For the third day in a row we’ve got a marginal indicator on the slide. Following the PMI and the NAB online sales index, the PSI has als0 slumped:

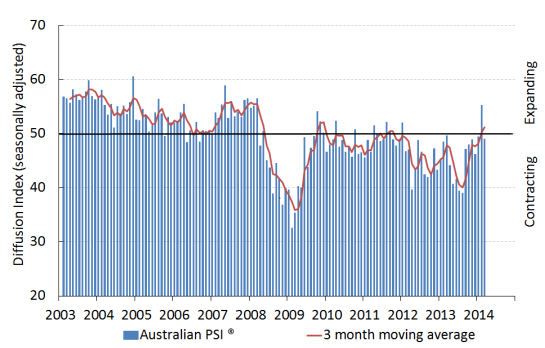

The latest seasonally adjusted Australian Industry Group Australian Performance of Services Index (Australian PSI®) dropped by 6.2 points to 48.9 points in March. This followed a strong expansion in the Australian PSI® (a reading above 50 points) last month. The weaker result this month result was evident across all sub-indexes except the new orders sub-index, which remained above 50 points (indicating expansion).

Although the sales sub-index of the Australian PSI® fell by 9.1 points in March, at 49.7 points it retained the gains made in the previous two months of expansion (above 50 points).

The services employment sub-index contracted this month indicating continuing caution by employers about the near-term outlook.

Growth continued to be concentrated in just a few services sectors, primarily health and community services (66.9 points) and finance and insurance (62.6 points). Personal and recreational services (52.5 points) expanded for the first time since July 2013, but the index for the large retail trade sub-sector declined by 1.8 points to 47.7 points (3 month moving averages).

The other, more business-oriented, services sub-sector indexes improved in March but remained below 50 points, indicating ongoing contraction (3 month moving averages).

Feedback from businesses participating in the Australian PSI® this month indicates that conditions remain challenging for many service businesses. In particular, concerns over the domestic economy and uncertainties surrounding potential spending cuts in the Federal and state budgets have reportedly dampened demand for services.

The steep falls in consumer confidence are beginning to show up in activity. The year appears to be playing out as expected, with the post-election and Christmas bounce fading to a dour reality but I’d like to see tier one data confirm that.

Today’s retail sales may prove to be a test for the Aussie.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.