I’m not one to jump on the band wagon of the confidence fairy champions. Over the stretch, consumer confidence trends are not the result of fleeting comments from politicians, single economic data points or one-off events. It is the result of a reasonable appraisal of economic fundamentals, taking in interest rates, asset prices and costs of living, wages and jobs prospects, general conditions, as well local and global narratives.

This year a great deal depends upon the consumer. With the capex cliff fast approaching and business investment set to fall very fast, there are only two sources of real activity in the economy. One is private consumption and the other is public demand (investment and consumption). If the government cuts back to the extent that its demand is flat, that only leaves the consumer. (There are net exports to add to the arithmetic of growth of course but they do nothing for real activity.)

Can the consumer bear up under the pressure?

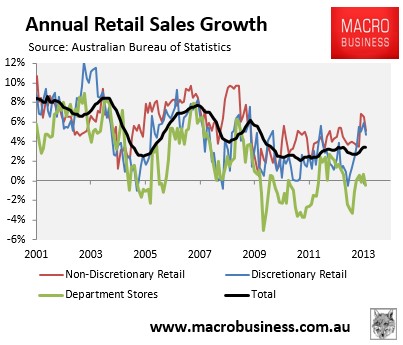

So far, the post election bounce in spending offers hope that s/he can. The RBA’s financial repression has also offered a temporary lift to asset prices to support spending and that has shown up in a solid rebound in retail spending:

Spending has jumped to post GFC highs (still low relative to history obviously) despite recent retracement. Typically, Australians are a spectacularly conformist lot so if told to spend they should do so.

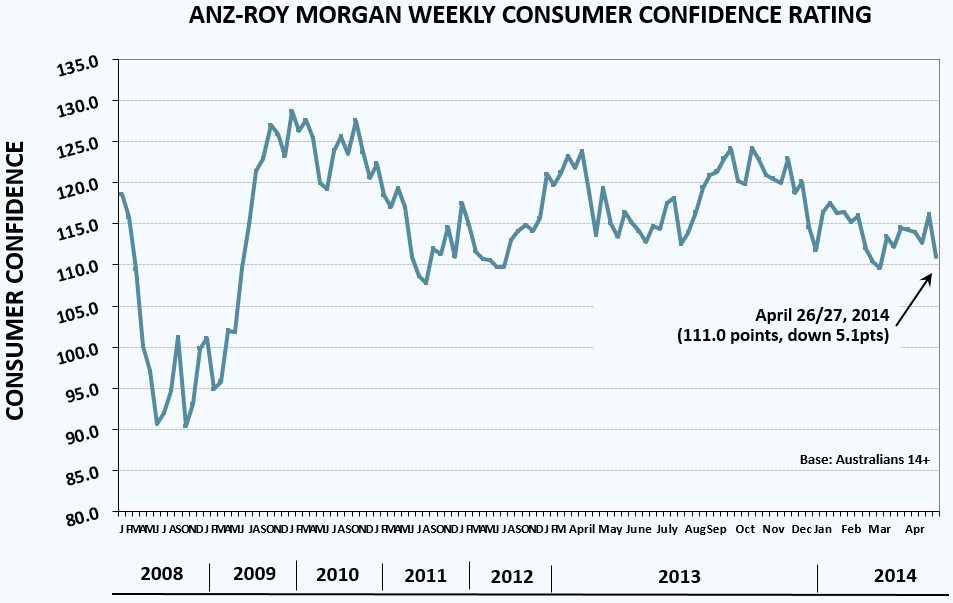

But more recent surveys of confidence are rolling badly, the most recent was Roy Morgan’s weekly reading yesterday:

We are already below levels associated with last year’s very weak spending and the big trend looks down. This is all the more noteworthy given soaring asset prices.

But is it all that surprising? If we line up the range of headwinds for the economy and the consumer’s assessment of his prospects the picture is pretty gloomy:

- rising unemployment and a generational closure of major businesses

- mining investment bust

- government austerity

- slowing China, falling iron ore and terms of trade

- stickily high dollar (which some may think is good)

- atypical housing cycle driven by investors only and spooking some into rate rise concerns

It’s enough to weigh down the hardiest of spenders.

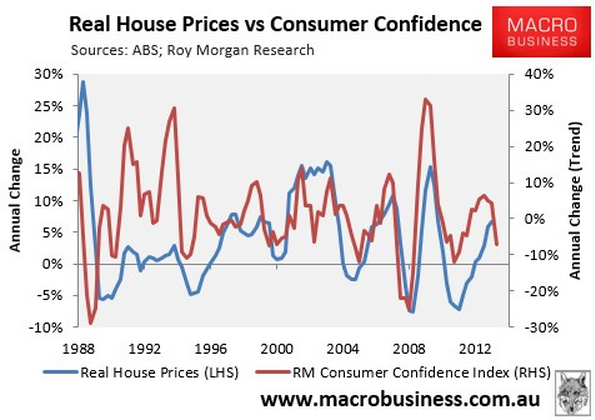

And there’s is a virtuous cycle here that could reverse too. Consumer confidence has traditionally led house price gains so any enduring consumer retrenchment may also show up in house prices before long:

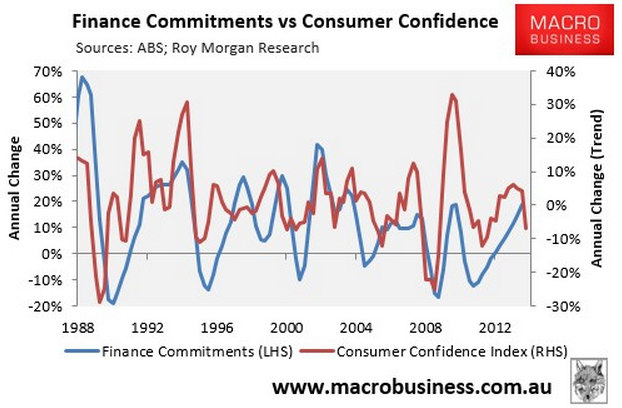

And the correlation is even more clear in mortgages:

If this relationship holds then falls to date will create a negative feedback loop and signal more rate cuts from the RBA this year. This is quite possible and the charts suggest should even be the base case.

But I’m not so sure this time around. This housing cycle has made so little sense – with little participation from household formation – that I still think it will keep running, perhaps more slowly. In fact, a fading consumer is just as likely to keep it up as rate rise fears subside. That aught to be some ongoing support for consumption.

But I would not be getting at all carried away with the households ability to carry the economy. That means you can forget interest rate rises for as far ahead as it matters and be cautious of sell side research selling retail stocks.

My best guess is that the consumer bounce is already at its peak and from here we should all be thankful if it slides only gently into more rate cuts next year.