While the rest of the electorate is being asked to tighten its belts, the Real Estate Institute of Australia (REIA) has released its pre-Budget submission, demanding greater taxpayer assistance for home buyers along with access to their superannuation for a housing deposit, and has also warned the Government not to “meddle” with negative gearing, repeating the lie that it would lead to rental shortages and push-up rents.

It’s a textbook case of rent-seeking by a body at the centre of Australia’s politico-housing complex.

Let’s examine some of the REIA’s key recommendations, beginning with their demand for first home buyer aid:

Advertisement

The REIA urges Government to not only retain but to review the amount currently provided to first home buyers as the relative size of the grant has declined markedly in relation to house prices.

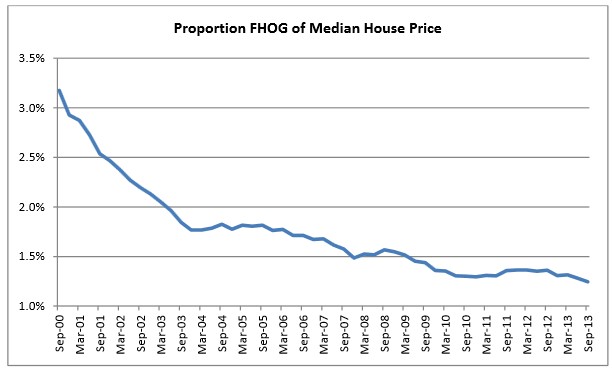

Since the introduction of the FHOG in July 2000 the Australian quarterly weighted average median house price increased 2.6 times from $220,443 in the September quarter of 2000 to $562,503 in the September quarter of 2013. Not only is the availability of the grant limited to less than one in five first home buyers, the contribution of the grant towards the purchase price has more than halved from 3.2% to 1.2% over the period. The proportion of the FHOG in the median house price has exhibited a downward trend since the introduction of the grant.

The REIA proposes that the FHOG be set at $15,000 for all housing, new and established and that it be indexed to median house price movements annually.

Notwithstanding the response by first home buyers to the Boost in 2008, the REIA is concerned that the overall level of homeownership in Australia has not shown significant improvements since 1995 and that first home buyers find it increasingly difficult to enter the housing market. Although the Boost helped the participation of first home buyers in the market, it was a short term measure and did not provide first home buyers long term support…

Allowing access to a proportion of superannuation funds would help prospective buyers to save for a deposit faster…

Furthermore, access to superannuation for the purchase of a first home by helping reverse the trend of falling home ownership, addresses the looming large policy problem of large numbers of long-

term renters aged 45 years and over remaining in the rental sector and possibly requiring rental support in later years…

The REIA proposes the Commonwealth Government establishes a scheme to encourage young Australians to have access to their superannuation for the purpose of raising a deposit for a first home.

If Saul Eslake’s 50 Years of Housing Policy Failure presentation showed us one thing, it was that demand-side measures aimed at promoting “housing affordability” and home ownership do not work. Despite the massive decline in interest rates and the myriad of subsidies to first home buyers (FHBs), the home ownership rate has decreased over the past 50 years (see next chart).

Advertisement

Under Australia’s constipated planning system, the REIA’s proposed reform would be self-defeating as the extra capacity to borrow and spend would soon be capitalised into higher home prices. At the same time, the Government would lose valuable taxation revenue for no public benefit.

If the REIA was truly concerned about the plight of FHBs, it would lobby strongly for an end to negative gearing and a relaxation of planning and other supply-side constraints that prevents the supply of affordable housing. Instead it has argued for the retention of negative gearing in its current form, thereby allowing investors to continue crowding-out FHBs, repeating the lie that its removal would lead to rental shortages and push-up rents:

Negative gearing in its current form for the purpose of property investment is complementary to the goals of the Government in addressing the supply of rental accommodation…

Changes to negative gearing would impact on the supply of housing and the level of rents in already tight rental market. In 1985, the Hawke Government abolished negative gearing for property only to have it reinstated in 1987. During that period rents increased by 57.5% in Sydney, by 38.2% in Perth and by 32.0% in Brisbane. In the current tight rental market expectations are the implementation of the Henry Review recommendations will have a dramatic negative impact on renters similar to the results of mid-1980s.

Advertisement

It seems you can’t keep a good lie down. The REIA’s claims are false. The below chart plots the Australian Bureau of Statistics (ABS) rental series from 1972, with the period where negative gearing losses were quarantined (i.e between June 1985 and September 1987) shown in red. As you can see, there was nothing spectacular about this period, with much higher rental growth recorded in earlier periods when negative gearing was in place:

Similarly, if we deflate the above series by CPI, in order to remove the effects of inflation, we again see that rental growth over the period when negative gearing was quarantined was nothing special, with periods of higher rental growth recorded both prior and subsequently:

If it was true that the abolition of negative gearing caused rents to rise, shouldn’t rents have risen Australia-wide since negative gearing affects all rental markets?

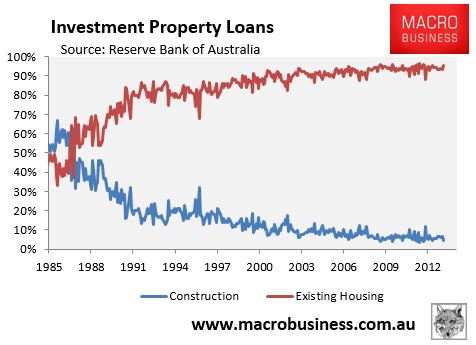

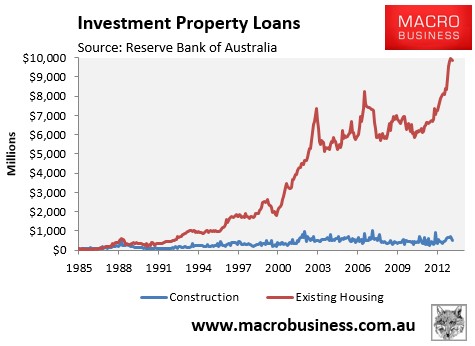

Nor is the claim that negative gearing boosts rental supply backed-up by evidence. As shown repeatedly, the overwhelming majority of investors purchase existing housing (see below charts).

Advertisement

And since investors primarily purchase existing dwellings, negative gearing in its current form simply substitutes homes for sale into homes for let. Accordingly, the policy has done little to boost the overall supply of housing or improve rental supply or rental affordability.

In the event that negative gearing was wound-back and a proportion of investment properties were sold, who does the REIA think these homes would be sold to? That’s right, they would be purchased by renters (or other investors that would rent them out). In turn, those renters would be turned into owner-occupiers, reducing the demand for rental properties and leaving the rental supply-demand balance unchanged.

Advertisement

Back to the REIA:

Further to amend the current negative gearing provisions for housing would be treating real estate differently to other asset classes and create a distortion on the investment landscape and result in a resource misallocation.

So the REIA supports introducing further distortions into the housing market via first home buyers grants and allowing access to superannuation, but laments so-called distortions arising from the quarantining of negative gearing.

Here’s a question for the REIA: would you support removing negative gearing if both property and other assets (e.g. shares) were treated equally (hence creating no distortions)? Didn’t think so.

Advertisement

The REIA makes other spurious claims in its submission, along similar lines to those made for negative gearing. For example, the below argument against reforming capital gains tax is a cracker:

Any proposal that increases the tax paid on capital gains on property, such as in the Henry Review, if implemented, would discourage investors from allocating financial resources to the property market, exacerbating the already low levels of vacant rental properties and consequently pushing rents up further.

The impacts on rents could be similar to the situation in 1985 when the Hawke Government denied many investors tax deductibility of interest payments. With a market response that lead to an undersupply of rental property and escalating rents before the decision was reversed less than 24 months later. The REIA believes that any increase in capital gains tax arrangements for rental property, would lead to a similar response to that in 1985.

Overall, the REIA’s pre-Budget submission is a text book case of self-interest trumping the wider public interest. It should be seen as an artful work of comedy and used as a door stop by all and sundry.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.