More on the fallout from the Russia/China mega gas deal:

With Russia able to ramp up its Eastern Gas Program and China partially reducing its LNG demand growth, global LNG supply could be in further excess, which could be absorbed but at a lower price, affecting LNG developers. Although 3.7-Bcf/d of pipeline capacity based on this China gas deal may not be a sizeable amount within the entire gas market, for global LNG, it is more than 10% of the current volume or about one-third of Japan’s annual consumption. By 2020, this amount of gas should still represent roughly 7 to 8% of total LNG supply then.

More broadly, we view the Russia-China gas deal unlocking vast resources in Russia’s Far East and US LNG exports are both critical events in the development of the global gas market. US LNG exports and the introduction of Henry Hub pricing could bring gas-indexed pricing to the global market… Low political risk and gas-indexation of prices appeal to importing countries looking for alternatives to oil-indexed gas and leverage for negotiation with current and future LNG suppliers…The lack of destination clauses and the resulting flexibility should raise the amount of LNG sold in the spot market…

…Coal demand for power generation could fall further as gas substitutes coal, thereby affecting coal producers. Around 20-Bcf/d of gas, split roughly half between Russia and the US, is also equivalent to ~400-mt/yr of coal. The excess would be absorbed – at lower prices – and should weaken coal.

Here China’s position also appears critical, as it consumes ~50% of global coal and has been the single-largest driver of demand and import growth globally…If China is able to receive more gas in boosting gas-fired generation, it is possible that more coal could be pushed out of the electricity supply stack, helped also by the desire to clean up the environment.

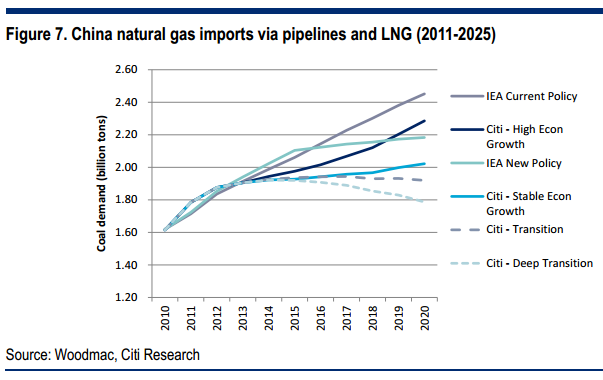

…In this scenario, suppose China’s economy indeed were to transition from the mid-7% GDP growth to the mid-5% by 2020, then the “Transition” case in the below graph on coal demand could take place. Adding more gas plants in the power stack to replace coal, particularly as carbon exchanges start up in China to help tackle pollution, coal’s dominance could weaken even further.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.