Fresh from Westpac’s Elliot Clarke.

With growing concerns over deflation and very little room to move on interest rates, the May ECB meeting brought Euro Area credit trends back to the forefront of investors’ minds. As at March, total loans to the resident private sector were 2.2% lower than a year ago. This is not a one off: annual growth in total loans to the resident private sector has been negative for two years.

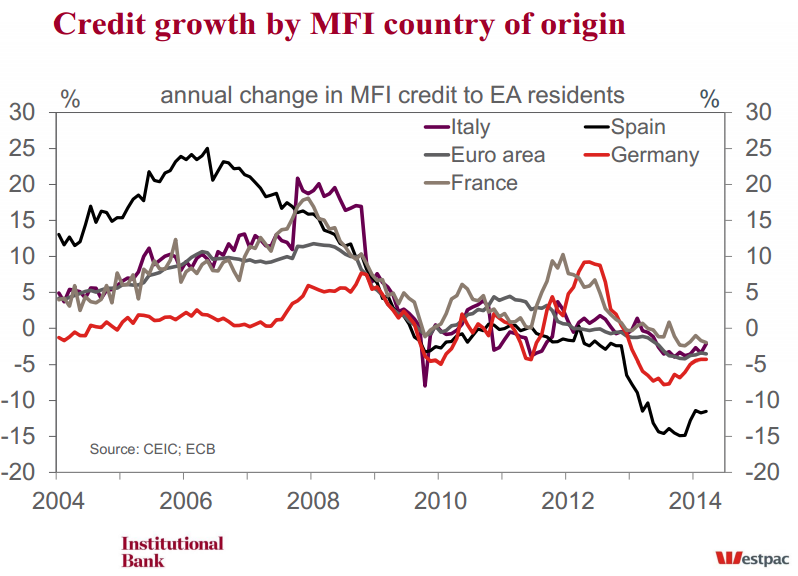

The disaggregated Monetary and Financial Institutions (MFI; i.e. European Banks) data for the Euro Area allows us to gain a better understanding of the underlying trends in credit provision, both with respect to the domicile of the banks writing the loans and also which sectors are putting the funds to work. (Note: unlike the reported aggregate headline, this data is not seasonally or working-day adjusted.)

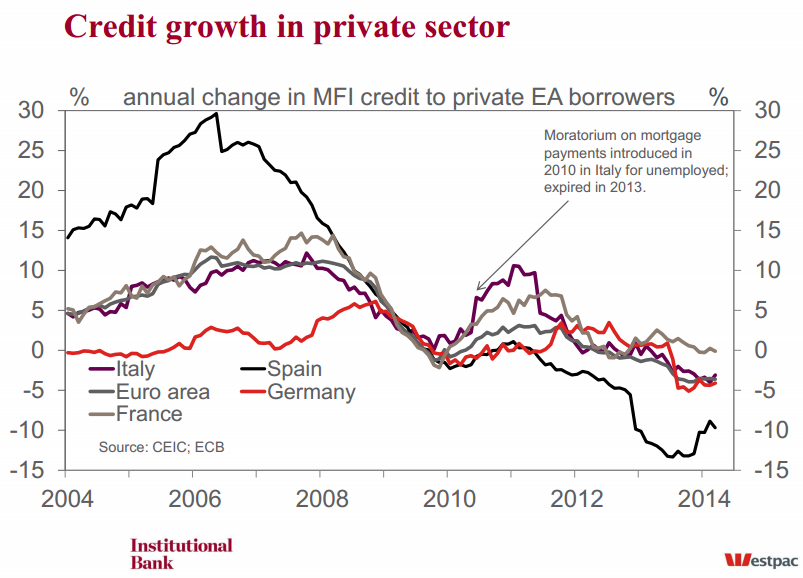

The MFI data makes it clear that there has been a marked divergence in non-MFI, private-sector credit provision by country. The decline in private lending by Spanish banks has been particularly sharp and protracted, with a cumulative 24% rundown since end-2008. This is not particularly surprising given the impact the GFC and ensuing recession have had – bad loans make up over 13% of total Spanish loans. Lending by Italian and German banks has declined by a more modest (but still substantial) 4–5% from peak levels, respectively seen in 2011 and 2012. In stark contrast, French banks have continued to increase their stock of loans, with loan growth of 11% since end-2008, but nil over the past year.

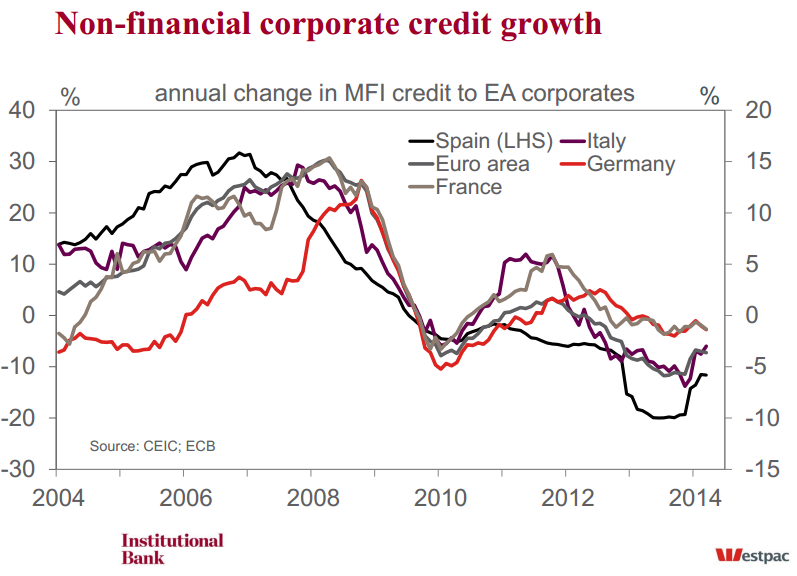

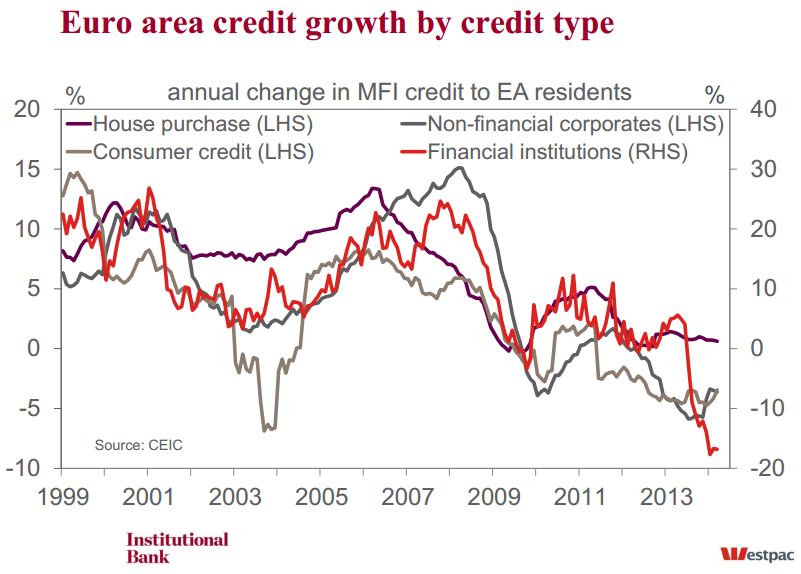

The themes apparent in the sectoral detail are also salient. Starting with loans to non-financial firms, after peaking at 15%yr in April 2008, annual growth fell to –3.9%yr by the beginning of 2010. And, after a brief renaissance in 2011, credit to this sector has trended lower for the past two years. As at March 2014, loans to Euro Area non-financials were down 11% from their January 2009 peak (but still almost twice as large as at the beginning of 1999, when the Euro was fully introduced).

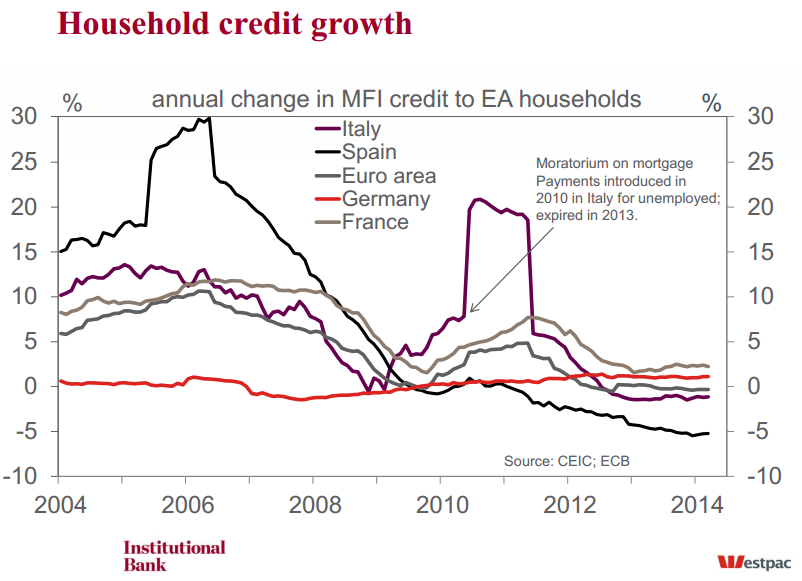

For households, we have seen two divergent trends in recent years for consumer credit and mortgages. Highlighting the reduced demand for durable goods, annual growth in consumer credit has been negative for almost three years, leaving the stock of consumer credit some 12% lower than its mid-2010 peak (but still 38% above it beginning-1999 level).

In contrast, but for a few very marginally negative outcomes in 2009, annual mortgage loan growth has remained positive since the GFC, leaving the total stock of mortgage credit some 11% higher than at the beginning of 2009 (and 150% higher than beginning-1999). A caveat to this observation: part of the strength in mortgage growth through 2010 and 2011 was due to Italy imposing a moratorium on mortgage payments for some borrowers. Annual growth in mortgage credit growth excluding Italy has averaged around 1.5% since the beginning of 2009, compared to 1.9% including Italy.

Turning to the financial sector (i.e. MFI lending to other financials), we note that leverage has fallen by around 17% over the past year. The country data discussed above also points to a reduction in the scale of MFI loans to other MFIs, with: France, –4%yr; Germany, –5%yr; and Spain, –20%yr. The timing of the decline is broadly coincident with the paying back of LTRO liquidity by MFIs as they readied their balance sheets for the 2014 stress tests. Arguably this is evidence of MFI’s (unsurprisingly) managing their exposure to suit what is appropriate from a profitability and regulatory perspective, regardless of the implications for aggregate financial system liquidity.

So what to make of these results? As is apparent in the level of loans outstanding relative to the start of 1999, the European economy benefitted significantly from the free availability of credit to all sectors in the lead-up to the GFC. Since this time, there has been a dramatic change of direction in the credit impulse, with the stock of all types of private-sector credit (excluding loans for house purchase) having declined substantially. It is hardly surprising then that the post-GFC recession has proved to be so protracted and that the growth of the past year has largely come as a result of external demand (and inventories in the overnight report for Q1).

So to see an enduring rebound in domestic activity, there is a real need for credit extension, most notably for non-financial corporates, which will require demand and supply to intersect far more frequently than it is at present.

This will only come with a return to positive growth in investment. With real investment comes jobs and income, both for households and the businesses themselves. Rising income makes existing liabilities less onerous and, with time, incentivises further borrowing for households and firms alike. All of the above also gives comfort to MFIs, with less-restrictive lending standards the likely result. Here then begins the justification of targeted, liquidity-oriented policy initiatives by the ECB, which we expect to see delivered at the June meeting. The specific targeting should be informed by the nature of the existing blockages/inhibitors. In this regard, the best resource (only it is still imperfect) is the ECB’s bank lending conditions survey. We will dissect this report in detail in a forthcoming edition.