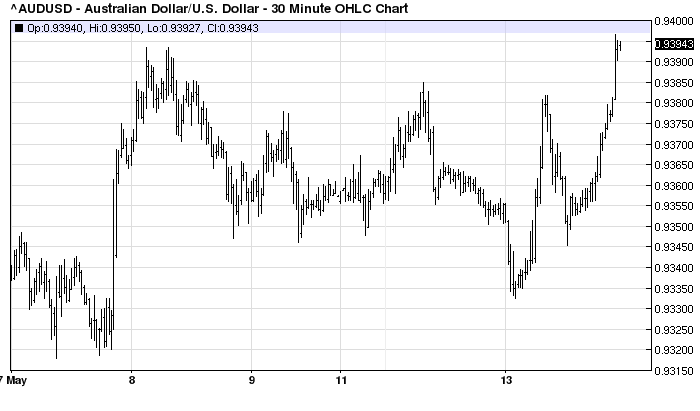

The Aussie if flying this afternoon, at a four week high, not on the Budget, but building expectations of European QE after the WSJ published this today:

Germany’s central bank is willing to back an array of stimulus measures by the European Central Bank next month if needed to fight unacceptably low inflation, underscoring the Bundesbank’s shift away from its reputation in recent years as the euro zone’s policy rebel.

The Bundesbank is open to supporting aggressive—and in some cases, for the ECB, unprecedented—steps including negative rates on bank deposits, long-term loans to banks at capped interest rates and purchases of packaged bank loans, a person familiar with the matter told The Wall Street Journal.

Mario Draghi, pictured at a news conference at the National Bank of Belgium in Brussels, May 8, 2014.Bloomberg News

The euro fell sharply on the news of the Bundesbank’s stance, which lends support to mounting expectations in financial markets that the ECB will act decisively, and with unity, on interest-rate cuts and other measures when it next meets June 5.

A little bit of backing from Martin Wolf doesn’t hurt, either:

Advertisement

Mario Draghi, president of the European Central Bank, gave a clear indication last week that monetary easing would arrive in June. That would be welcome. It would also be vastly too late and, in all probability, too little. Mr Draghi saved the day in July 2012 when he announced that “within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And, believe me, it will be enough.” He needs to promise to do whatever it takes yet again, to eliminate excess capacity and raise inflation to 2 per cent. If he does not, crisis might yet return.

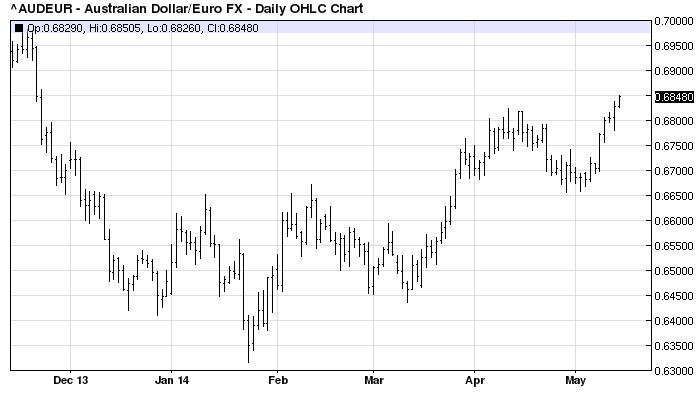

That has the Aussie flying against the euro to the highest this year:

The euro is not a renowned funding currency for carry trades but European easing can put a rocket under the Aussie. As I recall it was just this that pushed the local unit to its all time high in mid 2012.

I remain of the view that the second half will bring relief as iron ore tanks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.