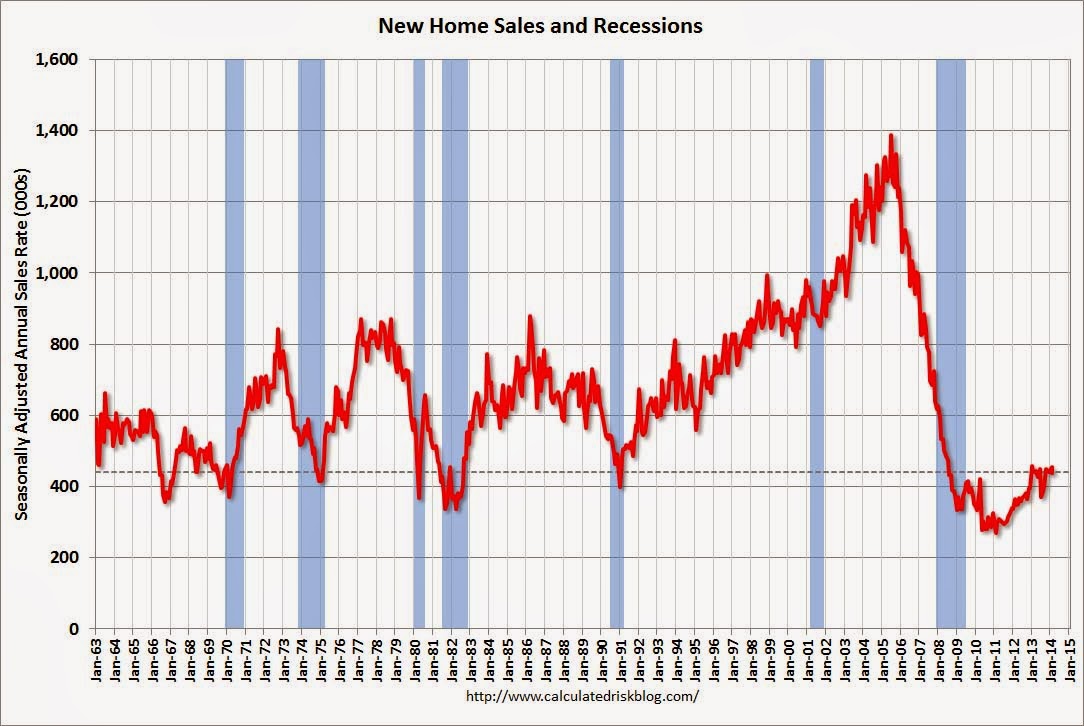

The last two days have seen a string of mediocre US housing reports, which may have helped along the bid at the long end of the bond curve. Yesterday we had new home sales which met lowered expectations (all charts from Calculated Risk):

Sales of new single-family houses in February 2014 were at a seasonally adjusted annual rate of 440,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 3.3 percent below the revised January rate of 455,000 and is 1.1 percent below the February 2013 estimate of 445,000.

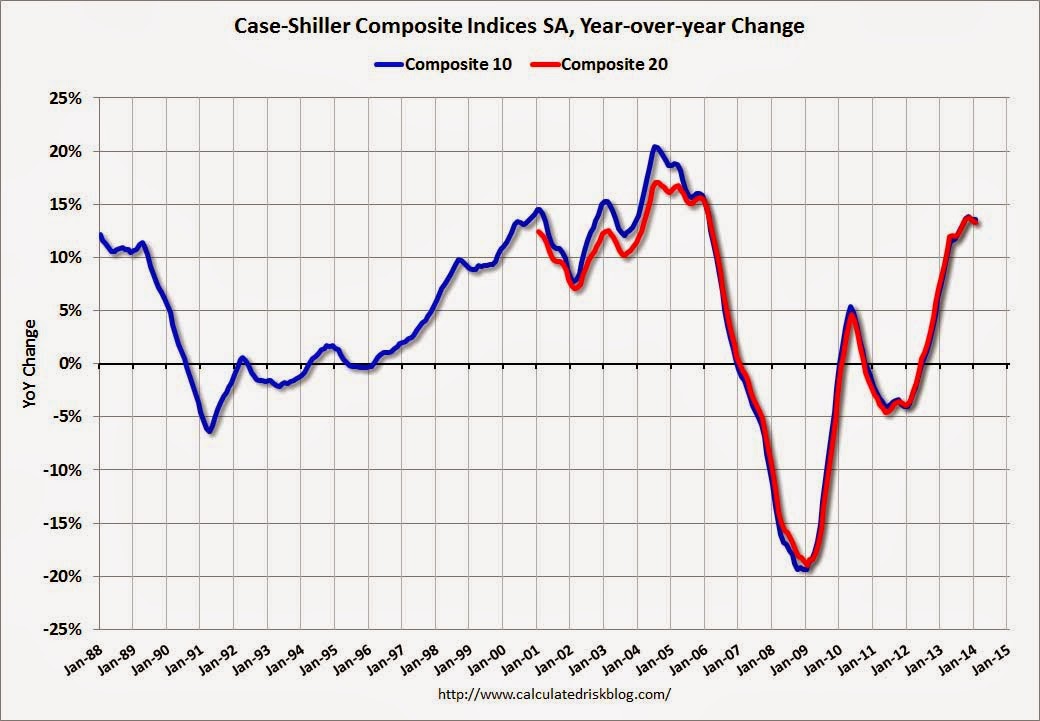

Case-Shiller was out for January and shows prices are slowing, o.8 for the month and 13.5% for the year:

Advertisement

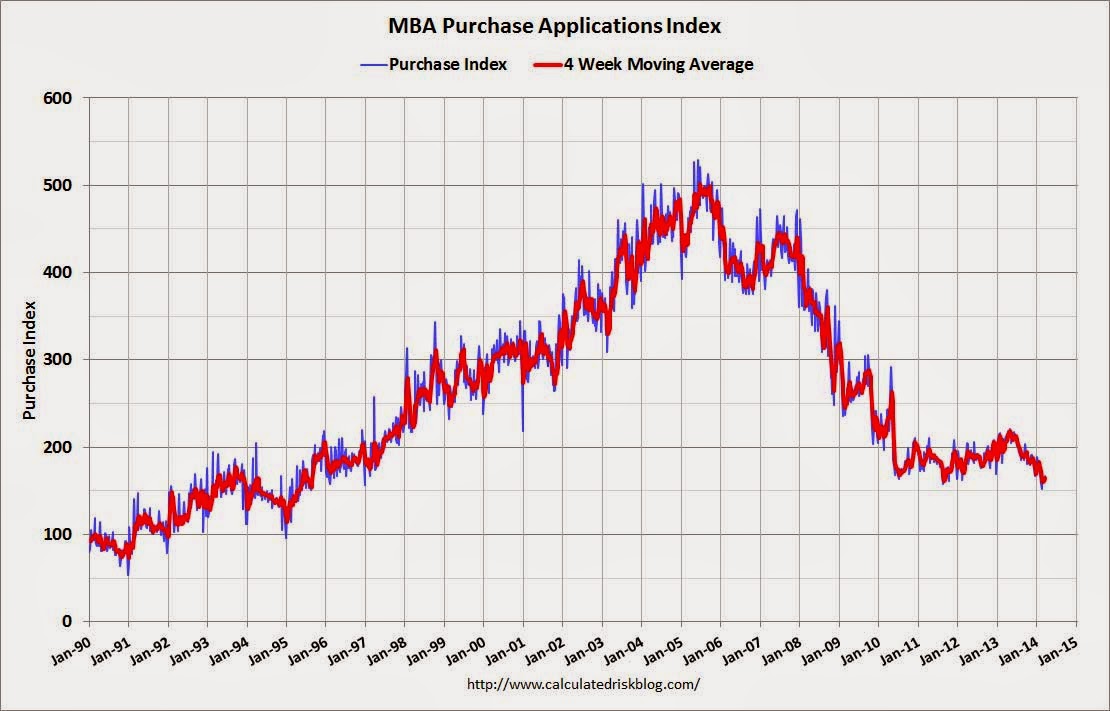

And today, MBA mortgage data shows ongoing weakness in originations:

The Refinance Index decreased 8 percent from the previous week, including an 8.1 percent decline in conventional refinance applications and a 5.8 percent decline in government refinance applications; the government refinance index dropped to the lowest level since July 2011. In contrast, the seasonally adjusted Purchase Index increased 3 percent from one week earlier, driven mainly by a 4.0 percent increase in conventional purchase applications….

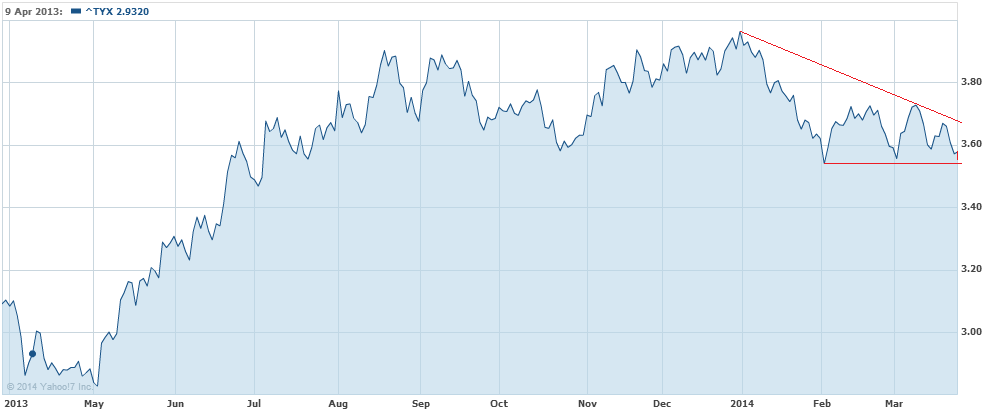

Perhaps there’s a little safe haven bid coming into bonds as well on Crimean tensions but that’s not helping gold or hitting the Aussie. Anyway, the 30 year yield is now right on crucial support 3.55%:

Advertisement

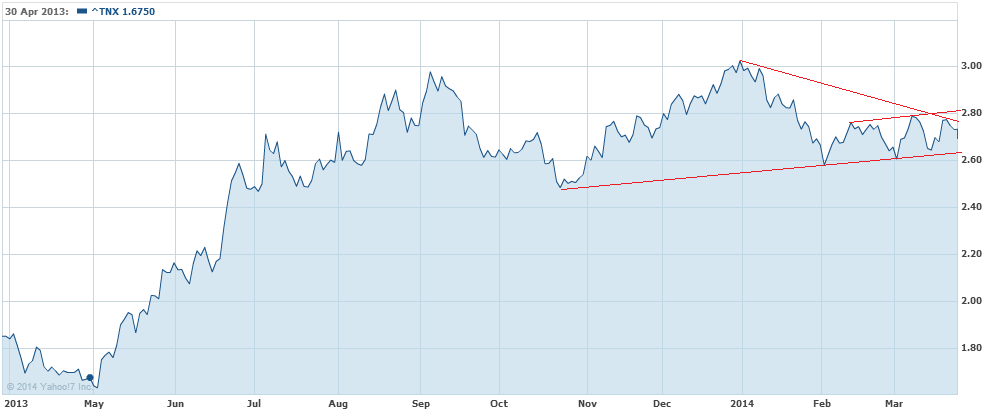

The 10 year is marginally less bearish, with some breathing room still:

Advertisement

If these supports break then the pressure on the Australian dollar will mount.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.