A couple of forex comments today from the sell-side. Credit Suisse is bullish in the short term:

The 61.8% retracement resistance at .9334/38 is capping for now, but we still look for an eventual break higher to our .9410/.9510 basing target. AUDUSD remains in a high level range this week as it consolidates recent gains. Price support at .9218/13 is intact, though and with the rising 13-day average at .9178 fast approaching we look for a turn higher above .9338 to test our core basing objective at .9410/.9510. With the 38.2% retracement of the entire 2011/2014 bear trend just above at .9584, we would look for a fresh top here. Support shows at .9218/13 initially with firmer levels at .91/41/38 expected to hold to keep the trend higher.

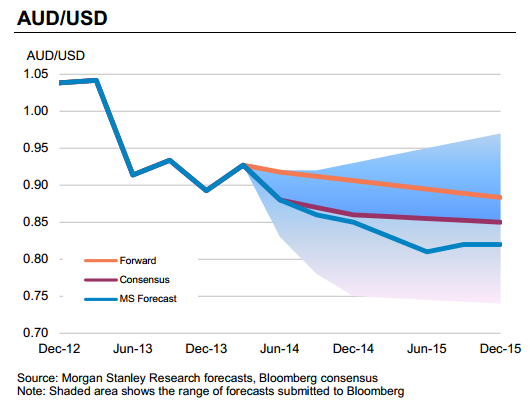

And Morgan Stanley on the long term:

In the near term, AUD is likely to outperform for two reasons.

First, given that AUD used to act as a proxy hedge for China risks, with many investors now expressing bearish China views through CNH, AUD should remain supported as these hedges are unwound. Second, Australian bonds have returned to favour by the Japanese investment community as seen in the below exhibit. Indeed, as the RBA moved away from its easing bias, Australia’s AAA-rated debt has become more attractive to overseas investors; the Japanese have now bought Australian bonds for four straight months.

That said, we like using AUD rallies to sell the currency, as we believe that AUD will be structurally weak over the medium term. Indeed, there are big changes currently occurring in China; not only is the government attempting to rein in lending and prevent excessive hot money inflow, but it is also moving towards establishing a sustainable growth model less dependent on investment, exports and leverage. As this transition occurs, Chinese growth is set to slow; such developments will disproportionately affect Australia, given the country’s heavy reliance on exports into Asia’s largest economy, we think.

Additionally, as China rebalances its economy away from manufacturing/export dependence, and towards a more balanced growth strategy involving domestic demand, China’s import basket will change significantly. Demand for industrial metals should fall, weighing on Australia’s terms of trade, which we believe will weigh on AUD valuation.

On the policy front, given the economic transition occurring not only in Australia, but the rest of Asia, we believe that the RBA will keep rates at or below the current level for an extended period. Moreover, the RBA has sounded further concern on the level of the currency, reintroducing the line that AUD remains “historically high” in its latest rate decision statement. As such, with policy normalising in many other parts of the developed world, both growth and rate differentials should weigh against AUD. The risk to our view would be a strong rebound in global economic growth.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.