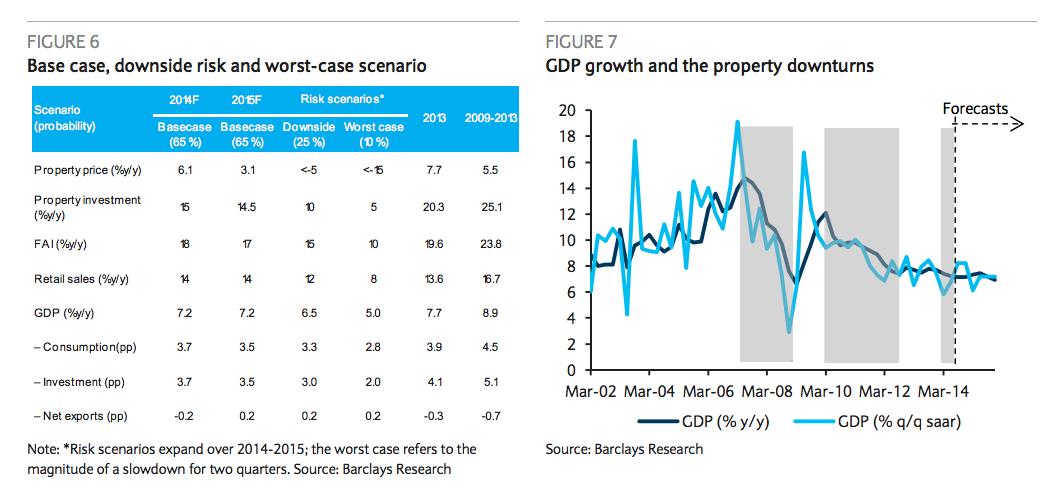

Via FTAlphaville, Barclays has issued some new scenario analysis on the Chinese property market. Here it is in a nut shell:

So, a 35% chance of GDP at 6.5% or worse next year. The sell side is slowly catching up to my 50% chance of similar. The worst case scenario is ludicrously short of the reality of course but Barclays offers a sensible conclusion:

Since taking office, the Xi-Li government has avoided making high-profile comments on the property sector, despite the continued rise in house prices in 2013. Their only substantive comment on the sector has been: “…to improve the mechanism for providing adequate housing, curbing speculative and investment demand, and promoting sustained and healthy development of the market.” This is in contrast to the previous government, which introduced many administrative measures and have vowed repeatedly to “resolutely regulate the real estate market, and bring the house prices down to a reasonable level”.

In our view, the Xi-Li government is well aware of the risks posed by the property sector. And they do not want to prick the property bubble. Rather, we think they have in mind a package of measures, which are more structural than cyclical in nature, and more market- based than administrative, to facilitate a healthier development over the longer-term. The government recognises that the ongoing structural reforms will have important implications regulate the real estate market, and bring the house prices down to a reasonable level”.

That’s fair enough. What bugs me about it, though, is that it does not acknowledge the long term impacts of reform. If rebalancing is about shifting income from industrial ponzi sectors like developers, ship-building and steel to households and consumption, then the primary mechansim for doing that is ending financial repression. It is low interest rates above all else that enables the mis-allocation of capital into uneconomic building. If you raise the rate of return required for investment in the economy then the old model collapses permanently.

That’s not to say that I disagree with the notion that Chinese authorities won’t be supporting all sorts of measures to prevent a collapse in prices. They no doubt will. But it is fundamentally a rear guard action designed to prevent an overly swift collapse of the old industrial ponzi model not the birth of a new cycle of price appreciation and construction.

That, of course, says nothing about the chance that authorities simply lose control of the process, which is what has happened just about everywhere else.

I remain constructive about China’s long term prospects given the latent productivity in such a poor but rapidly developing population (notwithstanding the demographic challenge). But even so, sell side analysts, global markets, Australia, are yet to fully absorb the implications of the epochal shift that is in the making in China.