Over the past few weeks I’ve noted the increasing confusion in RBA communications, aiming to be all things to all people or, as former Head of RBA Research Peter Jonson has put it, serving multiple masters.

A part of this has been the back and forth jawboning of the dollar. Late last year it was working fine, taking some 5-10% off the currency. But this the policy was dumped and the losses immediately reversed (notwithstanding other factors at work).

The basic lesson here is that jawboning doesn’t work unless one is prepared to back words with action. That’s a salient lesson as the RBA turns the focus of its jawboning to house prices.

A part of the RBA’s increasingly mixed messages has been more frequent talking down of house prices, while talking up the recovery and housing construction. Barely does a governor appear these days without making reference to the history of house prices that fall as well as rise. In the absence of macroprudential tools, the RBA appears to be aiming to prevent investor credit from accelerating too fast. Can it succeed in housing where it failed with the dollar?

The evidence is not very convincing.

First, there is the simple fact of RBA confusion. The bank looks pretty weak-kneed around house prices given it was it that egged-on the boom in the first place. And is still doing so to support construction.

Second, the drover’s dog knows that the end of the mining boom and high dollar have the bank between a rock a hard place on actual cash rate action. The jawbone looks pretty weak relative to a very obvious reality in which rate hikes will do great harm.

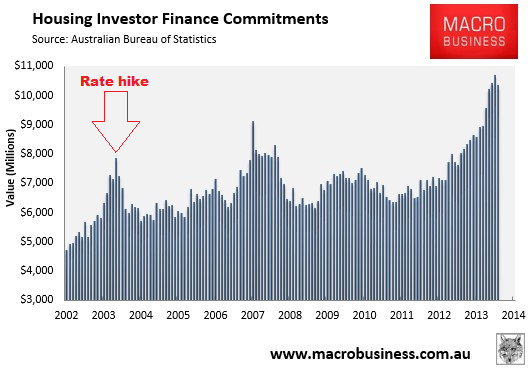

Third, if we look back at the much celebrated 2003 episode in which Ian Macfaralane’s RBA is widely considered to have popped the 2003 investor bubble, the evidence is that rate hikes were needed first. Throughout much of 2003, the RBA was sanguine about rising household debt and the investor boom. But from the August Statement of Monetary Policy there was a string of research releases, conferences, speeches and statements which intensively debated how a central bank should respond to asset prices.

The end result can be couched as a win for the Phil Lowe (now deputy governor) view of the world, that central banks should not target asset price levels but they should not be ignored in medium term projections either. From the conclusion of the RBA’s August 2003 conference “Asset Prices and Monetary Policy”:

Regarding the role of monetary policy itself, there was broad consensus at the conference that policy-makers should not attempt to target asset prices, but that they also should not ignore them. Many of the participants seemed to support the view expressed by Philip Lowe, in his comments on the papers by Bean and Cecchetti, that central banks should focus on whether developments in credit and asset markets are materially increasing financial system risk and broader risks to the macroeconomy.

The question is then how an inflation-targeting regime should take these risks into account, given the general goals in terms of inflation and economic activity. The challenge in this regard is that the risks engendered by developments in asset markets are most often low-probability, medium-horizon events that do not lend themselves to easy inclusion in standard short-term forecasts. In particular, the risk of a substantial asset-price correction may be sufficiently low or hard to quantify as to be excluded from any central forecast, particularly at a horizon of only one or two years. But that does not mean that it can be ignored. Rather, these considerations highlight the need for monetary policy to maintain a medium-term perspective and to take into account an assessment of risks to the outlook, not just the central forecast.

What followed was a series of jawboning statements from Governor Ian Macfarlane directed at housing investment, building to actual rate rises in November and December of that year.

However, if we look at the history of investor credit, it did not fall until the RBA actually jacked rates in November:

Again the lesson is that if you want to jawbone a market, you have to be prepared to follow through, and that markets will play chicken with you until you do.