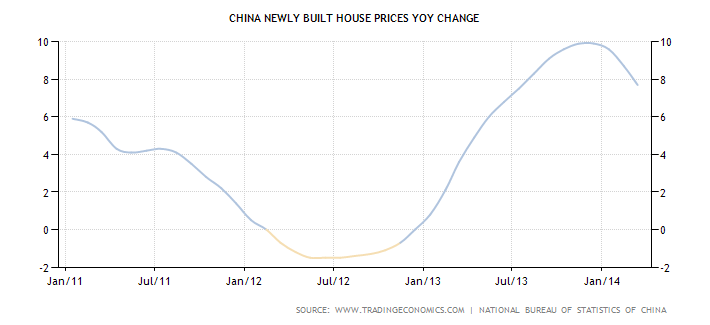

China’s home price inflation slowed to an eight-month low in March, extending to a third month a loss of momentum in a property market that has been a strong spot in the world’s second-largest economy.

Average new home prices in China’s 70 major cities rose 7.7 percent in March from a year earlier, easing from the previous month’s 8.7 percent rise, according to Reuters calculations based on data released by the National Bureau of Statistics (NBS) on Friday.

In month-on-month terms, prices rose 0.2 percent in March, slowing from February’s rise of 0.3 percent.

…”Home price rises will continue to lose momentum this year as we have seen more developers start to cut prices,” said Liu Yuan, a research head of property consultancy Centaline in Shanghai.

“However, we think the market will finally stabilize thanks to still strong demand and local governments’ possible moves to ease restrictions on home buying,” Liu said.

…”The current property market is just cooling down mildly from the red-hot situation seen in past years, which is actually quite good for the healthy development of the industry,” said Chen Guoqiang, vice chairman of China Real Estate Society, a property policy research body.

The last time we went through in 2012, authorities certainly blinked with rate cuts and a big stimulus package. One wonders how much pain they can take this time around. Over Easter, the People’s bank of China announced a new easing of reserve ratio requirements for rural banks (only), which is highly targeted (affecting only about 5% of lending). And on Sunday some accelerated energy investment was added. From the AFR:

Premier Li Keqiang announced the plans, without providing further details, at a State Energy Commission meeting last week, according to remarks released on a government website on Sunday.

While Mr Li has repeatedly ruled out a big-spending stimulus package, the government also ratcheted up its fiscal spending in March, following the unexpectedly slow start to the year. Fiscal spending jumped 22 per cent to 1.3 trillion yuan ($223 billion) last month, compared to a year ago, and almost matched the combined outlays for January and February of 1.7 trillion yuan.

The state-owned Economic Observer newspaper said Beijing had instructed local government finance departments in March to spend more money on housing and agriculture projects. In recent years, governments have tended to spend more money at the end of the year.

Advertisement

But these measures make broader easing less likely. The question remains, for how long? From Bloomieover Easter:

Citigroup Inc. sees “targeted easing” including on home purchase restrictions, while Bank of America Corp. says smaller cities may see looser rules. Centaline Group, parent of China’s biggest real-estate brokerage, says some cities are inclined to adjust policies such as the level of scrutiny of buyers.

…“The housing sector now poses the biggest downside risk to the Chinese economy,” said Yao Wei, China economist at Societe Generale SA in Hong Kong. “The next batch of policy announcements is likely to be housing policy relaxation at the local government level.”

…UBS AG estimates the real-estate industry accounts for more than a quarter of final demand in the economy when including property-generated needs for goods including electric machinery and instruments, chemicals and metals.

“For now, I think the government will hold its breath, but if the sector were to continue to weaken — and I think most forward-looking indicators suggest it will — I’d expect the government’s nerve not to hold,” George Magnus, an independent senior economic adviser in London to UBS, said in an e-mail.

Measures may include “monetary easing, including possibly further yuan depreciation, and a relaxation of some past restraints on property purchases and transactions,” Magnus said.

JPMorgan Chase & Co. said yesterday that there may be “some degree of easing in property tightening measures” such as restrictions on purchases and mortgages in markets where housing is under pressure. It’s “unlikely to evolve” into a national policy shift, Grace Ng, senior China economist in Hong Kong, said in a note.

Any loosening measures may only be minor, said Andy Mantel, founder and chief executive officer of Pacific Sun Advisors in Hong Kong. Xu Gao, chief economist at Everbright Securities Co. in Beijing, said the government should focus on loosening monetary policy to help the property market.

The pragmatists will likely be right. But the question is when does the Chinese nerve crack? All things equal in the reform process, authorities should be prepared to take the shakeout further than in 2012. In particular, they should be willing to lose some shadow banking entities and their ponzi borrowers before easing decisively.

Advertisement

And remember, this is only the current cycle within the larger structural transformation. Morgan Stanley nicely captures the larger glide path:

There is a risk that sustainable growth in China can either be at or above the 6%Y level that most investors expect, or consumption-led, but not both. Consumption growth in a consumption-led model of growth could be much lower than most expect.

The sequencing and speed of financial liberalisation (and hence the longevity of financial repression) will tilt the balance in favour of consumption-led but lower growth, or towards a path of higher growth where consumption plays a smaller role.

A happy medium with moderately high growth where consumption plays a growing role would be ideal, but could be hard to achieve if the interest rate liberalisation agenda remains in play.

Why could consumption growth in a consumption-led model be lower than most expect? For four reasons:

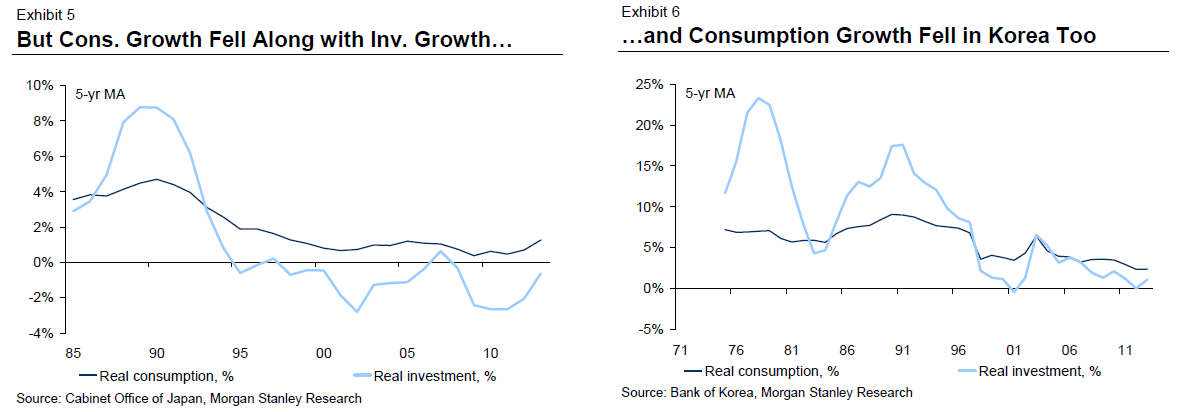

Strong investment growth in recent years has accelerated capital formation, which in turn has supported income growth and hence consumption. As investment slows down, consumption growth could come under pressure too.

For sustainable consumption-led growth, the capital stock has to be productively deployed: Capital misallocation makes it harder to generate consistent income growth and hence consumption. Put another way, capital misallocation makes it harder to generate permanent income growth. Milton Friedman’s Permanent Income Hypothesis tells us that it is permanent income growth rather than changes in transitory income which leads to an upshift in consumption.

When deleveraging is in progress, unlevered private sector balance sheets rarely see an increase in leverage: The most famous example would be that the corporate balance sheets in the US have not leveraged up despite solid balance sheets over the past few years when the household sector has been deleveraging (see Exhibits 1 and 2). In China, similarly, as over-leveraged corporates reduce their indebtedness, other unlevered corporates and households might be reluctant to increase their own leverage (see China Deleveraging: Small Steps Along a Bumpy Path, January 28, 2014). Why might this be the case? Perhaps the impact of deleveraging (from households or corporates) puts downward pressure on growth and on banks’ balance sheets, lowering both the demand for and the supply of credit in the economy.

The historical precedents for the rebalancing – Japan and Korea – also offer support to our argument. Investment/GDP fell and consumption/GDP rose as part of the ‘rebalancing’ (see Exhibits 3-6), but real consumption growth actually fell as investment growth declined.

If China opts for, or investors are banking on, consumption-led growth, the resulting level of growth may be much lower than most expect. If growth is to be sustained at higher levels, investment will have to continue to drive it, which has implications for how quickly interest rate liberalisation proceeds and interest rates rise.

Two fantastic charts there of Asian economies going “ex-growth”. One of historic success (Korea) and the other of historic failure (Japan).

Advertisement

In sum, China is on the down slope in another cycle within its larger structural descent. If the Chinese leadership is serious that means some controlled disorder in the ponzi sectors of housing, steel, ship-building etc and a significant risk of a hard landing (a quarter or two at 4% growth) before a decent rebound and then a return to the falling glide path.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.