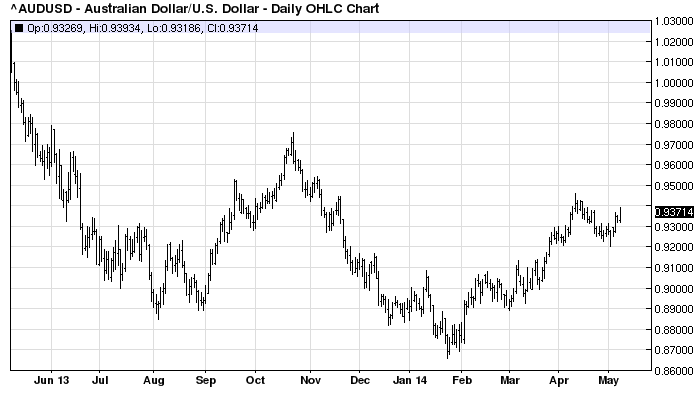

If it’s not one major funding currency then it’s another. Earlier this week the US dollar was smashed on the prospects of extended US easing. Overnight it reversed completely and the euro was hammered as the ECB gave bold hints of a resumption of money printing in June. It doesn’t seem to matter who wins on the night in the major player’s currency war but the loser is very clear, the Aussie, which is again threatening 94 cents:

That neat head and shoulders top that was forming is now history. Westpac describes the ECB:

The April CPI flashed 0.7% yr, and the ECB did nothing on May 8, but ECB chief Draghi openly acknowledged that the Council was disturbed by the inflation outlook and, “is comfortable with acting next time, but [first] we want to see the June staff projections”. He said a decision to ease in June had not been taken, but he was giving, “a preview of the discussion we will be having”. That is a very strong signal that the ECB is on the cusp of further easing. What form would a June easing take? On numerous occasions, Draghi has reiterated the ECB Council’s, “unanimous … commitment to using also unconventional instruments within the ECB’s mandate in order to cope effectively with risks of a too prolonged period of low inflation… The ECB is also contributing towards a revitalisation of the asset-backed securities market in Europe, which would be an important avenue to further support credit flows in the euro area and for the credit transmission channel.” But as we have pointed out previously, any ABS asset purchase program would not be viable until early next year, given regulatory and market size issues. What’s more, in a speech in Amsterdam in late April, Draghi indicated that, “a worsening of the medium-term outlook for inflation… would warrant a more broad-based asset purchase programme [than one comprising only purchases of ABS], without specifying what “broader” assets he meant.” Still, with an eye for recent history, one could envisage a November 2014 announcement of an asset purchase program, including ABS and other assets, to start in early 2015, and worth upwards of €800bn euro to have meaningful scale.

A stop-gap measure commencing in June would be no longer sterilising the Bank’s €172bn holdings of sovereign bonds purchased in the securities markets program from May 2010. The ECB could announce a €30bn per month program (similar in size to the Fed’s current $45bn per month APP) simply by not reabsorbing the SMP cash as it currently does by taking deposits out of the banking system. That could see the ECB “printing money” till the end of this year (retrospective QE, as it were, given the assets have already been purchased), by which time progress would have been made on re-establishing the asset backed market. The ECB would favour using its balance sheet to ease policy over interest rate cuts for a range of reasons including: the likelihood QE would tend to weaken the euro more because of its potentially unlimited size; interest rates are almost expired as an effective policy tool; purchasing asset backed securities would also address the issue of contracting lending in the Eurozone, especially the periphery, by taking those loans off bank balance sheets and making loans more attractive for banks to approve (ie it would be a targeted approach focused on a key problem). That said, we would not rule June policy easing also including an interest rate move, in part because it might add to downward pressure on the euro exchange rate. For more on the range of easing measures available to the ECB see ECB policy options and the euro response (May 7).

And there you have it…