Ever since Chinese authorities committed to higher growth earlier this year, they’ve largely backtracked and fudged by emphasising quality over quantity, as well as the importance of the labour market over headline growth. Premier Li Keqiang has said China can tolerate lower growth as long as employment figures are solid. Today the Chinese National Bureau of Statistics did so again. From MNI:

The government’s response to this report is the key question for investors. Premier Li Keqiang said last week that his government won’t respond to short-term economic volatility with major stimulus measures. That appeared to rule out the kinds of response measures that investors came to expect under the Wen Jiabao government, including reserve requirement cuts.

That doesn’t mean Beijing will remain totally inactive as growth slows, but the labor market is key. The NBS said again Wednesday that the government is comfortable with labor market conditions in the first quarter, suggesting that it isn’t planning to do anything dramatic on the policy front for now. The State Council has already announced steps to support growth, though the nature of the very modest fiscal spending measures announced imply that officials hope to boost activity through words, more than action. That could change, if the March headline indicators suggest an ongoing slowdown through 2014, and particularly if jobs are affected. Until that comes through the data, however, Beijing may be in wait-and-see mode.

COMMENT: National Bureau of Statistics spokesman Sheng Laiyun says over 3 million new jobs were created in urban areas in the first quarter, more than the same period of last year. Unemployment is stable. Migrant workers working more than six months away from home grew 1.7% to 2.88 million in the first three months. He cites NBS survey showing companies complaining about difficulties in finding employees so Q1 labor market survey shows conditions are improving.

According to Nomura, this is unbearable:

…Zhang Zhiwei said the government was “constrained” by its official GDP growth target of “about 7.5 per cent”, and would be forced to act if growth slowed further. Most analysts expect economic growth to dip further in the second-quarter, even to levels testing 7 per cent. China’s leaders have said maintaining growth of at least 7.2 per cent would be required to keep employment levels steady.

“It’s going to be hard for them to tolerate growth below 7 [per cent],” Zhang says.

“In that sense the economic growth is a binding constraint, even if unemployment is not a big issue.”

China doesn’t mind missing its growth targets. After all, it missed them just about very year to the upside in the past. It’s not beyond the realms of possibility that it’ll now happily miss them the downside so long as the labour market is stable. That is, after all, what China is telling us…

Or, is the PBOC already loosening? The People’s Bank of China yesterday launched a massive liquidity drainage operation that was shrugged off by money markets:

China’s key money rates fell on Tuesday morning as dealers in the interbank market ignored a massive 178 billion yuan ($28.62 billion) drain by the central bank during open market operations, the largest single-day drain since February.

…Traders said there was enough liquidity in the market to keep downward pressure on rates, even as the People’s Bank of China (PBC), the central bank, vacuumed up excess cash.

“The market reaction to the drain wasn’t much, because actually money’s not in short supply, and in addition if you look at the auction of deposits this morning, the net effect was a cash injection,” said a dealer at a city commercial bank in Shanghai.

Zhou Hao, an economist at ANZ Bank in Shanghai, said that the market was waiting for aggregate money supply data, and predicted that the PBC would keep rates low if new loans and M2 growth come in below expectations.

“While the size of repos is larger than expected, the Ministry of Finance auctioned 6-month RMB 50 billion deposits at 5.0 percent, 100 basis points lower than the last auction of the same tenor in January, which has eased market concerns of liquidity withdrawal,” he wrote in an e-mail to clients on Tuesday.

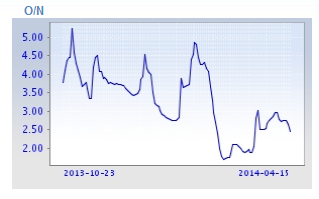

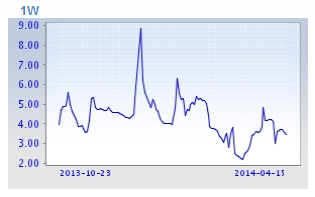

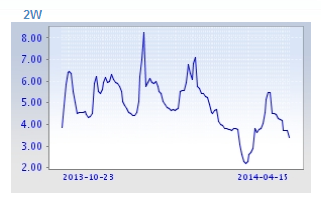

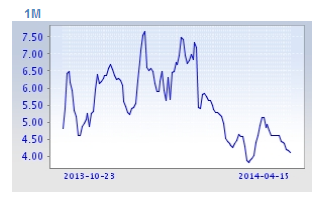

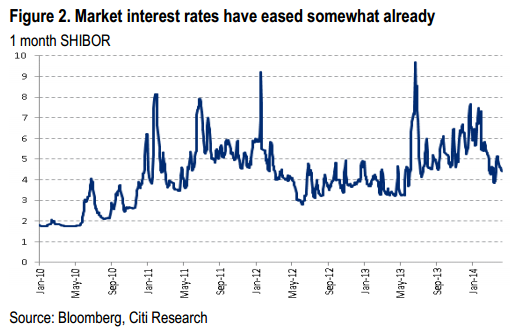

It sure has. SHIBOR rates are tumbling:

But March lending was weak despite softer SHIBOR rates than last year:

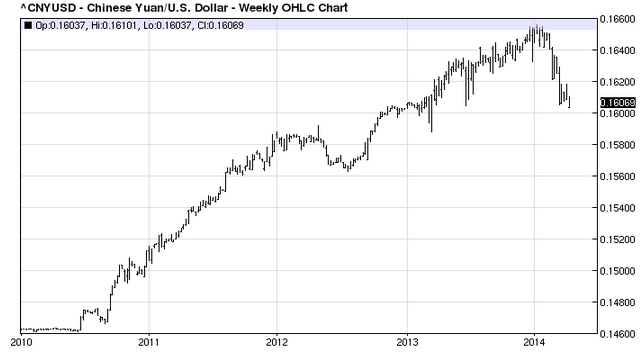

Adding to the puzzle, the PBOC keeps fixing the yuan lower and lower which chokes off credit:

It’s not clear just now whether demand for loans is lousy or the PBOC is pushing credit again.