CLSA’s Brian Johnson is the probably the best bank analyst in the country. His latest take is well worth your reading.

Having sat through the recent Australian bank reporting season we sensed a potentially dangerous degree of “optimism in perpetuity” with management expecting loan losses to stay low and a seeming increase in regulatory capital targets a mere distraction. That said we also noted consistent NIM declines given (i) the beginnings of a potential price war as the banks reduce incremental loan pricing to gain market share in a low system credit growth environment, (ii) the NIM dilutionary impact of increased holdings of low yielding High Quality Liquid Assets, and (iii) lower interest rates reducing the rates of returns on free funds.

As detailed in our previous sectoral reports Australian bank share prices continue to be driven by the macro environment rather than stock specific micro factors – in particular the global distortions from Quantitative Easing (refer Australian Banks (QE teeter totter: To QE-ternity and beyond!) . As detailed in Figure 1 QE –

inflates Australian bank earnings (low loan losses, writeback gains, positive CVA, positive marks in trading books),

alleviates concerns about structural deposit shortfalls,

reduces regulatory capital intensity allowing dividend payouts to expand (pro-cyclicality, asset optimisation, low loan losses), and

reinforces investor preferences for income over growth with Australian banks likely both the biggest source of structural benchmark deviation for underweight international investors but also the source of highest dividend yields.

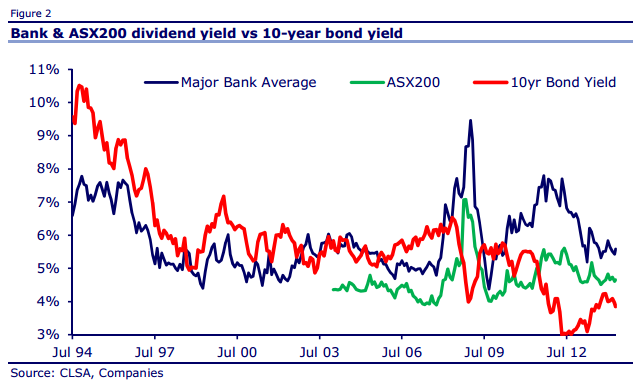

Conversely the prospect of QE-ternity (with Japan joining the club) could yet see the attractive Australian bank dividend yields (~5%) narrow even further towards the QE compressed domestic 10 year bond rate (~3.8%) (refer Figure 2).

In this macro-environment we retain our Neutral sectoral stance but caution investors should not kid themselves these stocks are trading at peak cycle PEs, on peak cycle earnings (low losses / writeback gains), capital intensity is rising and so is management complacency (ie GOAT)!

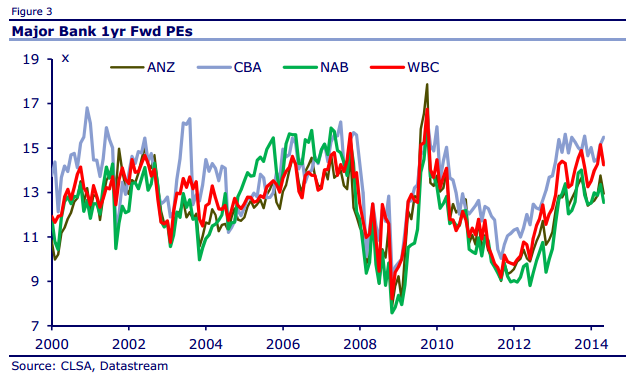

As detailed in Figures 3 and 4 “There is no-one more dangerous than a banker with no memory” – the FY07 to FY09 experience suggests that at some point QE-exit would smash Australian bank earnings, EPS and DPS(look at May 2012 at what even a whisper of QE-exit did to the Australian banks ie USD declines of >20% in 20 trading days! refer Figure 5).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.