The Reserve Bank of New Zealand (RBNZ) has released its quarterly bulletin, which contains a frank assessment of its macroprudential caps on high loan-to-value ratio (LVR) mortgage lending. Its conclusion? That the LVR caps have probably reduced New Zealand house prices by around 2.5%:

It will be some months before the impact of LVR restrictions can be reliably gauged.

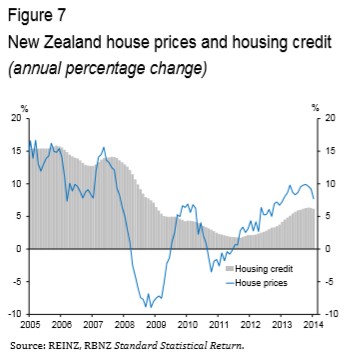

However, from an effectiveness point of view, the early evidence suggests that LVR restrictions are having the desired impact on house prices and credit growth. The housing market has weakened, with seasonally adjusted house sales down by around 13 percent over the five months to February, and nationwide house price growth easing to 8.2 percent over the year to February compared to 9.8 percent over the year to September (figure 7).

Survey data also suggest that expectations of continuing house price increases are softening. After trending up since June 2011 (when the survey began), households’ expectations of higher house prices appear to have stabilised (figure 8).

The weaker housing market is reflected in housing lending data. This is particularly evident in the first stage of the lending process, with the value of new housing loans approvals falling by a seasonally adjusted 7 percent over the three months to February. Changes in housing credit are slower to come through, reflecting that net credit is also affected by drawdowns on existing loans, and changes in repayment behaviour. Housing credit growth does appear to be turning however, having slowed from its October 2013 peak of 6.4 percent annual growth to 6 percent in January 2013.

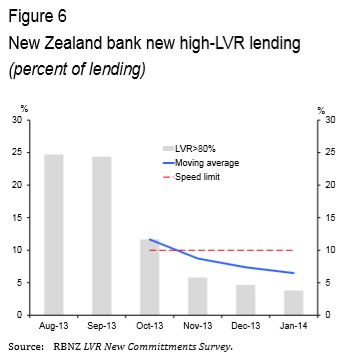

There have also been some marked changes in the pricing of housing lending, with banks now pricing for the higher risk and capital requirements associated with high-LVR lending. Banks have broadly increased the use and level of low equity premiums, and are offering discount rates on low-LVR lending. This created an initial pricing wedge of up to 100 basis points between high-LVR and low-LVR loans.

In assessing the impact of LVR restrictions, the Reserve Bank considers both actual developments in house prices and credit growth (as outlined above), and counterfactual developments; e.g. what would the likely path of housing credit and house prices be in the absence of LVR restrictions? This counterfactual modelling accounts for changes in key factors such as interest rate movements and net migration, but given the many other moving parts that also make up the financial system and economy, it is not possible to be too definitive around the results. That being said, the Reserve Bank’s counterfactual exercises suggest that house price inflation would have been around 2.5 percentage points higher in the year to February in the absence of LVR restrictions.

The RBNZ also notes that supply-side reform is key to mitigating New Zealand house prices, but that it could take some time to implement, thus necessitating its short-term demand-side response via macroprudential.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.