Guy Debelle is on the hustings today giving a speech about why changing capital flows will bring down the dollar. It’s too long to post but has some great charts. Here’s the gist:

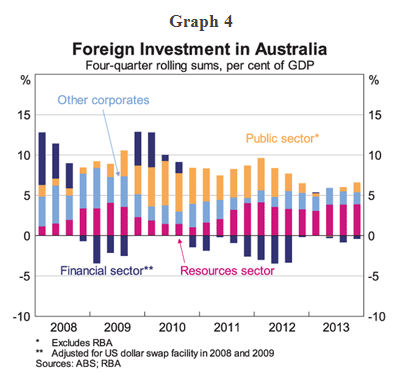

Given that changes in gross inflows to the banking, resources and government sectors have had a significant influence on changes in the composition of Australian capital inflows over recent years, it is worth considering what factors might affect these flows in the future.

In terms of the banking sector, it seems unlikely that the pattern of capital flows will change materially any time soon. The banks are likely to continue with little net debt issuance in the period ahead; that is, only issuing enough debt to replace that maturing. To the extent that investment in the non-resources sector is more likely to be intermediated by the banking sector than resources sector investment, the RBA’s forecast pick-up in investment in the non-resources sector might see some pick-up in business credit from its current low rate of growth. Even so, this would not require much of an increase in wholesale debt issuance given that deposit growth continues to outstrip lending growth by a few percentage points.

Turning to the resources sector, the investment phase of the resource boom has peaked, and a number of resource projects are moving into the production phase. As foreign investors have played a large part in the financing of this investment, a move to the production phase should result in reduced capital inflows. At the same time, the increase in resource export volumes should increase the resources sector’s export revenue. The combination of higher revenues and lower capital expenditure outlays could be expected to lead to an increase in resources sector profits and, particularly, an increase in the share of these profits that are paid out as dividends to investors. Given that the resources sector is largely foreign-owned, this would be accompanied by an increase in dividend payments to foreign investors (an outflow on the net income component of the current account).

Although the resources sector’s transition from investment to production will likely result in a reduction in net capital inflows to the sector, the effect on the Australian dollar is more nuanced. While capital inflows to the resources sector may be expected to fall (and thus reduce demand for Australian dollars), this will also be associated with declining imports to the sector, as resource investment has relied heavily on imported capital and labour. Moreover, the balance of payments records these notional foreign direct investment flows as capital inflows (and imports on the current account) even though the respective flows may have been predominantly in US dollars. The (still substantial) part of the capital inflow that represented an actual transaction in Australian dollars was that needed to pay for their workforce in Australia and the often small share of the assembly done locally.

Additionally, to the extent that resource firms’ revenues are primarily denominated in US dollars and their shareholder base chooses to be paid dividends denominated in US dollars, these flows will have no net direct influence on the exchange rate. Only those flows needed to pay for the operations in Australia, to pay dividends to the Australian shareholder base and taxes to the Australian Government will result in purchases of Australian dollars. The net result of all of this is that we might expect to see reduced capital flows and reduced demand for Australian dollars as the resources sector moves into the production phase.

Finally, on the outlook for investment inflows to the public sector, while the foreign ownership share of Australian government debt has declined somewhat from its peak, it remains at a historically high level. Sovereign investors tend to be relatively slow to change their portfolio allocations. Hence we might expect these holdings to be relatively sticky. Recent capital inflows to the sector suggest that demand for Australian government debt remains robust. The extent of any additional purchases will depend in part on the extent of further foreign exchange reserve accumulation by other central banks.

One source of potential additional demand for government securities is from Japanese investors, who have historically held sizeable shares of Australian government debt. While there is limited evidence to date that the program of quantitative easing in Japan has encouraged investors to substantially increase their purchases of other countries’ assets, the most recent data suggest that demand for Australian debt from Japanese investors has started to pick up.

Notwithstanding the possibility of these flows from Japan, the net implication of these developments is that one might expect to see reduced capital inflows in the period ahead, with the possibility of a consequent further decline in the Australian dollar. This would help in achieving balanced growth in the economy. That said, the ability of economists to forecast exchange rate movements is notoriously poor, but at least this might give you some idea of some of the dynamics at play in the period ahead.

Didn’t the RBA recently argue that bigger commodity volumes were raising the dollar? The speech hit the currency a little bit, anyway.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.