The nutters at Zero Hedge said it best with their Friday headline:

Stocks Close At New Record High On Russian Invasion, GDP Decline And Pending Home Sales Miss

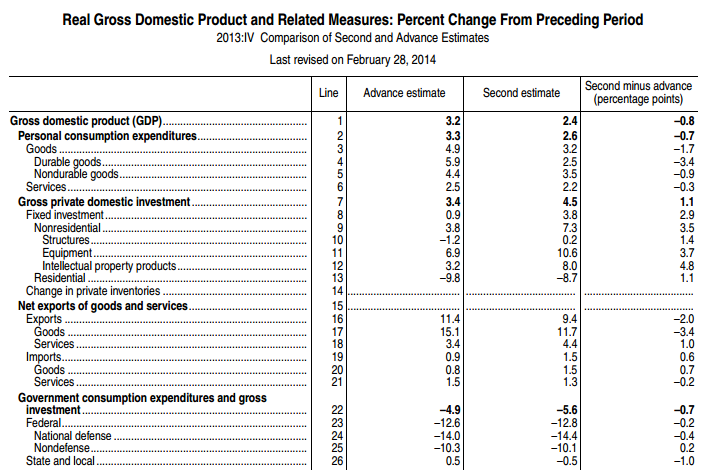

That about sums it up but let’s go through the data in detail and try to make some sense of a confusing evening! First up, the Q4 2014 GDP revisions were awful:

The GDP estimate released today is based on more complete source data than were available for the “advance” estimate issued last month. In the advance estimate, the increase in real GDP was 3.2 percent. …The second estimate of the fourth-quarter percent change in real GDP is 0.8 percentage point, or $32.7 billion, less than the advance estimate issued last month, primarily reflecting downward revisions to personal consumption expenditures (PCE), to private inventory investment, to exports, and to state and local government spending that were partly offset by an upward revision to nonresidential fixed investment.

Advertisement

So the two big drags were large falls in personal and government expenditures with decent upgrades (but not enough) to investment. That was enough to send stocks straight to record highs as taper faded to a distant nightmare.

Pending home sales were essentially unchanged in January, according to the National Association of Realtors®. Monthly gains in the South and Northeast were offset by declines in the West and Midwest.

The Pending Home Sales Index, a forward-looking indicator based on contract signings, edged up 0.1 percent to 95.0 in January from an upwardly revised 94.9 in December, but is 9.0 percent below January 2013 when it was 104.4.

Lawrence Yun, NAR chief economist, said that factors which dampened December activity also were at play in January. “Ongoing disruptive weather patterns in much of the U.S. inhibited home shopping,” he said. “Limited inventory also is playing a role, especially in the West, while credit remains tight and affordability isn’t as favorable as it was a year ago.”

The December index reading was the lowest since November 2011, when it stood at 94.6.

The PHSI in the Northeast rose 2.3 percent to 79.0 in January, but is 5.3 percent below a year ago. In the Midwest the index declined 2.5 percent to 92.9 in January, and is 9.3 percent lower than January 2013. Pending home sales in the South increased 3.5 percent to an index of 111.2 in January, and is 5.5 percent below a year ago. The index in the West fell 4.8 percent in January to 84.2, and is 17.5 percent below January 2013.

Existing-home sales are expected to be weak in the first quarter, while prices continue to rise from limited inventory. “Increasing new home construction can quickly solve two problems, producing more inventory and taming price growth,” Yun said.

The Chicago PMI threatened briefly to disrupt the party coming in at a very solid 59.8 points:

The Chicago Business Barometer remained broadly unchanged at 59.8 in February compared with 59.6 in January, as a double-digit gain in Employment offset declines in New Orders, Production and Order Backlogs.

The Chicago Report points to firm growth and a continued recovery in the US economy, with the Barometer standing at its highest level since December and remaining around 60 for the fifth consecutive month.

Some panellists cited the negative effect of the poor weather on their business, although overall this appeared to have a minor impact that was only visible in longer supplier lead times.

Stocks fell into the close but were rescued by the final shocker of the day, the headline that Russia was invading Ukraine. From Zero Hedge:

The upshot for markets was taper confusion. Stocks closed at record highs, the 30 year bond was bid marginally but the 10 year fell, the US dollar was hammered half a cent but gold fell as well one percent, the Australian dollar fell to but not very far.

It’s hard to go past Zero Hedge’s summation of the day’s trade:

All one can do at this point is sit back and laugh at the complete abortion that Ben Bernanke’s, and now Janet Yellen’s centrally-planned “market” has become.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.