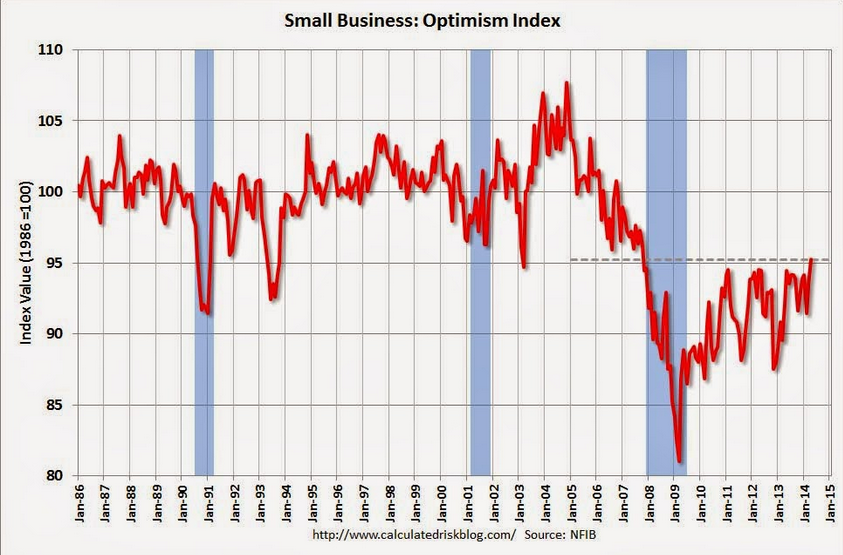

April’s Small Business Optimism Index rose 1.8 points to a post-recession high of 95.2. The economy continues to perform modestly and April’s index followed suit as it crossed the 95 marker for the first time since 2007. …Labor Markets. NFIB owners increased employment by an average of 0.07 workers per firm in April (seasonally adjusted), weaker than March but the seventh positive month in a row and the best string of gains since 2006.

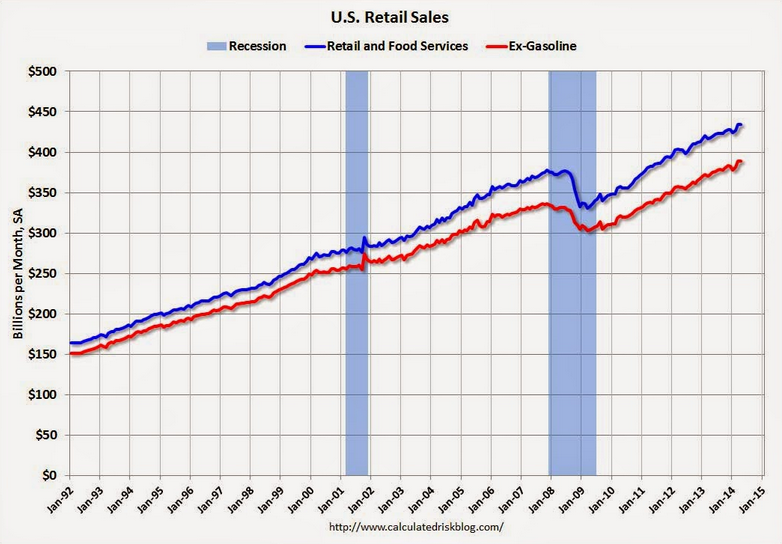

Retail sales missed expectations but eked out growth:

The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for April, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $434.6 billion, an increase of 0.1 percent from the previous month, and 4.0 percent above April 2013.

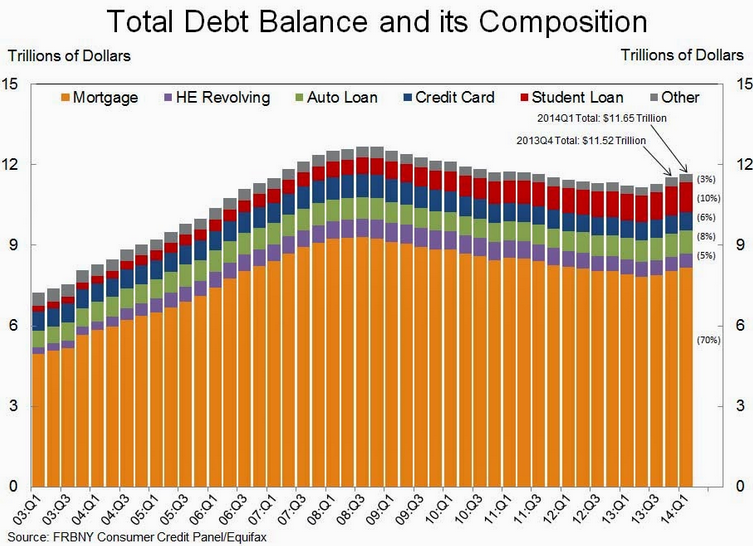

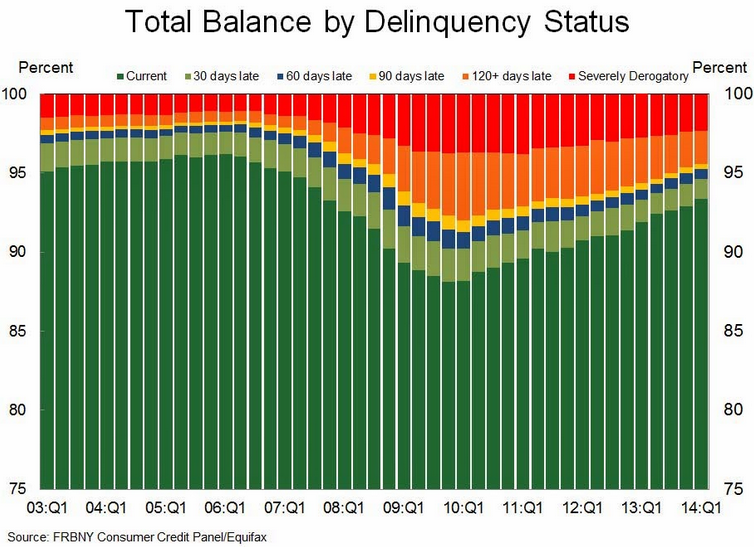

…outstanding household debt increased $129 billion from the previous quarter. The increase was led by rises in mortgage debt ($116 billion), student loan debt ($31 billion) and auto loan balances ($12 billion), slightly offset by a $27 billion declines in credit card and HELOC balances. Total household indebtedness stood at $11.65 trillion, 1.1 percent higher than the previous quarter. Overall household debt remains 8.1 percent below the peak of $12.68 trillion reached in Q3 2008. The report is based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample drawn from anonymized Equifax credit data.

Additionally, an update to a recent blog discussing the impact of student loan debt on housing and auto markets is available on our Liberty Street Economics Blog.

“We’ve observed household debt increase three quarters in a row and delinquency rates at their lowest levels since 2008,” said Andy Haughwout, vice president and economist at the New York Fed. “However, the direction of future mortgage originations will have an important implication on the household financial outlook and we will continue to monitor it.”

I could not have put that better myself. I would say deleveraging isn’t over until credit surpasses its previous peak and that still seems well distant at this stage.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.