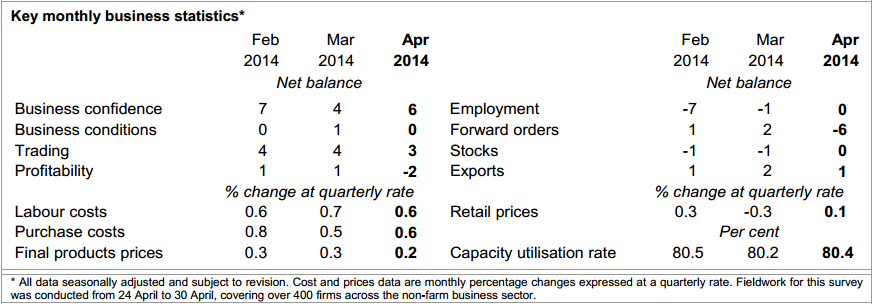

The NAB Business Survey for April is out and held up better that I feared:

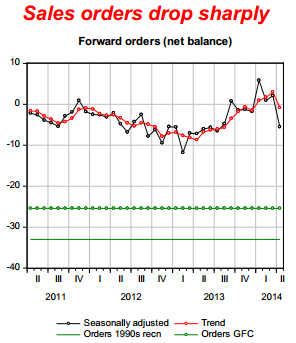

Business conditions more subdued in April but confidence up marginally – shrugging off ‘tough budget’ rhetoric. Sales eased slightly, employment slightly better but still soft, profits weaker. Conditions remain volatile and mixed across industries: ‘bellwether’ sectors (wholesale, transport) still soft with near term conditions likely to remain sluggish – forward orders fell sharply. Inflation pressures relatively muted, but retail prices accelerated. Tomorrow’s Budget to show lower growth outlook with fiscal headwinds. We now expect Q1 GDP to be stronger (mainly net exports) and unemployment to peak marginally lower, prompting us to drop our call for a rate cut in November (subject to Budget). Rate rises not till late 2015.

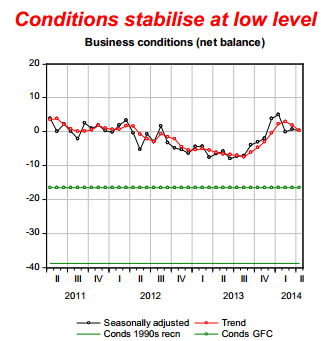

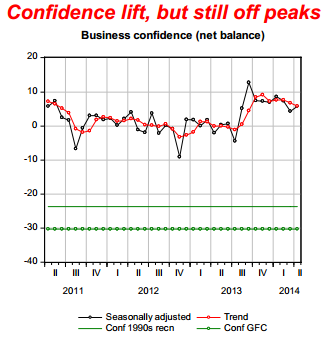

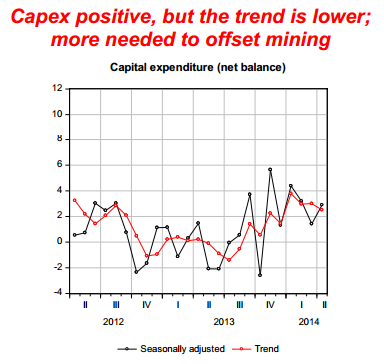

Here are the charts:

Advertisement

Not terrible but not great either and all trends are now down. Remember that this index tends to follow consumer confidence so I expect further erosion in the months ahead.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.