The Commission of Audit (COA) has released its much anticipated report, which recommends some sweeping changes to Australia’s retirement system, although baby boomers would be spared any Budget pain (surprise, surprise!).

Without changes to Australia’s tax and expenditure system, the COA claims that Australia “faces 16 consecutive years of budget deficits with net debt rising from $190 billion today to $440 billion by 2023-24”.

Advertisement

The COA’s 86 recommendations are designed to save the Budget between $60 to $70 billion per year within ten years, with additional savings from the reduction of debt.

With regards to the Aged Pension, the COA recommends lowering the indexation rate to 28% of Average Weekly Earnings (from 28% of Male Weekly Earnings currently), which should improve long-term sustainability without pensions falling in real terms. Below is the explanation provided in the report:

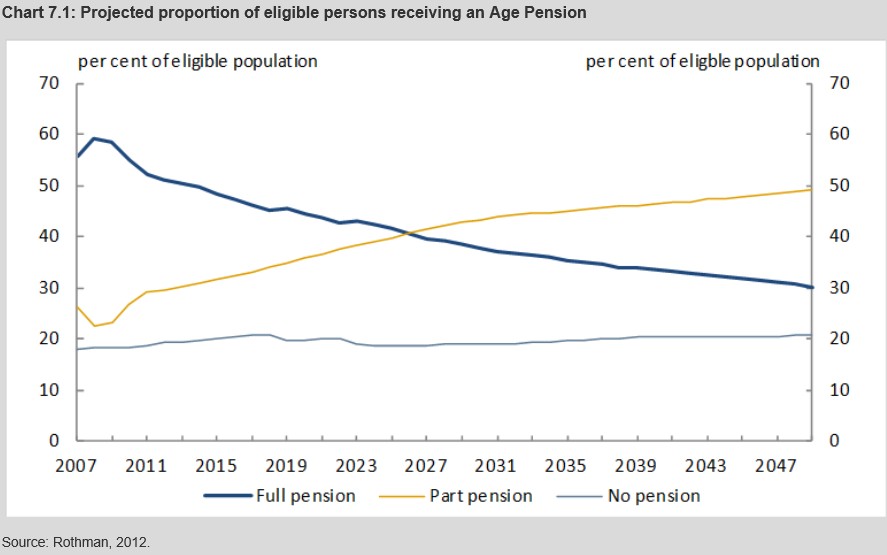

Expenditure on the Age Pension is currently growing at 7 per cent per year. Age Pension expenditure is expected to continue to increase largely as a result of an ageing population, increased life expectancies and benchmarking to the Male Total Average Weekly Earnings benchmark.

The features of the Age Pension means test, such as a 50 per cent taper rate and high income free area, can mean pensioners with relatively high levels of income (up to $47,000 in annual income) are able to access a part-rate pension…

Even allowing for a decline in the proportion of people receiving the full pension, a rise in the number of people receiving the part-rate pension will see the proportion of older Australians eligible for the Age Pension remaining constant at 80 per cent over the next forty years or so.

The Commission considers that changes are needed to ensure that the cost of the Age Pension remains sustainable and affordable and well targeted to those in genuine need…

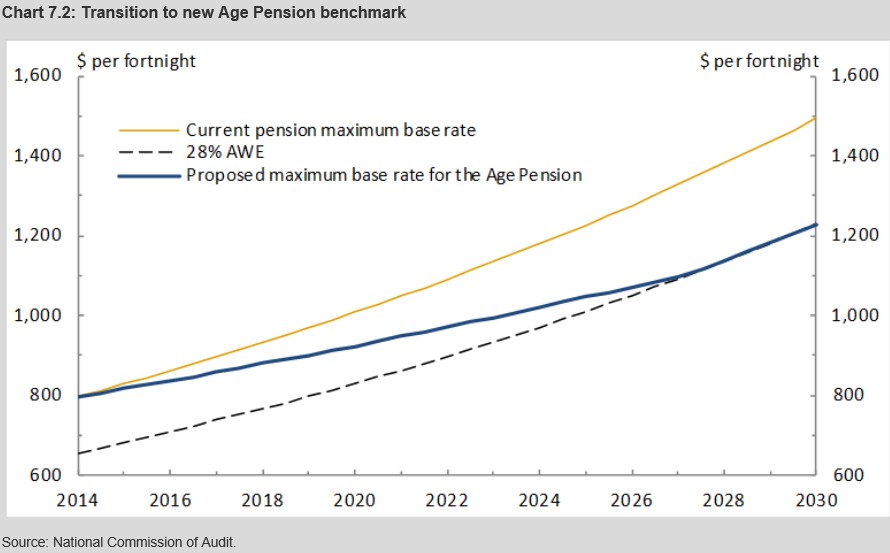

The rate of the pension is currently linked to Male Total Average Weekly Earnings. The policy rationale for using this benchmark is weak… Average Weekly Earnings is a more appropriate benchmark for the rate of the pension, given that women are a major part of the labour force. Benchmarking to Average Weekly Earnings still recognises that pensions should have regard to community standards through benchmarking to wages.

It is proposed that the maximum base rate of the Age Pension be changed over time to be equal to, and then grow in line with, 28 per cent of Average Weekly Earnings [rather than 28% of Male Weekly Earnings currently]…

The re-alignment over time could be achieved by indexing the current maximum base rate of the Age Pension to the higher of the growth in the CPI or the Pensioner and Beneficiary Living Cost Index until it reaches the new benchmark.

As shown in Chart 7.2 below, on current trends the transition can be expected to be completed by around 2027-28 (that is in just under 15 years time).

The recommended re-benchmarking of the Age Pension will ensure that Australia’s Age Pension programme is more sustainable over the long-term. The proposed transition to the new arrangements will ensure that a person’s pension entitlement does not fall in either real or nominal terms.

Advertisement

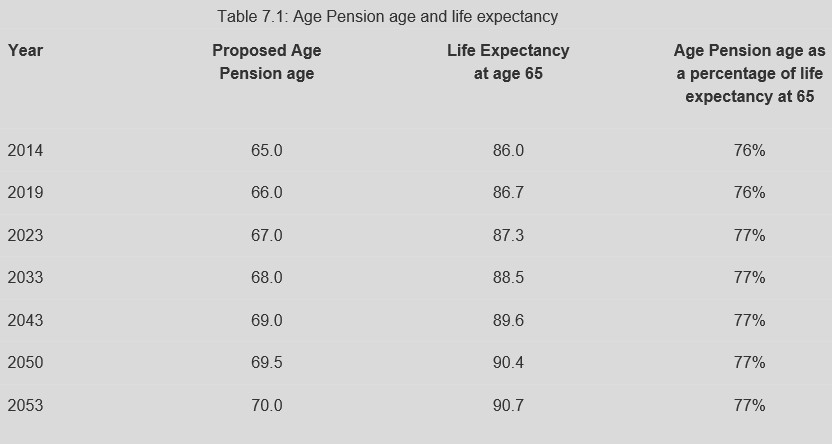

The COA also recommends tightening means testing around the Age Pension, so that the value of one’s principal place of residence is included above $500,000 for a single and $750,000 for a couple, along with increasing the access age to 70 by 2053. However, no existing recipient of the Aged Pension would have their access reduced, with changes to means testing not kicking in to 2027-28, effectively excluding the baby boomers from cuts.

…the Commission considers that there is a strong case to re-examine other aspects of Australia’s Age Pension system including tightening eligibility requirements to improve its targeting to those unable to support themselves in retirement.

Consistent with the approach outlined above any changes to eligibility should only affect new recipients and even then there should be a reasonably long lead time recognising that people need sufficient notice given the importance of decisions that are often taken ahead of retirement. No existing recipient of the Age Pension will have their eligibility or pension amount reduced as a consequence of any of the Commission’s recommendations in this area…

The Commission considers that people born before 1965 should not be subjected to this change or any other further changes to the eligibility age to ensure they have adequate time to plan for their retirement.

The Age Pension could also be better targeted by introducing a simpler single comprehensive means test.

The move to a comprehensive means test could apply from 2027-28, to new recipients of the Age Pension, to allow people sufficient time to adjust to the new arrangements.

A new single comprehensive means test could replace the current arrangement which is underpinned by dual income and assets tests. The existing assets test could be abolished and the income test extended by deeming income from a greater range of assets.

The deeming rates could be based on the returns expected from a portfolio of assets held by a prudent investor. Under this proposal, there would be a single income test based on a combined measure of employment income, business income and deemed income on assets…

The principal residence is currently exempt under the means test. This allows for high levels of wealth to be sheltered from means testing. The Commission considers that a proportion of the value of the principal residence should be included in the means test, such as the value over a relatively high threshold. The means test would capture the value above $500,000 for single pensioners and $750,000 combined for coupled pensioners.

Exempting the principal residence from the means test is inequitable as it allows for high levels of wealth to be sheltered from means testing. For example, under current rules a single person who owns a $400,000 house and has $750,000 in shares ($1.15 million in total assets) would not be eligible for the pension, while a similar person with a principal residence worth $2 million and $100,000 in shares ($2.1 million in total assets) would be able to claim a pension at the full rate…

With any changes recommended to apply from 2027-28 onwards and only to new recipients of the Age Pension, no current pensioner would be affected by this change. That is, no existing recipient of the Age Pension would have their eligibility or pension amount reduced by the proposed inclusion of the principal residence in the Age Pension means test.

The COA also attacks superannuation concessions, and urges to Government to address these in its White Paper on tax reform [tax expenditures were strangely excluded from the COA’s terms-of-reference]:

Advertisement

The Age Pension and superannuation are interrelated elements of the retirement income system and should be considered in parallel when changes to one or the other are proposed.

In regard to reform of the broader retirement income system any longer term consideration of superannuation tax concessions would be best considered in the context of the Government’s White Paper on Tax Reform. The Commission notes that many superannuation tax concessions disproportionately benefit higher income earners, when compared to taxation at marginal tax rates under the progressive income tax system.

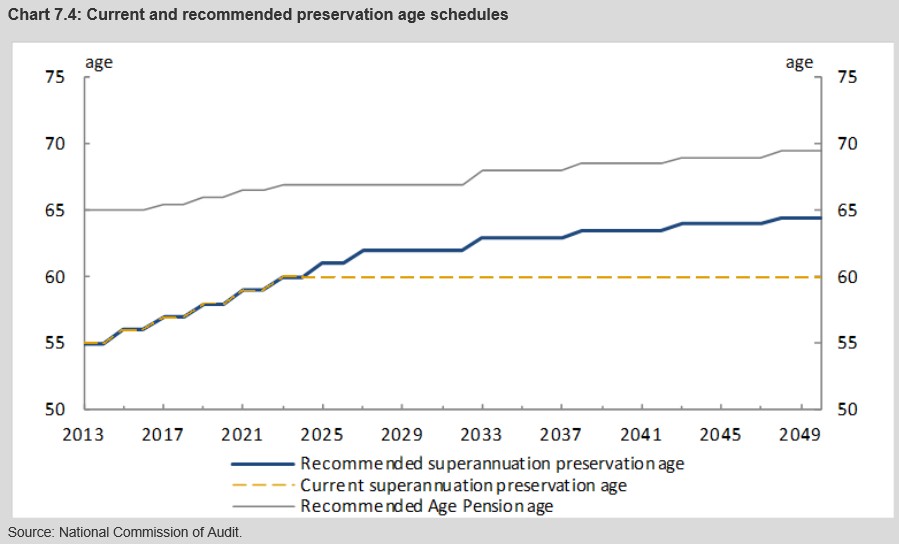

Nevertheless, it does recommend an increase in the superannuation preservation age to 5 years below the Aged Pension access age, so that by 2027 it would reach 62, and rise proportionately with the pension thereafter:

Advertisement

Finally, the COA recommends restricting access to the Commonwealth Seniors Health Card “to improve targeting to those most in need by adding deemed income from tax-free superannuation to the definition of Adjusted Taxable Income used for determining eligibility for the Commonwealth Seniors Health Card.”

While I support the COA’s recommendations on retiree entitlements, and have argued along similar lines for the past year, as a 36-year old member of Generation X, it does irritate me that the proposed reforms would not apply until 2027-28, effectively exempting the large (and wealthy) baby boomer generation from shouldering any Budget pain, and pushing the burden instead on to the younger generations.

The baby boomers are, and will likely remain, the lucky generation.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.