Late last year, Andy Haldane, one the smarter eggs at the Bank of England declared:

…the central bank’s new financial policy committee is taking too long to force banks to hold more capital and appeared to criticise the bank’s culture under outgoing governor Sir Mervyn King. Haldane told the Treasury select committee that the bursting of the bond bubble – created by central banks forcing down bond yields by pumping electronic money into the economy – was a risk “I feel acutely right now”.

…”If I were to single out what for me would be biggest risk to global financial stability right now it would be a disorderly reversion in the yields of government bonds globally.” he said. There had been “shades of that” in recent weeks

…”Let’s be clear. We’ve intentionally blown the biggest government bond bubble in history,” Haldane said. “We need to be vigilant to the consequences of that bubble deflating more quickly than [we] might otherwise have wanted.”

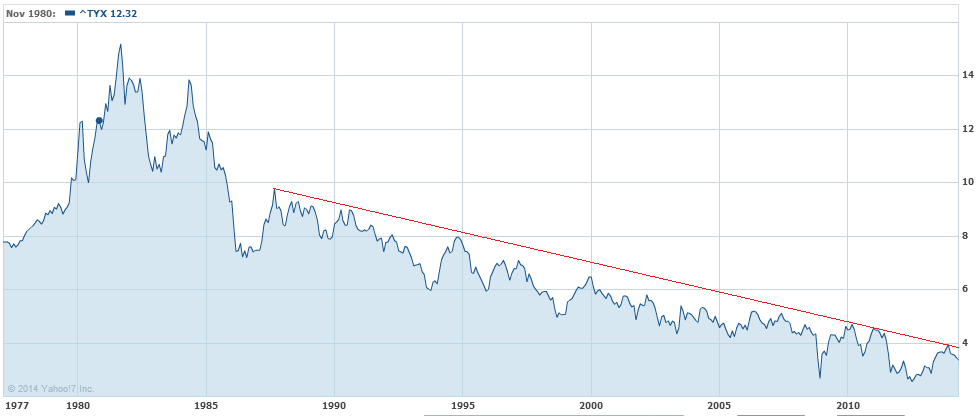

I’m wondering today if he was wrong, at least in his framing of the duration. Take a look at the US 30 year bond yield over the long haul:

That’s not a recent bond bubble. It’s an enormous 30 year bond bull market which shows something else is going on. I suspect that something is more akin to Larry Summers secular stagnation, in which Western economies are stuck in the slow lane as peak debt and de-industrialisation finally bite. If it’s a bubble it’s been growing for 30 years.

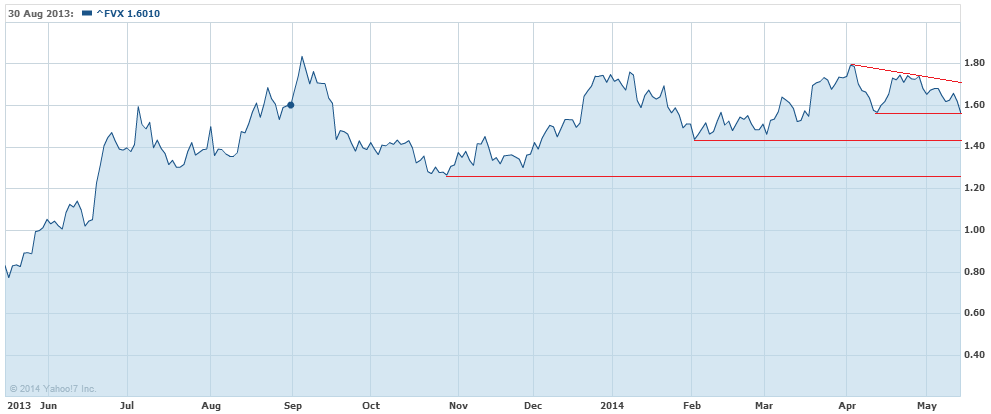

Right now, it’s all downhill for yields. Across the curve last night the US action was wholesale buying. The 5 year looks like it could break down but at least has some support levels ahead:

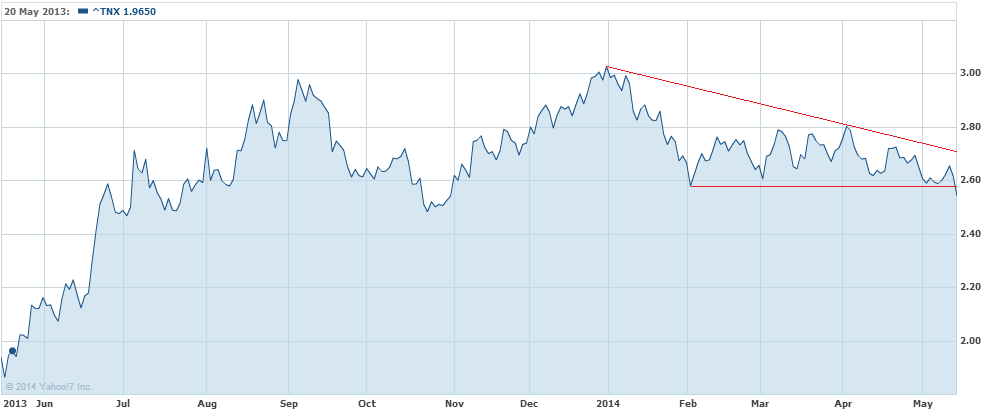

The 10 year finally broke the key support in its descending triangle pattern and looks like it could really fall now:

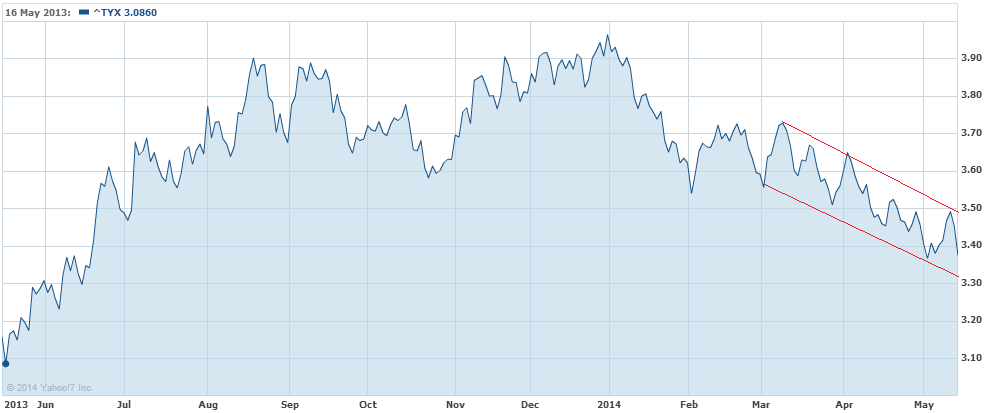

The 30 year is still in free fall:

Who knows how far this can run? The implications are similar to that described by PIMCO in its new neutral yesterday:

- a permanent low growth environment

- low downside risks

- perpetually low interest rates

- low returns on investment

Despite all of the efforts of major global central banks to print money there is little prospect of inflation anywhere. The monetarists of this world must be wondering what the Hell has happened. Considering that China is determined to rebalance away from construction, which has driven the only real source of global inflation that we’ve seen in the past five years – commodity prices – global disinflationary pressures look set to get worse.

It’s epochal stuff and shows just how far behind the curve Australia is with its fading inflationist growth model. The catch up has begun but it’s got a long, long way to run.