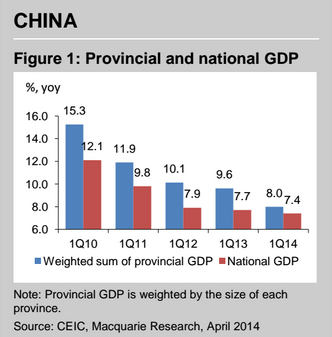

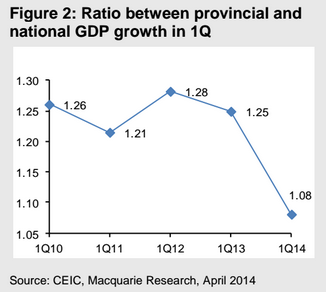

Local governments turn more conservative in reporting GDP. Up until April 28, all provinces in China except Shaanxi had reported 1Q14 GDP growth figures. Weighting them by the GDP level of each province, we get 8.0% yoy in 1Q14, compared with the 7.4% national GDP growth from the NBS (Figure 1). In the past four years, the ratio between these two has never fallen below 1.2 (Figure 2). Does this mean China only grew 6.5% in 1Q14?

We don’t think so. A more plausible explanation is that local governments began to systemically reduce the over-reporting of their growth figures. Why?

Deleveraging as the top priority for local governments: Local officials used to engage in a tournament competition for GDP growth, resulting in a fast accumulation of local government debt (~30% annual growth). Since last Dec, local officials seem to sense the pressure for deleveraging from Beijing.

Consequently, they are turning more conservative in playing the old game as higher growth often entails faster debt accumulation. Moreover, the national debt audit last year made it harder to attribute newly raised debt to their predecessors. As the result, 23 provinces lowered their growth target for 2014 and only one province (Guangdong) raised it. Even so, in 1Q14, all provinces in China except one missed their new growth targets.

It’s a change for the better, but could it last? We tend to give the benefit of doubt at this moment, but only time will tell. First, if growth falls below 7%, Beijing may have to get local governments involved in stimulating the economy; Second, the recent slowdown in some resource-intensive provinces may force them to return to the old track; Third, to compete for promotion, local officials always face the temptation to achieve higher growth by leveraging up, and they may take notes from the front-runners.

Who are the front-runners in 1Q14? They are Chongqing (10.9%), Guizhou (10.8%) and Tianjing (10.6%). This is not surprising, as they have been the fastest in the past five years. Tianjing has become the national growth champion since 2010, driven by fast investment growth. From 2008 to 2013, the annual investment growth was 30%, 9% and 5% in Tianjing, Beijing and Shanghai, respectively. Guizhou is another investment-driven story, with the highest FAI growth rates across all provinces in 2012, 2013 and 1Q14.

Chongqing is featured as an emerging export machine (mostly processing trade). From 2010 to 2013, the average annual export growth for Chongqing was 89%. In 1Q14, Chongqing’s exports grew 66% yoy, compared with -3.4% at the national level.

Resource-intensive provinces are hit heavily in 1Q14, including Heilongjiang (to 4.1% in 1Q14 from 8.0% in 2013), Hebei (to 4.2% from 8.2%) and Shanxi (to 5.5% from 8.9%). These are provinces intensive in resource, specializing in oil, steel and coal production respectively. It’s in line with the industrial profit data released over the weekend, pointing to a soft upstream, mixed midstream and held-up downstream sectors.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.