I was chatting to my bank manager yesterday about today’s RBA meeting and he made the point that customers are beginning to reckon on interest rate rises later this year. August was the hottest bet.

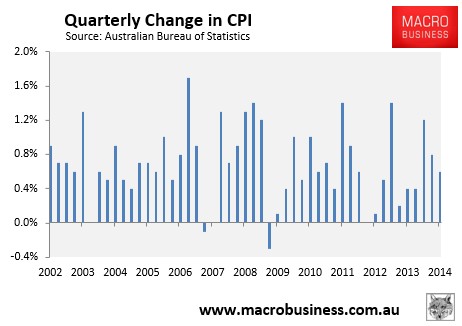

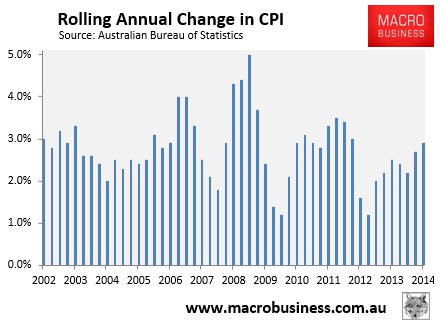

It’s a good month to finger because the bullhawks may be screetching for a hike at that point. The June quarter inflation number is out on the 23rd of July and it’s possible that it will break above the RBA’s 3% ceiling. The June CPI number will see a 0.4 reading drop out from last year and if it’s replaced with a 0.7% or above reading then the headline number will be running at 3% or above.

But even in that event, the RBA will not hike rates. Rather, it will argue that tradable inflation will pass in time and the removal of the carbon price will deflate some prices. It will also want to try to jawbone housing and/or domestic activity for while. If that fails then the chances are the next step will be some form of macropudential tightening before any rate rise.

Why?

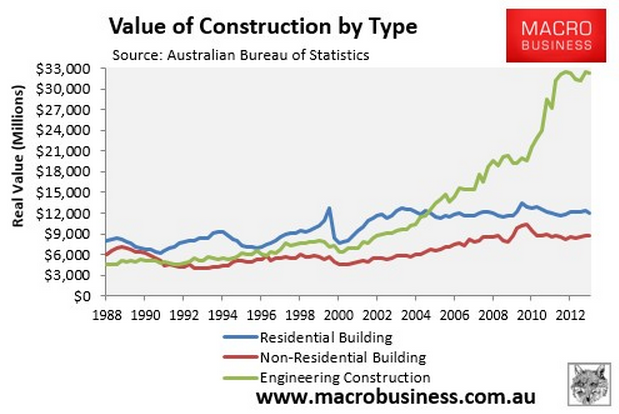

There are three main reasons. First and foremost, the composition of Australian growth in this new cycle is much more vulnerable to rate hikes than in previous cycles. That’s because of the huge transition underway in mining. By now we all know that that transition is from construction to production. What fewer realise is that the production phase involves far fewer jobs than the construction phase. NAB estimates 100k fewer but it could be more with big multiplier effects. That means that the growth provided by production via net exports actually shrinks activity in the real economy even if headline growth looks OK.

Although the capital boom that drove construction has already begun to fall, the component that drives the jobs has not, so that lies ahead, much of it in the next eighteen months as LNG projects begin to pump:

Add in government austerity of any kind and the only driver left for domestic activity is household spending, which the RBA will have to support with low interest rates.

The second reason there will be no rate hike is the terms of trade. Combined Chinese property and iron ore busts are underway.

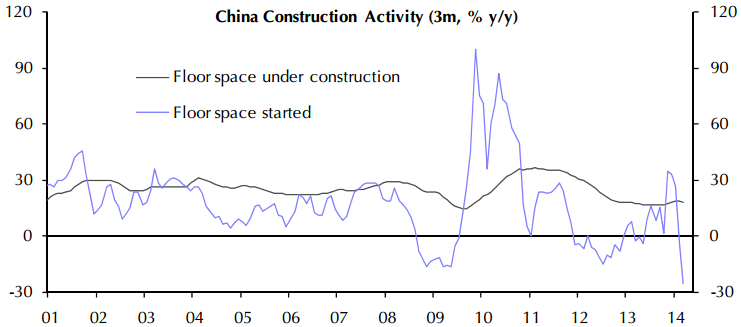

Tight credit is bringing Chinese property prices to heal. The People’s Bank of China may be forced to ease monetary policy as the year goes on but not before pain gets much deeper in the property market. Property construction trails price movements by some six months so the second half of this year is going to see residential construction come off sharply (whether or not it then fires again). In fact, it has already begun, chart from Capital Economics:

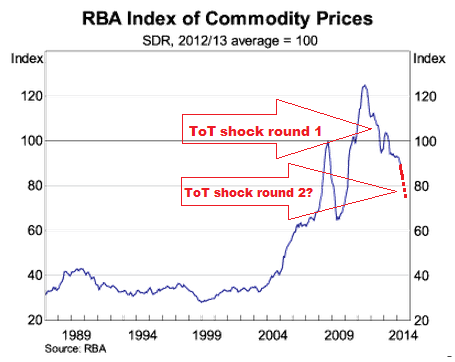

More than half of Chinese steel goes into residential property and as the iron ore supply ramp continues that is going to ensure that our number one commodity keeps falling in price. Here is my forecast for the Terms of Trade falls ahead over the course of the year:

This is the RBA’s index of commodity prices, which is a good proxy for the ToT. I expect the index will drop through 8o by this time next year which will constitute a second round terms of trade shock. Remember that the first, which began in late 2011, smashed nominal growth, added 1% to unemployment, blew up the Budget, initiated a miner equity bear market, and triggered 2.25% in rate cuts even though the mining investment boom was powering.

Perhaps less dramatic effects can be expected this time given mining has already busted to some extent but you can still expect budget instability, further big falls in major mining equities and possible crisis in some, as well a material hit to national income.

The third reason there will be no rate hikes this year is the dollar, which remains way overvalued. The dollar has already risen a lot since its low in the 86s and anything near mid nineties is roughly the equivalent of 50bps of tightening from that level. That is slowing tradables, will subdue inflation in time and slow property as offshore investors wait for better prices.

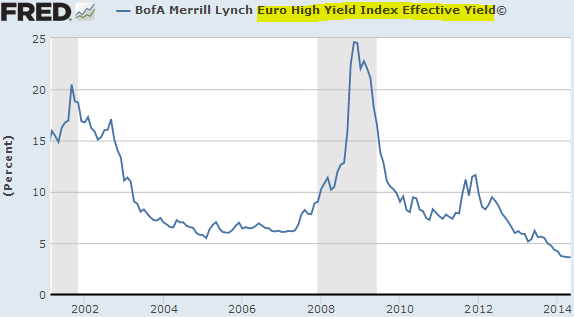

One must also understand that the global setting for forex and fixed interest remains a mad chase for yield as both global growth and inflation remain flat and falling. I could pick any number of charts but one of peripheral European bond yields tells the tale:

If the RBA raises interest rates in this environment the dollar will go straight back through parity at the worst possible time.

There won’t be any rate rises in 2014. I doubt there will be in 2015, either. Those focused on the cyclical froth are missing the big and growing structural pressures.