The WSJ has some nice texture on the shifting psychology of the Chinese real estate market using the example of Ningbo, a city of 8 million people in the fraught province of Zhejiang. Recent targeted easing has tried to lure back buyers but in the case of Ye Zhengwei:

“I wouldn’t buy another home even with the loosening of restrictions,” said Mr. Ye, who bought his first apartment in 2012 for 14,000 yuan ($2,250) per square meter. Now, a developer is offering a comparable home nearby for 25% less.

“I’m a victim of oversupply,” Mr. Ye said.

Property developers face a view among consumers that Chinese real-estate prices have peaked. Potential buyers are holding off on purchases.

…”The downturn this time is more serious compared to 2008 and 2011,” said Barclays Bank analyst Alvin Wong.

Recent instructions to lend more mortgages do not seem to be fairing well:

…Xiang Songzuo, chief economist at Agricultural Bank of China [said] “Now, what you’re hearing from banks’ local branches is that ‘we just don’t think the property is worth that much money anymore.'”

…Some housing agents said they recalled the 2011 downturn with fondness. Many home buyers saw the slump as a buying opportunity and approached agents about circumventing curbs on buying second or third homes,

“There are no such requests now,” said Huang Heng, a sales agent in Ningbo.

Standard Chartered also adds to the picture after a recent tour of China:

We toured a large shopping mall near the south train station in Nanjing, which is by no means remote. Nanjing is the capital city of Jiangsu province, which is the second largest province in China in terms of GDP output. Nanjing is a leading Tier 2 city.

This visit was not on our agenda, but it was highly recommended by a seasoned property researcher based in Nanjing. The whole mall was a sprawling set-up. We did not do a one-by-one count, but we estimate that there must be more than 100 shops on each floor and 500 shops in total, if not more, in the four floors. We noticed that the majority of shops (except for a few facing the streets) are still empty rooms, as they have never been let out. Through the locked glass doors, one could clearly see that the rooms were still empty and remain the way they were handed over to the buyers by the developer a few years ago.

This case illustrates the danger of overestimating demand combined with the lack of commercial planning/positioning.

…We also met Centaline’s property researchers. They believed that the number of property transactions year-to-date is down 10% YoY nationwide (though the official numbers show a decline of 5%), with Tier 1 cities showing a 30% fall, Tier 2 showing a decline of 8-10% and Tier 3 showing a flat change. YTD new starts were also down 10-15% YoY (partly because of the high base last year). They believe that property demand would continue to slow down in 2014 and 2015…

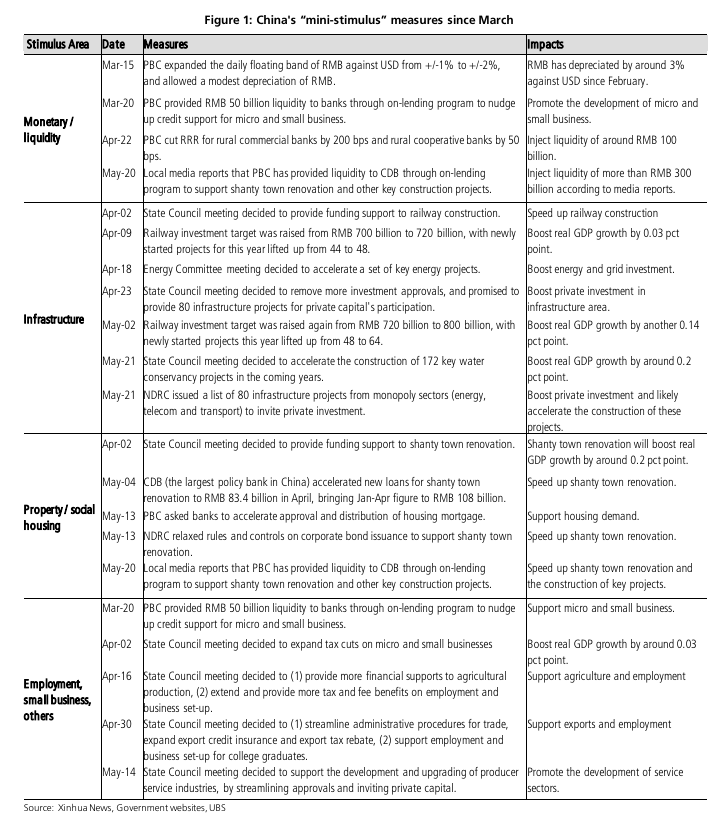

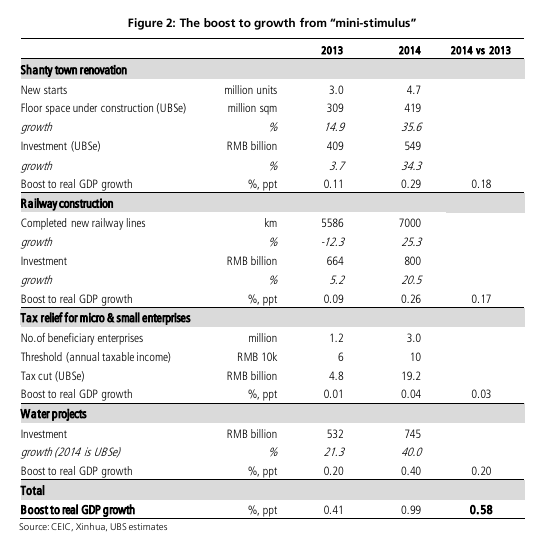

There is better news from UBS via FTAlphaville which provides a couple of useful charts that calibrate the aggregate value of the mounting targeted stimulus measures that China has undertaken so far this year:

Some of this railway and shanty town renovation spending was locked in earlier anyway so I’m not sure I’d described that as stimulus.

Anyway, the amount is modest even if some of it will help offset to blow to bulk commodity demand from property. But it isn’t enough to turn it around, which is the whole point, really.