In another potential blow to Australia’s magnificently expensive seven LNG projects, Citigroup has released an interesting research report forecasting a “slump” in Japanese LNG demand from 2015:

Japan is a key player in world energy markets, accounting for 35% of LNG (seaborne trade)… Since the March 2011 disaster, consumption has increased more than 20%, including an increase of around 34% for power generation.

…we forecast that the LNG peak will come in 2014… With the population already shrinking and the number of households set to shrink, we expect demand for many energy sources to peak in the relatively near future…

We expect the weightings of nuclear, coal, and renewables to rise versus FY3/14. We forecast that nuclear plants will gradually restart from 2014 H2 and that the weighting of nuclear in power generation volume will recover from 1% (FY3/14) to 21% by FY3/31. In contrast, we expect the weightings of LNG-fired power and oil-fired power to slump, to 24% from 42% and to 4% from 15%, respectively. We anticipate growth in renewable energy (including hydro) to 20% from 11%. We see coal remaining steady, with a share of 29%…

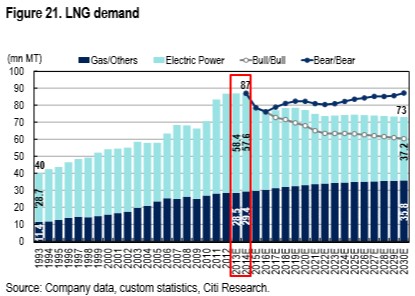

Based on our main renewable energy growth and nuclear plant restart assumptions (base/base scenario), we forecast demand for gas for power generation (currently about 70% of total gas demand) will fall steeply. This is because 1) in the short term we forecast LNG will return to a midrange power source as a result of nuclear plant restarts, and in the longer-term we expect 2) the further introduction of renewable energy, and 3) the construction of more coal-fired plants. As a result, we believe LNG demand will peak in FY3/14-FY3/15 and then decline almost uninterruptedly through FY3/31. In FY3/14, we estimate gas demand of 58mn MT for power generation and 29mn MT for other purposes. In FY3/31, we estimate demand of around 37mn MT and 36mn MT, respectively [Figure 21]…

We are forecasting a decline in LNG demand of over 12% over the next three years in whichever case… We expect the pace of demand shrinkage to be intimately correlated with progress in nuclear restarts. We think that a relatively large number of nuclear plants will be restarted if just the first few can be restarted; however, if restarts lag versus our expectations, we would expect the decline in LNG demand to be moderate…

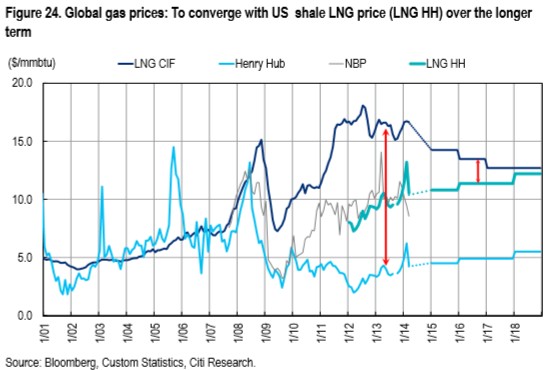

Over the long term, we expect the LNG import price to decline and LNG sourcing to diversify as shale LNG imports expand.

Australia’s magnificent seven LNG projects run at a break even between $12 and $14, suggesting a squeeze on profitability and returns on equity if Citi’s forecasts prove to be accurate. For Australia it means more falls in the terms of trade as LNG follows the pattern set by coal and now iron ore.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.