Goldman Sachs is out with a study of the effects of macorprudential policy on house prices, via FTAlphaville:

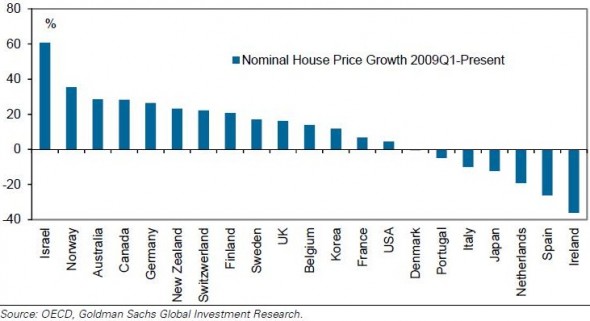

Relative to their previous peaks, nominal house prices are now 43%higher in Norway, 20% higher in Canada, 14% higher in Israel and 7%higher in Australia.

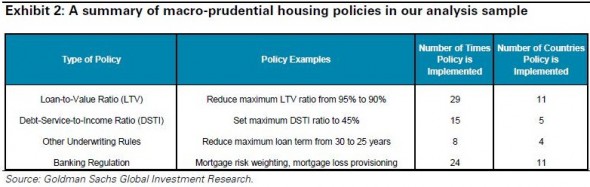

…In Canada, nominal house prices did not fall much during the GFC and have risen steadily since 2009. Homebuilding activities have also exceeded their pre-GFC levels. In response, the Ministry of Finance lowered the maximum LTV ratio from 100% to 95%, reduced the maximum amortisation period from 40 years to 35 years, and set the maximum DSTI ratio to 45% in October 2008. In April 2010, it lowered the maximum LTV ratio further to 90% for refinancing mortgages and to 80% for investor properties. In March 2011, the authorities reduced the maximum amortisation period from 35 years to 30 years and decreased the maximum LTV ratio to 85% for refinancing mortgages.

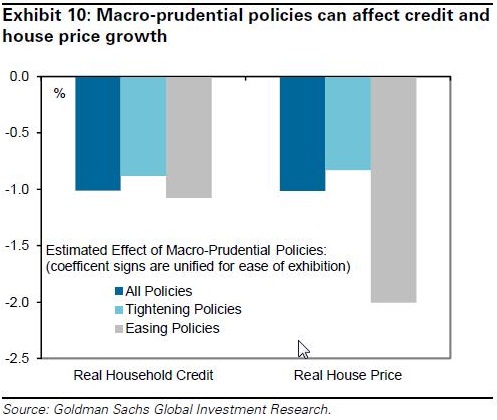

We find that macro-prudential housing policy, when designed to tighten (ease) mortgage availability, reduces (increases) the annual growth rate of real household credit by 1% and the annual growth rate of real house price by 1% (Exhibit 10). These estimates are statistically significant and are of economically significant magnitudes, given that the average annual growth rate is 5% for real household credit and 2% for real house prices in our sample. Estimating VAR and DSGE models using US data, Jarocinski and Smets (2008) and Iacoviello and Neri (2010) find that a 50bp increase in the federal funds rate leads real house prices to decline 0.75%-1.5%. Putting our estimates in this context, the average macro-prudential housing policy in our sample is equivalent to a 50bp change in the policy interest rate.

Advertisement

If Australia were to implement this and provide cover for an additional two rate cuts, the dollar would probably fall to 80 cents.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.