Cross-posted from Sober Look:

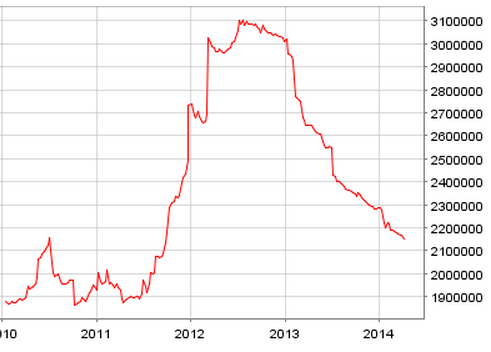

The story from the Eurozone is beginning to sounds like a broken record. The area’s monetary conditions continue to tighten as the Eurosystem’s balance sheet shrinks.

The decline is driven by banks’ deleveraging, as the LTRO balances decline.

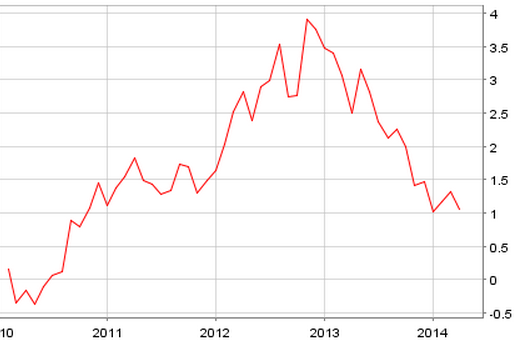

As a result of bank deleveraging, loans to area’s households are now growing at merely 0.4% per year.

… while loans to Eurozone’s businesses are falling at over 3% per year.

This has resulted in the overall decline in private loans of 2.2% from a year ago, which was worse than economists had expected. With credit contraction continuing, it is not a surprise that the broad money supply growth has stalled at just over 1% a year.

According to some however, these trends do not matter much because the Eurozone is simply undergoing a “creditless” recovery. We are supposedly paying too much attention to credit growth. The ECB will simply stay on the sidelines and watch the area’s economy blossom.

WSJ: – But if the banking system is in poor shape, why are policy makers increasingly optimistic about the recovery?

Part of the answer is that too much focus is being placed on credit growth.

One in five recoveries is “creditless” according to a 2011 International Monetary Fund working paper. Credit growth remained very subdued for several years during the recovery from Sweden’s financial crisis in the early 1990s, according to J.P. Morgan research. U.K. bank lending is only now starting to pick up, more than a year after a strong recovery began.

The early stages of a recovery are funded from income and savings rather than new debt. Indeed, continued deleveraging is inevitable as loans issued during the boom are repaid.

More importantly, there is encouraging evidence that the ECB’s ongoing “comprehensive assessment” of bank balance sheets is having a cathartic effect.

Of course Japan too had a “creditless” recovery – until it didn’t. But let’s not make such silly comparisons.