It was night of more reasonable US data but whatever it is right now the results are the same: a bond stampede!

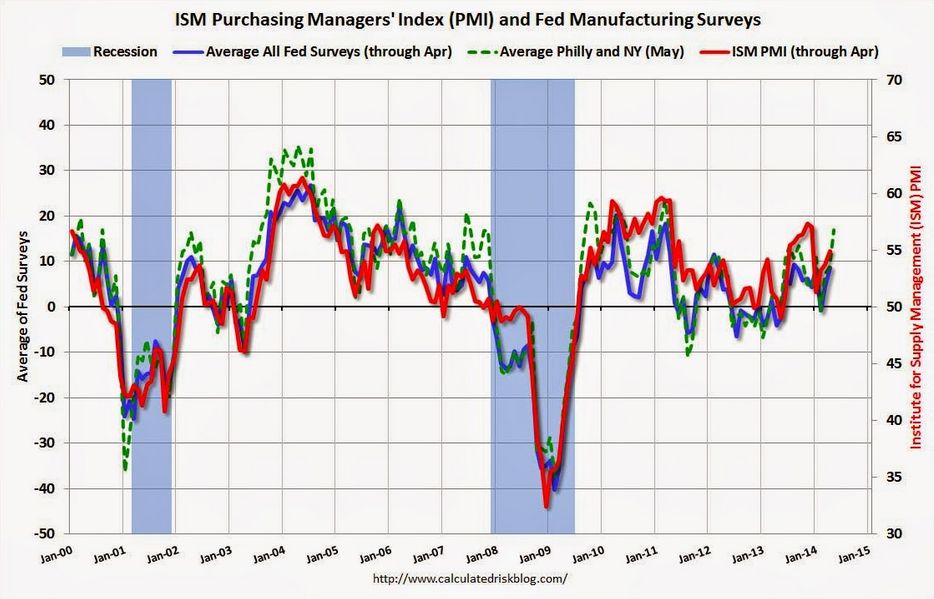

Two Fed regional manufacturing surveys were strong. The Philly Fed was firm at 16.6 up from 15.4 in April and the Empire State leaped to 19 from 1.3 in April.

That bodes well for the May ISM (all charts from Calculated Risk):

Advertisement

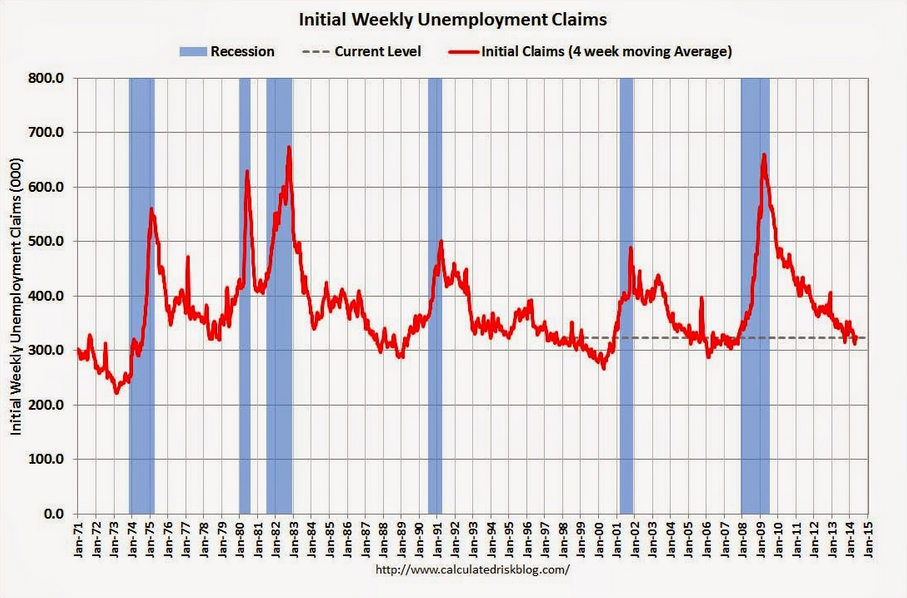

Also positive were weekly unemployment claims which fell to 297k, the lowest since May 2007, and now back in expansionary economic territory:

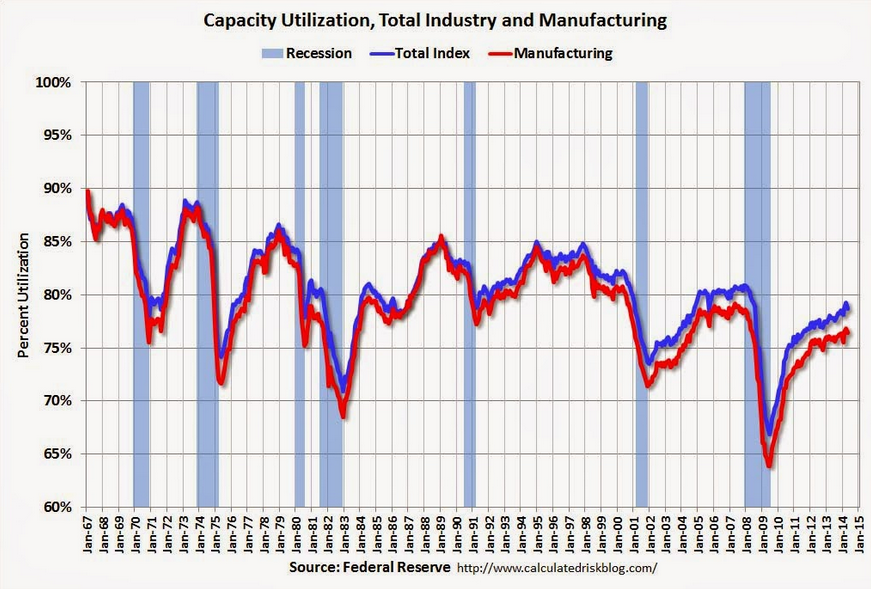

However, it was not all good. Industrial Production in April tanked:

Advertisement

Industrial production decreased 0.6 percent in April 2014 after having risen about 1 percent in both February and March. In April, manufacturing output fell 0.4 percent. The index had increased substantially in February and March following a decrease in January; severe weather had restrained production early in the quarter. The output of utilities dropped 5.3 percent in April, as demand for heating returned toward normal levels. The production at mines increased 1.4 percent following a gain of 2.0 percent in March. At 102.7 percent of its 2007 average, total industrial production in April was 3.5 percent above its level of a year earlier. The capacity utilization rate for total industry decreased 0.7 percentage point in April to 78.6 percent, a rate that is 1.5 percentage points below its long-run (1972–2013) average.

The drop was a little odd but then so were the February and March gains so I’ll take this as volatility. Year on year is still solid.

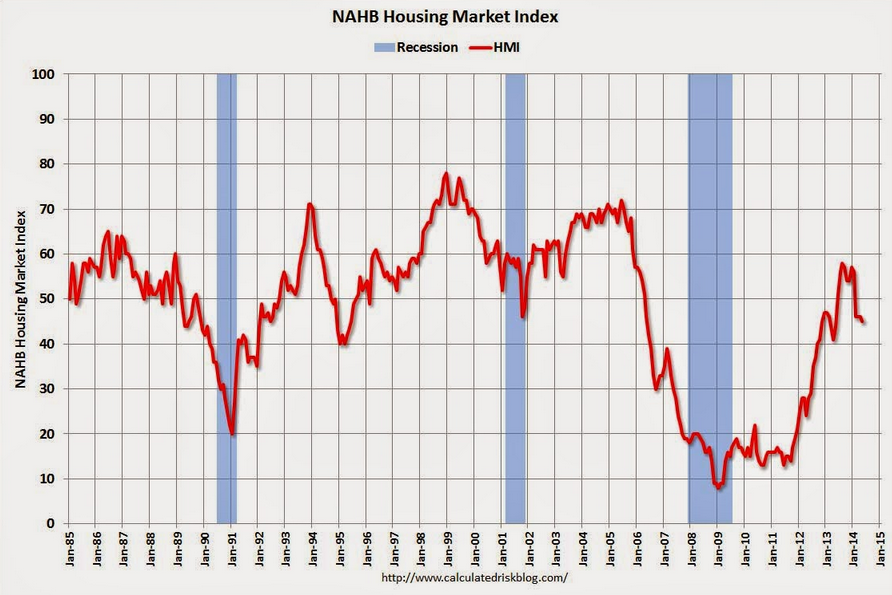

Also marginal was the NAHB Builder Confidence which fell a little but still looks decidedly toppy:

Advertisement

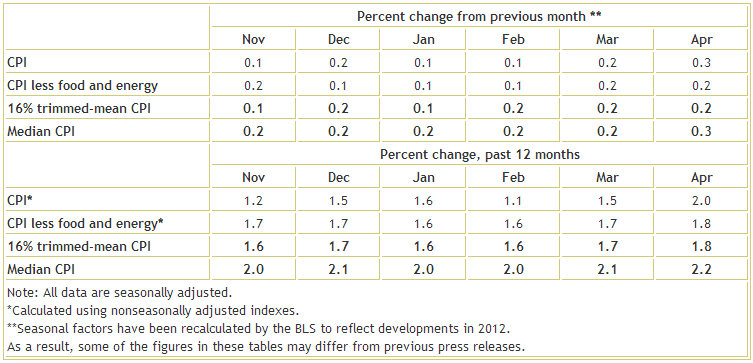

Finally, the CPI was released and came in a little stronger but is still very benign on core measures with the trimmed mean at 0.2 in April and 1.8% year on year:

Advertisement

Would this data “normally” ratioanlise a charge into bonds? Probably not but that’s what we got with the 30 year yield hitting a new low of 3.34% while the 10 year yield crashed 4 points to 2.5%.

The US dollar fell a bit and so did the Aussie and gold. There’s no swing to greater stimulus here. But bond markets were pricing for recovery and wage inflation last year. Now they’re undoing it.

If we want a lower dollar before weakness ensures it, we’ll have to take it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.