The AFR has an interesting piece on the ongoing conflict between LNG buyers and sellers over pricing regimes:

The head of Japan’s quasi-national oil company Inpex Corporation fears a “lose-lose” result in the global liquefied natural gas market unless producers and suppliers resolve their differences over supply, demand, and pricing.

Toshiaki Kitamura will tell the Australian Petroleum Production & Exploration Association conference in Perth on Monday that should a consensus on those factors not be reached the development of a “healthy” global LNG market will be delayed.

“To convert such a negative situation into a “win-win” outcome, close coordination between LNG suppliers and buyers is needed,” Mr Kitamura will say.

…Chevron has said it won’t move ahead with new LNG projects such as Kitimat LNG in Canada or an expansion of Gorgon in Western Australia without appropriate long-term contract pricing.

…Mr Kitamura will acknowledge the need for suppliers to lock in long-term contracts with a “bankable” pricing formula to justify the huge investment required in projects.

However he will say that for buyers, the priority is to “diversify their LNG pricing formula.”

Sensible enough but not possible for Australia’s super expensive magnificent seven which occupy the cost curve from $12 to $14. Sadly for them it will still have happen through pain given they’re the marginal producer, a view endorsed by an Ernst and Young report today:

The last few years have seen a record divergence in regional gas prices, driven by both supply and demand factors, including the US shale gas boom, the European financial crisis and the Fukushima nuclear crisis. In addition to regional price differences for natural gas, the oil and natural gas price differential has dramatically decoupled from an “energyequivalency” basis. The advent of diverse potential new supply sources is challenging the LNG status quo, with Asian buyers presumably looking to modify or possibly replace their long-standing and relatively expensive pricing model of gas prices tied explicitly to oil prices.

Typically, high LNG development costs have generally required ironclad long-term off-take agreements —

agreements that have historically been oil price based. Recent high oil prices and oil-indexed LNG contracts have

resulted in high LNG prices for Asian buyers that — to those buyers — appear much higher than what North American natural gas prices would suggest should be the case. The market is now witnessing the inherent conflict of increasingly more expensive projects trying to sell to increasingly more price-sensitive buyers. High oil prices and low natural gas prices (in North America, at least) have strained the traditional “oil-indexation” LNG pricing approach. Asian buyers assert that oil-indexed LNG prices are untenable, while LNG project developers argue that contracts based on the current low North American price for natural gas will not create acceptable project economics (or support the further development of unconventional gas resources).

In theory, oil indexation of gas contracts will become more difficult with greater competition between sellers, more price-sensitive buyers, growing energy deregulation, more gas-on-gas competition from new pipeline infrastructure, increasing spot market liquidity and, most importantly, increasing availability of spot-price-based LNG exports.

Developers of higher-cost projects will find it more difficult to protect their returns through contracts that do not reflect the realities of spot price pressures.

More realistically however, the current supply side of the LNG business — including most, if not all, projects under construction — needs to be assured that it will be able to achieve a netback (i.e., after shipping costs) of about US$10 to US$11 per million BTUs, or about US$12 to US$13 per million BTUs delivered. Given a broad assumption that long-term oil prices average between US$80 per barrel to US$90 per barrel, this would imply that sellers would seek oil-linked contracts with slopes in the range of 14% to 16% — approximately where they currently are.

But the possibility of spot gas-linked contracts from North American LNG could upset the traditional pricing structure. Using the notional terms of some of the proposed US export contracts, the attractiveness of “Henry Hub plus” pricing becomes apparent, both to buyers and sellers: buyers accessing supply not linked to high oil prices, and sellers opening margin opportunities compared to domestic North American markets.

Where do “spot” and “oil-indexed” prices converge?

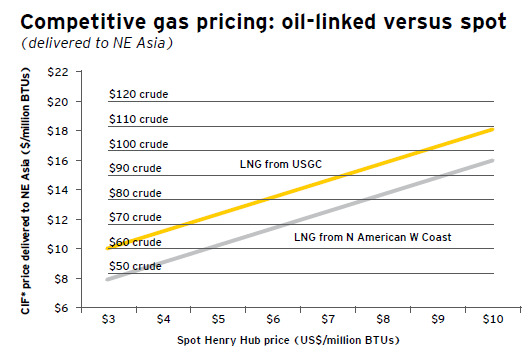

The charts on the next page are intended to set out a simple comparison of the deemed prices for LNG cargos from North American LNG projects at a variety of oil and natural gas price points on an “energy equivalent” basis. For example,

US$5 per million BTU Henry Hub natural gas prices translate into US$10 to US$13 LNG prices into Asia (after accounting for liquefaction and transportation cost estimates) which on an energy equivalent basis equates to oil prices ranging from US$60 to US$75. Thus, buyers who have access to lower priced US LNG would have attractive supply alternatives and

could capture some of the implied margin/arbitrage, and/ or these buyers would have some leverage with oil-linked sellers, as long as those oil-linked prices for LNG were above

the nominal energy equivalent price range.

Alternatively, current Asian LNG prices in the US$16 to US$18 per million BTU range (calculated on an oil-indexed basis) suggest that buyers would be willing to buy at implied Henry Hub natural gas prices in the US$8 to US$10 range.

Thus, LNG sellers (either producers or portfolio players) with access to supply at prices below this implied energy equivalence level, could seemingly capture some of that margin/arbitrage.

In short, for both LNG buyers and some sellers, the arbitrage opportunity available by linking to current Henry Hub

spot prices (and in fact against many of the longer-term natural gas price forecasts which remain in the US$4 to US$6 range) is clear.

Our notional costing model reflects the terms of the early US LNG export projects, all of which are brownfield projects that leverage many of the sunk costs from those projects’ earlier lives as LNG import facilities. While we use an uplift factor of about US$7 per million BTUs for Gulf Coast LNG to Northeast Asia, to account for liquefaction and transportation, this amount may be insufficient to cover the costs of the proposed greenfield projects, and it may not be sufficient to cover any or all necessary costs upstream of the spot-hub.

Given that all Canadian projects are greenfield projects requiring significant infrastructure investments, the notional FOB costs for proposed Western Canada LNG exports are assumed to be modestly higher than those for US Gulf Coast exports. However, it is expected that shipping costs to Asia will be lower as a result of the significant “distance advantage” enjoyed by the West Coast projects. At the present time, it is unclear whether/how the full upstream costs of Canadian LNG will be reflected in LNG prices, as opposed to simply basing prices on spot prices similar to the merchant US projects.

As substantial volumes of lower-cost LNG move into Asian markets, projects at the high end of the supply curve — namely, many of the Australian projects — will become increasingly vulnerable, with at a minimum, situations arising where sellers may be forced to re-open or renegotiate contracts.

A similar analysis for shipments into Europe from the US Gulf Coast shows the implied pressure that spot-based contracts could put on oil-linked sellers. As shown below, US LNG at US$5 per million BTUs would remain competitive with oil linked contracts down to about US$60 per barrel. Spot pricing increases buyers’ choices, adds liquidity to markets, and allows buyers to hedge financially and physically. The historic justification of oil linkages was the security of supply, but with increasing liquidity in the LNG market, some of the security “premium” becomes harder to justify (and perhaps unnecessary). Growing liquidity also gives suppliers confidence to sanction projects before locking in off-take agreements − resulting in the emergence of major portfolio LNG players.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.