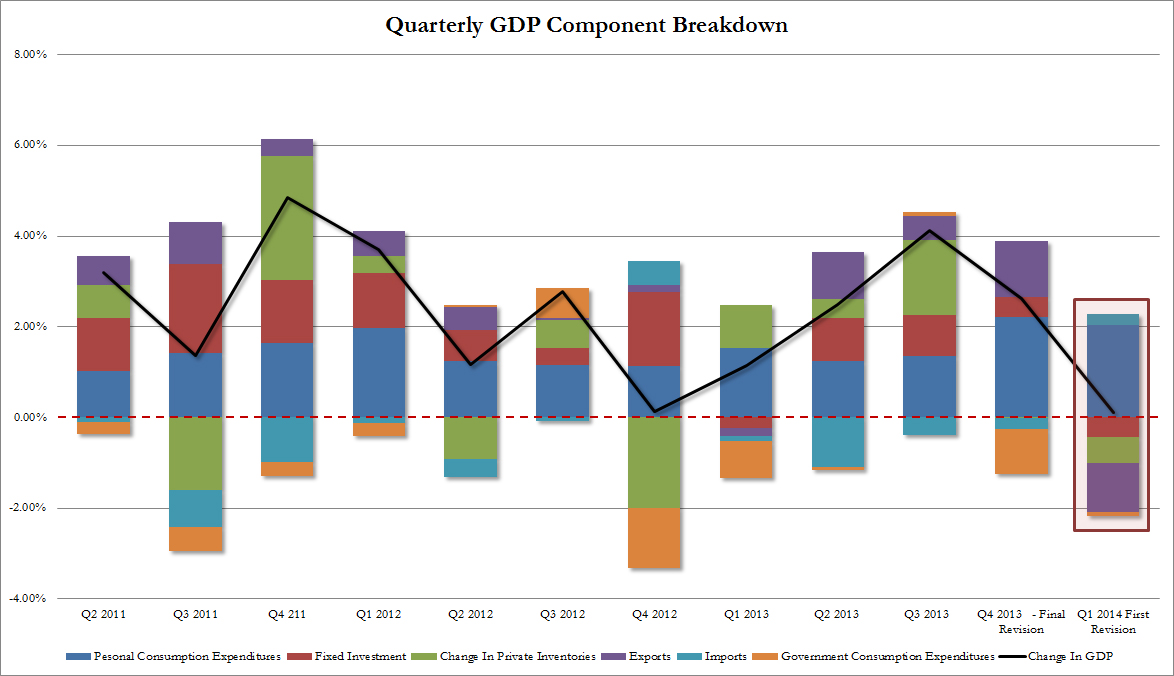

Low rates forever! Data was mostly awful. First quarter annualised GDP came in at 0.1%, everything but consumption was busted (chart from ZH):

Advertisement

Real gross domestic product — the output of goods and services produced by labor and property located in the United States — increased at an annual rate of 0.1 percent in the first quarter (that is, from the fourth quarter of 2013 to the first quarter of 2014), according to the “advance” estimate released by the Bureau of Economic Analysis.

…The increase in real GDP in the first quarter primarily reflected a positive contribution from personal consumption expenditures (PCE) that was partly offset by negative contributions from exports, private inventory investment, nonresidential fixed investment, residential fixed investment, and state and local government spending. Imports, which are a subtraction in the calculation of GDP, decreased.

So, the US has virtually been in recession, but it is bouncing back, of course, and Goldman Sachs immediately forecast 3% for Q2:

MAIN POINTS:

1. GDP grew only 0.1% in Q1 (vs. consensus +1.2%). Personal consumption rose 3.0%, although the increase appears to have been largely due to special factors in services spending, including a weather boost to utilities and Affordable Care Act-related healthcare spending. Outside of personal consumption, business fixed investment disappointed our expectations, falling 2.1%. Equipment investment was particularly weak (-5.5%). Exports fell 7.6%, with net exports subtracting eight-tenths from growth. Residential investment declined 5.7%, reflecting weaker housing data. As we expected, inventory accumulation returned to a more normal level ($87bn), subtracting a further six-tenths from growth. Government spending was roughly flat on the quarter. Final sales to domestic purchasers—excluding the effect of inventories and net exports—rose 1.5%. Overall, we do not see Q1 growth as representative of the underlying trend, in light of weather distortions, the out-sized subtraction from net exports, and the drag from inventory normalization.

2. ADP employment increased 220k in April (vs. consensus 210k). The distribution of job gains by industry was similar to that seen in recent months, with the largest job gains in professional and business service jobs (+77k) and trade, transportation, and utilities (+34k). Construction employment added 19k, while manufacturing employment was a bit soft at +1k . March ADP employment growth was revised up by 18k to 209k. ADP has yet to prove itself as a reliable predictor of nonfarm payroll job growth, following methodological revisions in 2012.

3. The employment cost index—which measures total compensation costs—rose 0.3% at a quarterly rate in Q1 (vs. consensus +0.5%), a slowdown from +0.5% in Q4. On an unrounded basis, the gain was the slowest since 2009Q2. Wages and salaries also grew 0.3% in Q1 (vs. +0.5% in Q4) and an even slower 0.2% in the private sector. On an unrounded basis, wage and salary growth was the slowest in the 32-year history of the series. Benefit costs rose 0.4% in Q1 (vs. +0.6% in Q4). On a year-over-year basis, compensation costs for all civilian workers rose 1.8% and wages and salaries rose 1.7%. Overall, the report continues to suggest subdued inflationary pressure from the wage side.

4. We are starting our Q2 GDP tracking estimate at 3.0%.

Advertisement

As Goldman says, there was more evidence of the snap back in activity post winter with the ADP employment report solid at 22ok jobs and the Chicago PMI also relaunched 7 points to 63.

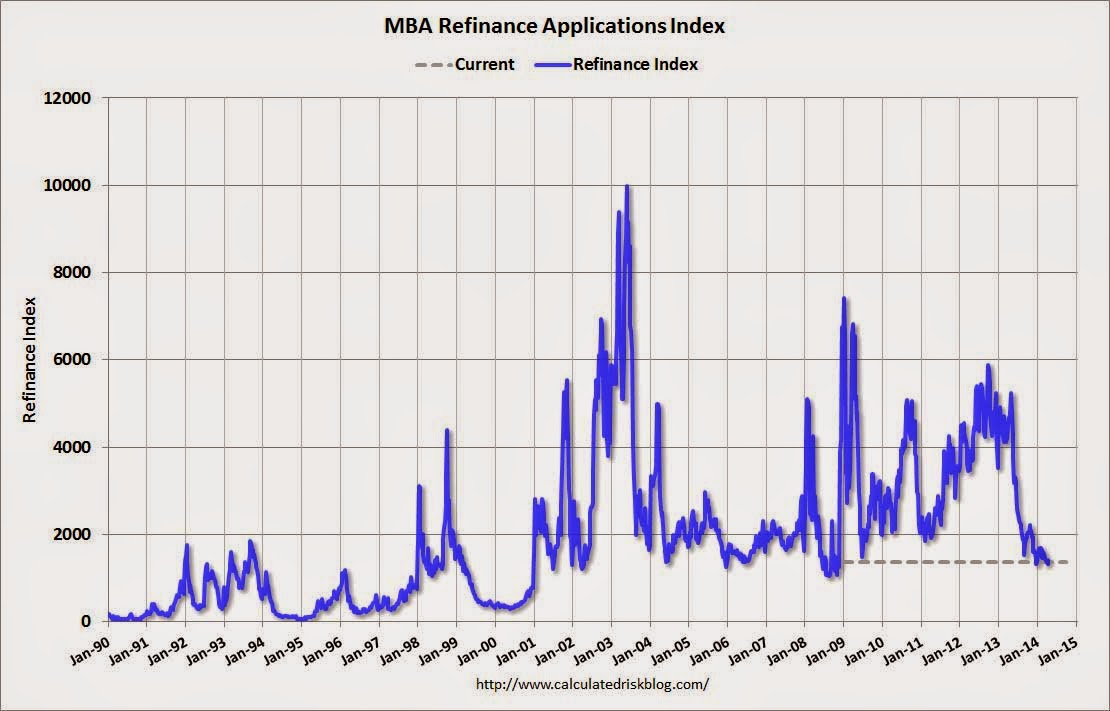

But 3% is still bold. There is little sign on income growth, no sign yet of any investment pick up (the contrary actually), persistent spending is boosting imports more than exports and inventories are still high. The other data point on the night was weekly mortgage originations, which plumbed new lows despite the easing in mortgage rates:

“Both purchase and refinance application activity fell last week, and the market composite index is at its lowest level since December 2000,” said Mike Fratantoni, MBA’s Chief Economist. “Purchase applications decreased 4 percent over the week, and were 21 percent lower than a year ago. Refinance activity also continued to slide despite a 30-year fixed rate that was unchanged from the previous week. The refinance index dropped 7 percent to the lowest level since 2008, continuing the declining trend that we have seen since May 2013.”

Advertisement

House price gains are easing fast and consumption is the only standout in GDP. I’ll take the under on 3% for Q2!

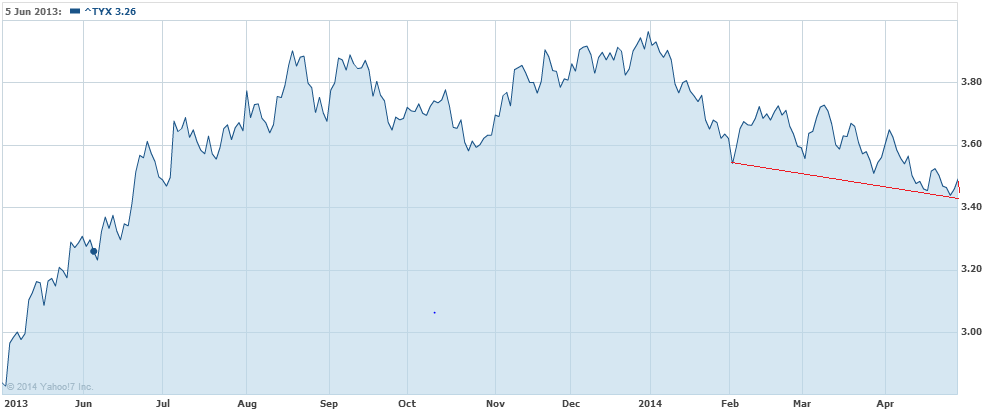

And so did markets, despite the Fed bullishness and further taper. Bonds were bid hard across the curve. The 30 year rose 1% and yields fell to within a whisker of a new low in the downtrend:

Advertisement

The 10 year roared 2% as yields fell to 2.64%. Even the short end went nuts with the 5 year up 3.5% and yields down 0.6% at 1.68%.

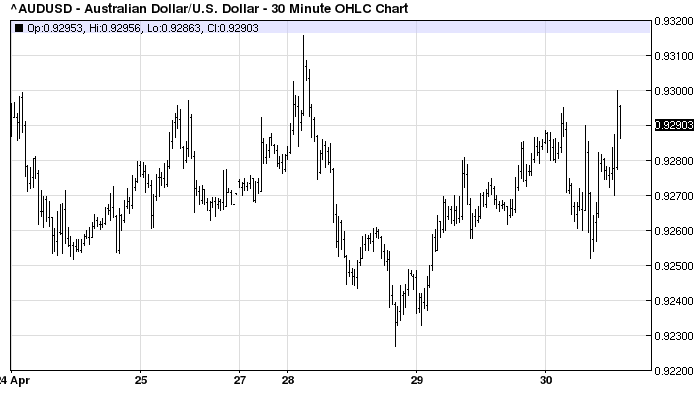

In broader markets, stocks managed a meek gain, the US dollar dumped half a cent. Just to confuse, gold fell slightly as well, but the Aussie popped to 93 cents:

Advertisement

In short nobody believes the Fed’s bullishness can last and if we want a lower dollar we’ll have to take it for ourselves.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

{kind=link}