Former Governor of the Reserve Bank, Ian Macfarlane, today goes to bat for his employer, the ANZ, in a submission to the conflicted Murray Inquiry. From The Australian:

In a personal submission to the financial system inquiry, made in his capacity as an ANZ non-executive director, Mr Macfarlane questions why the Australian Prudential Regulation Authority seems “so keen to exceed the international norm”.

“This overachievement is most apparent in the extremely stringent definition of capital applied in Australia,” he says.

The former RBA governor echoes some of ANZ’s criticisms in its submission, particularly the requirement for Australian banks to deduct from their capital ratios the entire equity position they own in listed overseas banks.

…Mr Macfarlane is also critical of the classification of the four major banks as systemically important financial institutions, which he says is “unhelpful” in a number of ways. He says the requirement for these banks to add an extra 1 per cent on to their capital ratio applies a capital penalty to the largest and most secure banks — the ones that depositors moved to in the global financial crisis.

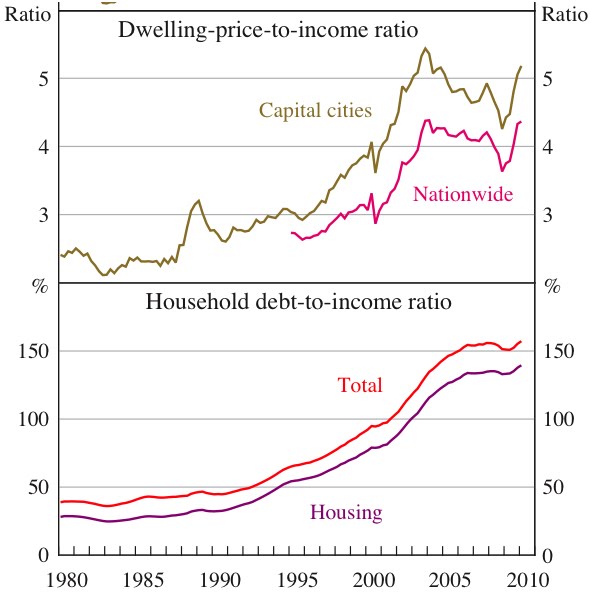

A little history here is germane. Ian Macfarlane is not a hawkish economist. His tenure at the RBA oversaw the rise of the great Australian credit surge, which dates from his appointment in 1996:

The low interest rates that triggered the credit surge can be partly blamed on the conditions of the time. There was a new Conservative government from 1996 as well, which set about crimping fiscal outlays to pay down debt. And Australia was still enjoying its productivity surge from the reforms of the late eighties through the mid nineties. From mid 1997 we also faced the Asian financial crisis, which played a role in keeping interest rates low right through until the early 2000s.

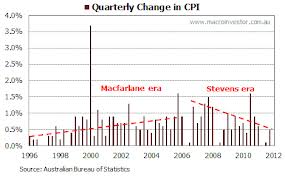

But, by way of comparison, when, in 2000, Australia faced four consecutive quarters of GST-induced inflation above 6%, official rates peaked at 6.25%. Whereas, in 2008, under Glenn Stevens, when Australia faced three consecutive quarters of commodity-price induced inflation from 4.5% to 5%, rates peaked at 7.25% with another 50 basis points added for real rates as banks widened the spread.

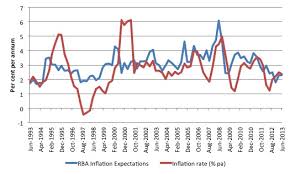

Indeed, the greatest achievement of the Stevens RBA (to date) has been unwinding the high inflation propensity accumulated under Macfarlane. Inflation expectations were 2.5% when began and nearer 4% when he left. Inflation itself was roughly 1.5% when he arrived and nearer 4% when he left:

In short, the Macfarlane period is the one in which credit and financial services moved to the heart of the Australian economy and witnessed the creation of too-big-to-fail banks, which today he wants to hide lest it distort perceptions of stability. Well, sorry, Mr Macfarlane, it’s reality that’s doing that.

One can only observe, wryly, that this is best seen as a plutocratic parlour game. The opaque internal risk weighting models that determine major bank capital are invisible to us plebs anyway and APRA has already allowed the banks to game the DSIB rules.

The great likelihood is that what we are really discussing is how little capital the banks can carry so that the dance of the elites can go on.