The marvelous Reserve Bank of New Zealand (RBNZ) has released its bi-annual Financial Stability Report, which in true RBNZ fashion contains some blunt assessments about risks facing the New Zealand financial system and broader economy.

While acknowledging that the financial system is currently sound, the RBNZ remains concerned about New Zealand’s high household debt and its over-valued housing market:

Advertisement

Debt in the household sector remains high relative to income, and house prices are overvalued on several measures. As a result, financial stability could deteriorate if there is a sharp correction in house prices, particularly if accompanied by a reduction in debt repayment capacity…

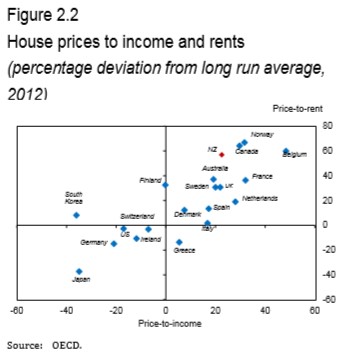

Recent increases in house prices came after a strong increase in the decade prior to 2007, and only a modest correction in the aftermath of the GFC. House prices are well above their long-term average relative to fundamental metrics such as rents and incomes, and stand out as particularly stretched among OECD economies (figure 2.2). The OECD and IMF both believe that house prices are significantly overvalued…

The RBNZ also notes some success from its speed limits on high loan-to-value ratio (LVR) mortgage lending, implemented in October 2013, although pressures remain:

After the announcement of the speed limit, the Reserve Bank noted its expectation that such a limit would help dampen house price inflation and credit demand. The early evidence suggests that the LVR speed limit is having the expected effect of moderating housing imbalances. The outlook for rising interest rates is expected to support the LVR speed limit in moderating housing demand…

The Reserve Bank’s initial estimates were that LVR restrictions would lower house sales by 3-8 percent, house price inflation by 1-4 percentage points, and housing credit growth by 1-3 percentage points, over the first year that the restrictions are in place…

The Reserve Bank currently judges that LVR restrictions are meeting their objective of mitigating the risks associated with excessive growth in housing-related credit and house prices, with clear evidence of a particularly strong restraining impact on housing market activity in the first six months of implementation…

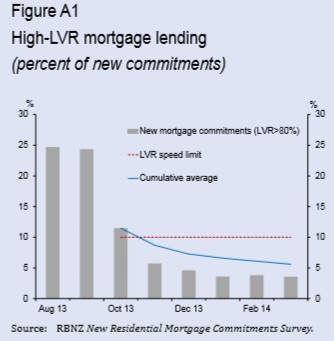

Since October, banks have rapidly reduced the share of high-LVR lending to well below the speed limit requirement of 10 percent (figure A1)…

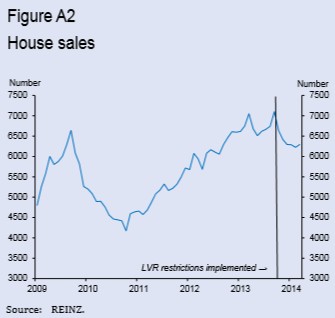

Data since October confirm that house sales have dropped sharply since the introduction of LVR restrictions, following a run-up in the months prior to the restrictions coming into effect (figure A2)…

Over the longer term, increasing housing supply is expected to eventually bring about a better balance in the housing market. Although the LVR speed limit is helping to contain the risk of a sharp housing correction, house prices remain at elevated levels and have continued to grow faster than household incomes. Housing demand will likely continue to outstrip supply in the near term, particularly with strong net immigration adding to population growth…

Advertisement

The RBNZ expects the LVR speed limits to remain in place until the housing market comes into better balance, which will be assisted by the upward movement in interest rates and an increasing supply of new houses:

However, we will need to be confident that immigration pressures will not cause a resurgence of house price inflation. We consider that the earliest date for beginning to remove the LVR restrictions is likely to be late in the year.

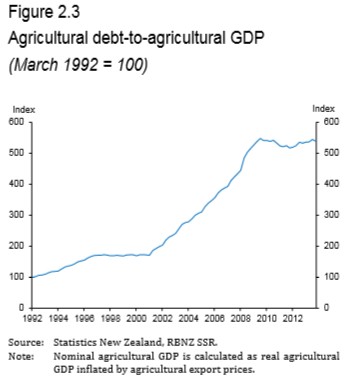

High leverage in New Zealand’s dairy sector is also worrying the RBNZ, with a slowdown in China a particular concern:

Advertisement

Debt is also elevated in the dairy sector, although incomes are currently strong. A reduction in dairy export prices, and any associated fall in land prices, could place pressure on the more highly leveraged borrowers in this sector…

World dairy prices have already declined by over 20 percent in recent months, as global and domestic supply have increased. There are also several potential global shocks, including a disruption in the Chinese economy, which could trigger a more significant decline in commodity prices and a consequent drop in collateral values, specifically land prices…

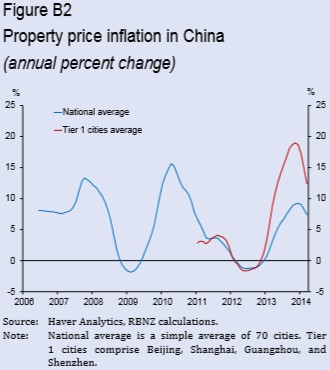

There is a risk of a disorderly correction to the lending and property boom in China, resulting in a sharp slowing in Chinese growth…

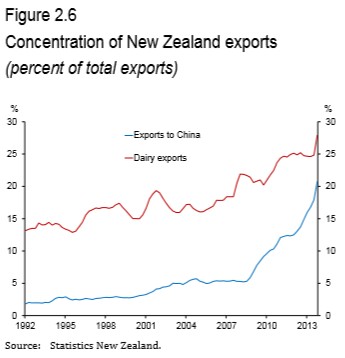

New Zealand’s export receipts – especially from dairy exports – have become increasingly reliant on Chinese economic growth (figure 2.6). As a result, incomes in the indebted agricultural sector could fall sharply, notwithstanding the expected buffering effect of a floating New Zealand dollar. Furthermore, a slowing in China could have significant ramifications for the Australian economy, which could reduce the demand for New Zealand exports in Australia…

In November 2013 China overtook Australia to become New Zealand’s most significant export partner. China has been urbanising rapidly in recent years, and urban households tend to have higher incomes and more westernised diets. As a result, Chinese consumers have greatly increased their consumption of meat and dairy products, and New Zealand’s agricultural exports to China have benefited accordingly. A contraction in Chinese demand associated with a financial crisis could have a major impact on New Zealand agricultural exports. While New Zealand could maintain export volumes by diverting products to other markets, a drop in Chinese demand for soft commodities would put significant downward pressure on New Zealand’s export prices globally.

The RBNZ is also concerned about the flow-on effect to New Zealand’s financial sector, which would suffer from any disruption to international capital markets, in turn impairing funding conditions for New Zealand banks:

More broadly, New Zealand remains exposed to the international financial markets as a result of its high external debt and ongoing current account deficit…

A sharp slowing in the Chinese economy would have significant implications for the New Zealand financial system. Fallout within the financial sector in China could affect global funding markets, potentially increasing funding costs for the New Zealand banks, and result in a marked slowdown in global growth…

A sharp fall in [Chinese] property prices would reduce household wealth, increase balance sheet stress for local governments and property developers, and potentially trigger more widespread asset losses in the financial system.

…the degree of direct contagion from Chinese to global financial markets is highly uncertain. Nonetheless, serious financial disruption would likely undermine investor sentiment towards the Asian region, leading to capital outflows and posing significant challenges for policymakers in the region – particularly in those countries with high levels of foreign currency debt. Similarly, capital could withdraw from New Zealand and Australia as investors re-evaluate assumptions of strong Chinese growth underpinning growth in both countries over the longer term. Chinese outward investment has increased rapidly in recent years, although remaining small compared to global flows of foreign investment. In the event of financial crisis, Chinese investors may choose to repatriate funds invested abroad in an attempt to consolidate balance sheets.

Advertisement

Finally, the RBNZ intends to develop a “comprehensive stress testing framework for the banking system”, adding that it is also developing a framework for ongoing insurance supervision after the completion of its initial licensing process.

Overall, it’s another frank assessment by the RBNZ, largely free of spin. The Reserve Bank of Australia could learn from its approach.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.