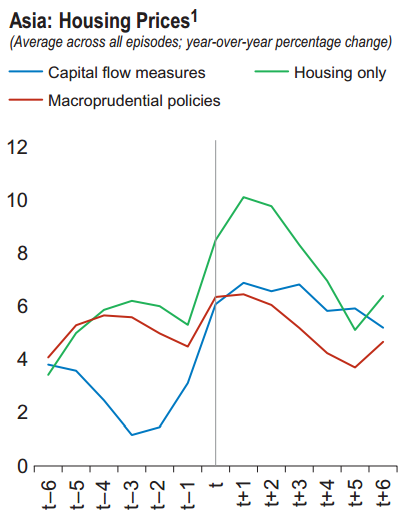

The IMF is out with its regional report on Asian economies and it included an examination of the efficacy of macroprudential tools in Asia. It finds attempts to offset capital flows were pretty useless but on housing it worked well:

Macroprudential instruments have been used more extensively in Asia than in other regions. This has been particularly true of measures related to the housing market. By contrast, Asian economies, which have comparatively less open fi nancial accounts, have taken a smaller number of measures than others to discourage transactions in foreign currency and

residency-based CFMs.

MPPs and CFMs have sometimes been used as a counter-cyclical tool. Usually they have been used to dampen the macroeconomic and fi nancial stability risks associated with large capital infl ows, but they were also used countercyclically in 2009 with policies loosened as the global fi nancial crisis unfolded.

Housing-related macroprudential instruments have had an impact—particularly caps on loan-to-value ratios and the taxation of housing transactions. In particular, such instruments have helped lower credit growth, slow house price infl ation, and dampen bank leverage in Asia (although the latter effect is quite small).

There appears to be little evidence that nonhousing related macroprudential policies and CFMs have had a systematic and measurable effect on lending, leverage, or portfolio infl ows in Asia. However, these policies may have had an impact on the distribution of risks in the fi nancial system and the resilience of the system in the face of systemic pressures. For example, foreignexchange- related measures can contain currency and liquidity mismatches, without having a strong impact on loan growth or asset prices.

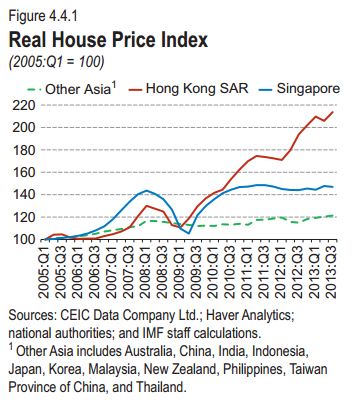

In particular, Singapore and HK have had success, though given the size of the latter’s housing bubble one wonders if it did enough!

Singapore and Hong Kong SAR—the two regional fi nancial centers in Asia—have relied extensively on macroprudential policies targeting the housing sector in recent years. The use of these tools intensifi ed after 2009, following a sharp rebound in real housingprices and a surge in mortgage loans. Between 2009:Q2 and 2011:Q2, real house prices in Singapore went up by more than 40 percent, though they stabilized afterward (Figure 4.4.1). Real house prices in Hong Kong SAR rose by about 90 percent from 2009:Q1 to 2013:Q3, while toward the end of 2013, prices started to level off in nominal terms.

Several factors have played a role in driving house prices in these economies. The supply of housing is rather inelastic and is mainly driven by public land auctions, contributing to lags in supply expansion. In parallel, strong income growth and persistently low interest rates after the global fi nancial crisis supported domestic demand for housing.2 Foreign investors further boosted demand for real estate.

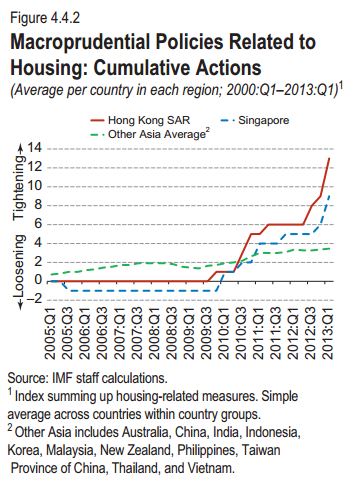

A wide range of macroprudential policies have been used to enhance fi nancial stability amidst rising house prices and credit growth (Figure 4.4.2). LTV limits have been tightened (that is, lowered) sharply in both economies. While Singapore has used LTV limits to target second (and plus) mortgages and mortgages with high tenors, Hong Kong SAR targeted all mortgages, applying tighter caps to luxury properties, investment properties, and borrowers with sources of income from abroad. Hong Kong SAR has also tightened the DTI ratio limit, which had been introduced back in 1997, while Singapore adopted a DTI limit in 2013. Hong Kong SAR further imposed higher risk weight requirements for mortgages. Real estate taxes and loan tenor limits have also been used in both economies. For example, in Hong Kong SAR stamp duty measures were introduced to cool down the housing market in 2010, 2012, and 2013.

Macroprudential policies have contributed to cooling down somewhat the housing market in both economies. In Singapore, after the introduction of LTVs, the share of borrowers with single mortgages increased, and speculative transactions fell. For Hong Kong SAR, empirical evidence suggests that the changes in LTV limits helped reduce transaction volumes and slowed house price infl ation (Ahuja and Nabar, 2011). LTV limits also dampened borrowers’ leverage and credit growth and lowered the impact of a property price correction on mortgage default risk (Hong Kong Monetary Authority, 2011; Wong, Tsang, and Kong, 2014).

Both countries have also had periods where they loosened their macroprudential policies. Singapore lowered stamp duties during the Asian crisis as the macroeconomic environment deteriorated. In addition, as housing markets weakened, Singapore eliminated the capital gains tax during the 2001 recession and raised the LTV ceiling in 2005. In Hong Kong SAR, the LTV limit for luxury properties was tightened in 1997 and then reversed in 2001 as prices collapsed. However, recalibrating macroprudential tools maybe more complicated in the current juncture, given the need to coordinate a much broader and more extensive set of measures now in the system.

Advertisement

The Singapore study especially suggests that MP tools might be used successfully to slow a housing market without crashing it, though wider economic conditions would need to be factored in. Full report here.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.