The Reserve Bank of New Zealand’s (RBNZ) Michael Reddell has written an interesting paper questioning the merits of New Zealand’s high immigration program, which appears to have crowded-out (through higher interest rates and a high average real exchange rate) other productive investment, lowering living standards in the process:

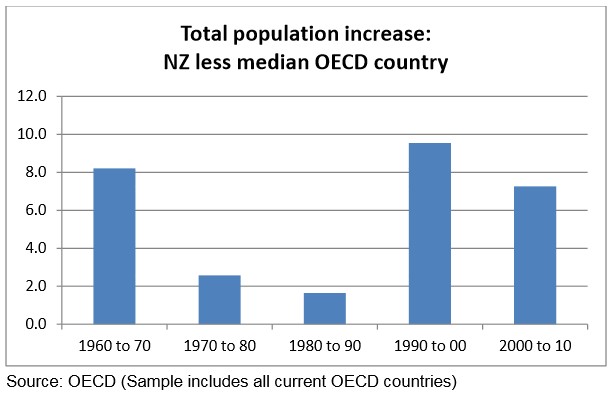

Over the last 50 years (and more) New Zealand’s population has mostly grown materially faster than the populations of other advanced countries…

All else equal – and in particular for an unchanged savings rate – faster population growth (especially relative to that abroad) means that some other investment that would otherwise occur will tend to be crowded out to make way for the infrastructure (private and public) needs of the increased population. This is not some central planner’s response, but how the market respond to the demand created by the additional population – it crowds out spending that is relatively more sensitive to changes in real interest and exchange rates. Typically, that will be business investment, especially that in the tradables sector.

In such a situation, the total capital stock will still be growing, perhaps quite materially, but the capital stock per capita, or per worker, will be growing less rapidly than it would otherwise have done…

After the period of very subdued population growth, New Zealand’s population growth accelerated rapidly from the early 1990s and, relative to other advanced economies, the pace remains strong. Public policy played a decisive part in the change – it is not just a matter of the free exercise of individual New Zealanders’ preference (either through having more children, or choosing to stay rather than leave New Zealand).

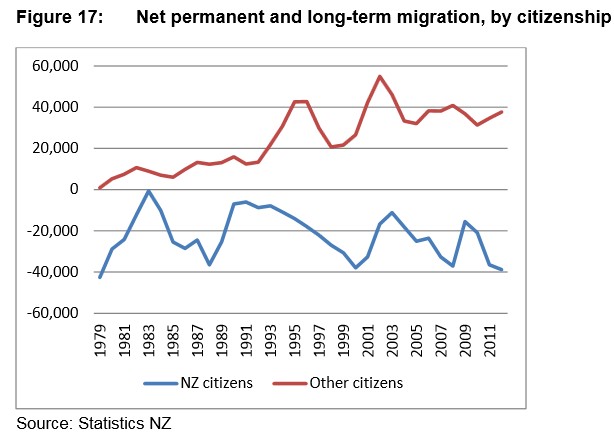

Immigration policy was markedly reshaped and liberalised in the late 1980s and early 1990s. In macroeconomic terms, the most important element of the change was the very substantial resulting increase in the net inflow of non-New Zealanders…

Taking the period as a whole, it is likely that the markedly increased net inflow of non-New Zealanders – a new wave entering each and every year – has extended and exaggerated the degree to which our average interest rates have exceeded those of other advanced economies. That, in turn, will have extended and exacerbated the persistent severe average overvaluation of the real exchange rate. In that sense, government policy has tended to directly, if inadvertently, stymie the rebalancing and adjustment that private citizens’ choices would otherwise have brought about.

Had that net outflow experienced in the 1970s and 1980s continued over the last two decades, the resources that had to be devoted to the housing (and the other population-driven components of the capital stock) demands of a fairly rapidly rising population would have been free for other uses. Other things equal, we might have expected to have seen rather lower real interest rates and a lower real exchange rate. The prospects for “capital deepening”, and for associated improvements in labour productivity and MFP, made possible by the other reforms and liberalisation of the late 80s and early 1990s, would have been materially enhanced.

If, say, the same ratio of total investment (gross investment to GDP) had occurred, it would have involved materially less house-building and less government infrastructure investment. On the other hand, private business investment, which is much more sensitive to expected economic returns, would have made up a much larger share of total investment. Within business investment it is likely that there would have been a stronger skew towards investment in the tradables sector to take advantage of the opportunities created by a lower exchange rate and the generally fairly good business regulatory environment…

Internationally, there is no evidence over the last century that countries with faster population growth, or greater inward migration, have achieved faster income or productivity growth than

other countries…

With modest savings, and a large net outflow of New Zealand citizens, it looks quite anomalous for policy to have been designed to induce large net inflows of people from other countries. I suspect it looks anomalous for good reason – given the specific circumstances of New Zealand, and the aspirations towards convergence, it was not very good policy…

Low population growth of the sort we saw in the late 1970s and 1980s would have provided a good platform to maximise the per capita income benefits of the wide-ranging reform programme, especially in a country with a modest savings rate. Instead, immigration policy reforms had the effect of sharply reaccelerating population growth, at just the time when the focus might more naturally have been on lifting per capita income rather than total GDP…

The indications that countries with faster population growth have in recent decades devoted fewer resources to non-housing investment and have seen less growth in multi-factor productivity are sobering. They provide another straw in the wind, suggesting caution about the merits of continuing large inward immigration to New Zealand for the time being…

Had the inflow of (well-chosen) non New Zealanders been kept to the aggregate levels seen in the 1980s, it is almost certain that over the last couple of decades New Zealand real interest rates would have been closer to those in the rest of the world, and the real exchange rate would have been materially lower. (House prices would have been lower, and) if real interest and exchange rates had been lower then per capita incomes would most likely have been materially higher…

Advertisement

Reddell’s paper follows analysis completed earlier this month by the New Zealand Treasury, which questioned the merits of high immigration, and recommended a reduced immigration intake in the event that the economy is unable to adequately cope with population pressures.

It also follows a 2011 report by New Zealand’s Savings Working Group, which also supported the notion that high levels of immigration tend to put upward pressure on inflation and interest rates, which can crowd-out productive sectors of the economy.

As argued many times on this blog, a big negative of high rates of immigration is that it places increasing pressure on the pre-existing (already strained) stock of infrastructure and housing, reducing productivity and living standards unless costly new investments are made, which in turn chokes-off other productive investment.

Advertisement

Indeed, as explained in a 2011 speech by the Reserve Bank of Australia’s Phil Lowe (summarised here), rapid population growth (immigration) since the mid-2000s has placed upward pressure on rents, as well as caused a big surge in utilities prices as the capacity of the system struggled to keep pace with the growing demand, requiring costly new investments.

Any objective examination of the facts suggests that the case for a high level of immigration is anything but clear-cut and those advocating a strong migration program need to justify their position.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.