I gave Charlie Aitken a ribbing last year when he picked Fortescue as a top stock for 2014 and it seems he’s now bearing me out (pun intended):

Not many people in Australia would have noticed but the former high-flying NASDAQ Internet Index lost another -4.2% on Friday night taking it back to its lowest close since November 2013. To me this simply confirms the momentum/growth at any price (GAAP) trade is dead and rotation to growth at a reasonable price (GARP) and value stocks is the new trend. Sell hares, buy tortoises remains the right strategy, or sell hares, park in cash for absolute return investors. The 5 year chart of the NASDAQ Internet Index is below, confirming a classic “head & shoulders” pattern.

You can see this rotation occurred over the last few weeks and it actually took broader global and local equity indices higher due to the index weightings of mega cap relative value stocks. In Australia, the ASX200 made a fresh six year high led by ASX20 leaders names, the big 4 banks, Telstra, Woolworths, Origin Energy and Woodside Petroleum.

The question then clearly becomes ‘what comes next’?..

Personally I think in an Australian context there is more rotation from high-flyers to laggards to come, but I suspect that process could be driven by a broader global trading correction starting. To me any rotation from the leaders of the rally to laggards is a short to medium term bearish event. It’s is more often than not the prelude to a broader corrective event in the asset class as it’s the first sign investors are struggling with valuations, or more correctly, struggling to find absolute value.

This is exactly where I sit right now writing Australian equity strategy. There are plenty of stocks I am prepared to “hold”, but I am finding it increasingly difficult to find stocks to recommend physically buying or adding to at current share prices. On the other side of that I am finding it increasingly easy to find stocks that appear overvalued and vulnerable to a valuation correction. As I have written previously, whenever I have found myself in this position before it has usually been the precursor to a pullback that produced a better broader buying opportunity.

This wouldn’t be an unusual position to find yourself in after 5 years of ZIRP and QE. Central banks have forced anyone who relies on investment income to take a risk and now we are even seeing corporate boards, who have previously been the biggest cash hoarders of all, deploy that cash via M&A. That M&A spree, which globally is already at $1trillion this year, is another contrarian signal to be tactically cautious in my view as it also coincides with the peak in near-term valuations.

Similarly, hedge funds have been forced to cover shorts and margin loan volumes are back at record highs on the NYSE. Yet, the leaders of the global rally of the last few years, high revenue growth stocks, have hit an air-pocket.

In Australia, some of the recent strength in banks has been global macro funds covering Australian bank short positions vs. Chinese mainland bank longs. Australian banks have performed extremely well into the interim reporting and dividend season, one which we believe will confirm record earnings and dividends, but even I as the longest term strategic Australian bank bull would have to say they are now pricing in the good news we think is coming.

It’s worth noting last week 3 of the 4 major Australian banks hit my long-held top down price targets that were inverse of 5.00%ff FY14 dividend yields. CBA even dropped to 4.98%ff on FY14, while NAB is still up at 5.63%. However, the point is when I set those inverse 5.00%ff yield based share price targets most people though they were ridiculous: today they are reality and that suggest the major banks are also now more “holds” than “buys”.

You can see this is all building up to a point and the seasonally weak period in equities from May through July is upon us.

I just think it’s a time to be sensible and disciplined. The Fed will further reduce support for markets this week with another $10b QE taper and it’s absolutely clear the next move in global and domestic interest rates is up. It’s just a matter of when. I think you can see the clear effect of QE tapering in the momentum/GAAP names on Wall St: that is where the big “free money” bets were deployed and are now being unwound.

At the same time the Ukrainian situation does have the potential to become uglier for markets, while in Australia we face the prospect of the toughest Federal Budget in a decade.

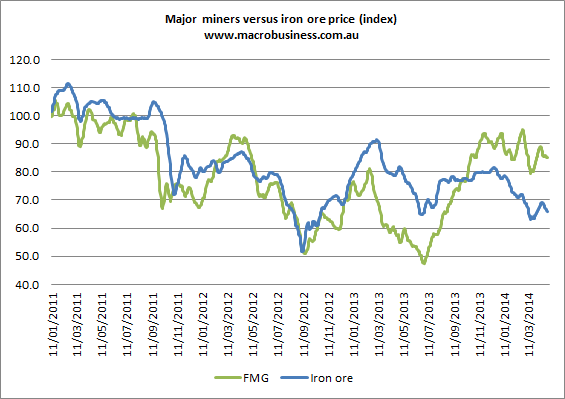

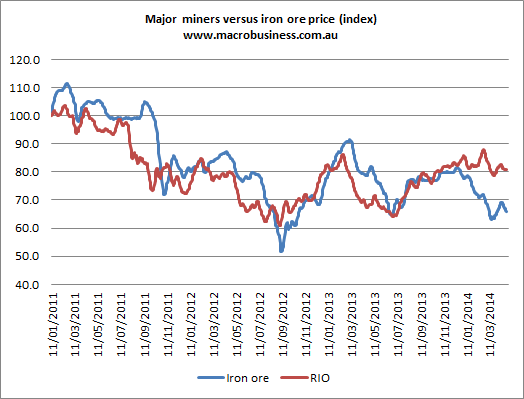

Similarly, key Australian bulk commodity prices (ex LNG) are falling, with both forms of coal looking horrible and iron ore looking like it wants to drop below $100t as India ends export bans. I realise the consensus view is that lower forward iron ore prices are “priced into” key Australian iron ore producers, but I also remember this was the consensus view on coal equities about 2 years ago and they went down 1:1 with the spot coal prices. I do worry that if we come in and turn our screens on in a few months and iron ore is $80 to $90t that the major producer share prices will be lower, again putting pressure on the broader Australian equity indices.

The other problem we have is these bulk commodity prices are falling yet the Australian Dollar is remaining remarkably resilient due to foreign carry trade demand. Commodity prices in AUD are weak and it seems the more the Treasury issues large amounts of bonds to finance our deficits the more demand there is for AUD from foreign carry traders. Don’t get me wrong, I still think AUD/USD @92.74usc is overvalued and think we will eventually see 75c to 80c, but it could take longer than I previously thought.

After 10 days of fresh country air I have to say my conservative tactical stance is even more confirmed. I reiterate my list of Australian stocks vulnerable to a valuation correction and suggest many Australian investors are a little too sanguine about what is happening globally in momentum/GAAP stocks; REA Group (REA), Seek ltd (SEK), Domino Pizza Enterprises (DMP), CarSales.Com (CRZ), Xero Ltd (XRO), Vocus Comms ltd (VOC), TPG Telecom Ltd (TPM), iiNet ltd (IIN), CSL ltd (CSL), ResMed Inc (RMD), Ramsay Healthcare (RHC), Sirtex Medical (SRX) ,21STCentury Fox (FOX),Navitas (NVT),G8 Education (GEM),OzFoxex (OFX),Vocation (VET),Donaco (DNA),James Hardie (JHX),Magellan Financial Group (MFG),BT Investment Management (BTT),Platinum Asset Management (PTM),Henderson Group (HGG),Credit Corp Group (CCP),Veda Group (VED),ASX Ltd (ASX),Macquarie Group (MQG),Brambles (BXB), Amcor (AMC), Fletcher Building (FBU), IOOF (IFL), Sydney Airport (SYD) and Transurban Group (TCL).

I suspect most people have tried to buy the dip in these names where the global experience is you should be selling any rallies. It’s blatantly clear momentum names will lead any broader trading correction, yet also underperform on simple rotation. To me they are a lose/lose situation, both absolutely and relatively until better value emerges.

I find myself in furious agreement with our Charlie today. High beta will remain under pressure either from tapering or geopolitical tensions and iron ore weakness is not priced into equities at all, not the kind that’s coming, anyway. Since Charlie’s late December pick, FMG is down 10% and there is more to come assuming the iron ore price falls:

Advertisement

I expect the current decoupling gap between the relative performance of the iron ore price and iron ore equities to close before this year is out and perhaps invert at some point as we overshoot!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.