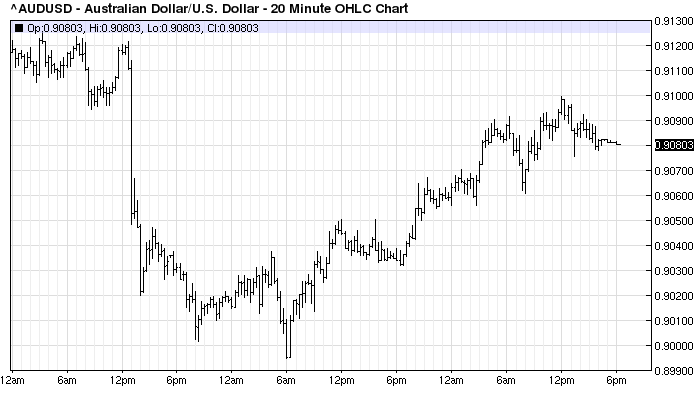

Friday evening saw more bullish Australian dollar action. It was a night of subtle ‘risk off’ but not for the Aussie, piling on 0.5% and threatening 91 cents again:

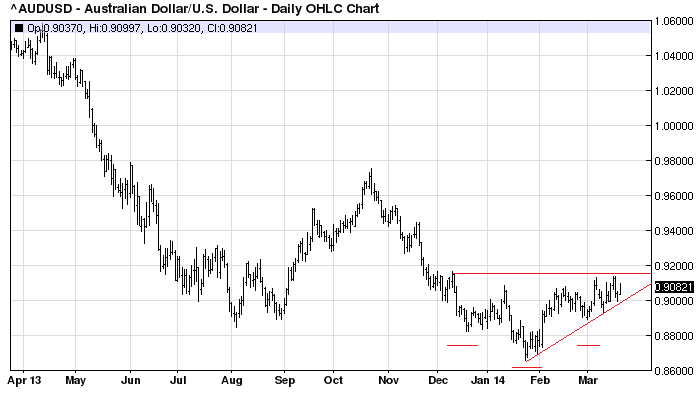

The long term chart is now unmistakably bullish with an inverted head and shoulders bottom and ascending triangle forming:

Advertisement

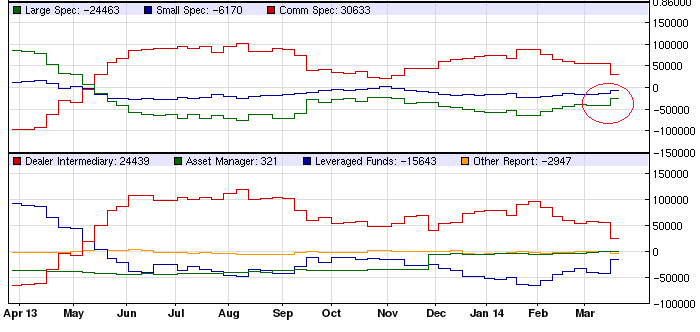

The recent commitment of traders report is also showing large and small speculators covering their shorts:

Not yet net long but trending that way. So, what’s going on? Unusual moves in US bond markets is what.

Advertisement

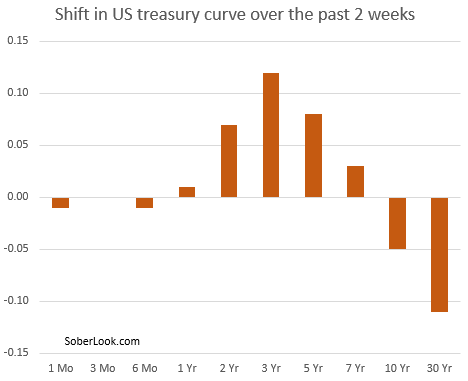

Last week saw lots of comment about the Fed’s hawkish shift and its effects on the US yield curve. Sober Look has a nice summary:

Treasuries once again experienced what amounts to a sharp curve flattening in recent days. The market action resembled what took place after the initial announcement of taper back in December (see post). The yields in the “belly” of the curve have risen sharply as the market prepares for rate “normalization”.

MarketWatch: – The yield curve’s violent reaction to the Federal Reserve on Wednesday shouldn’t be thought of as a first-day fluke by Chairwoman Janet Yellen. Rather, the rise of intermediate-term Treasury yields is one step in a monetary policy normalization process that will characterize the rest of the year, according to mammoth investment management firm BlackRock.

If last year was all about longer-duration Treasury yields moving higher — the 10-year Treasury yield rose more than a full percentage point and now trades at 2.78% – this year is all about the rise at the front end of the curve, according to Rick Rieder, chief investment officer of Fundamental Fixed Income for BlackRock.

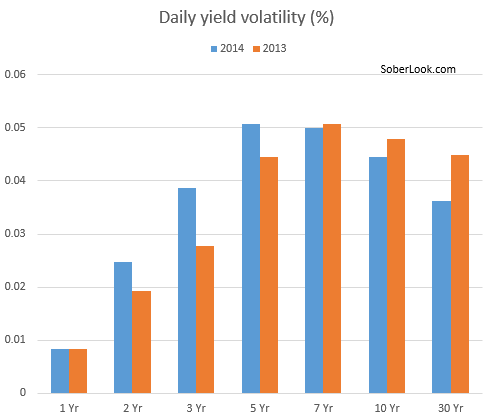

“I think this is a very different year for managing fixed income,” he said in a press briefing Thursday.The MarketWatch article proceeds to describe in detail how rates had moved this year vs. last year. It all however comes down to a single chart which shows daily treasury yield volatility across the curve this vs. last year. A picture is worth, well you know…

Market focus is shifting from taper to the near-term trajectory of the overnight rates, which is impacting the intermediate and shorter maturities. The first rate hike, while still some time away, is becoming a reality.

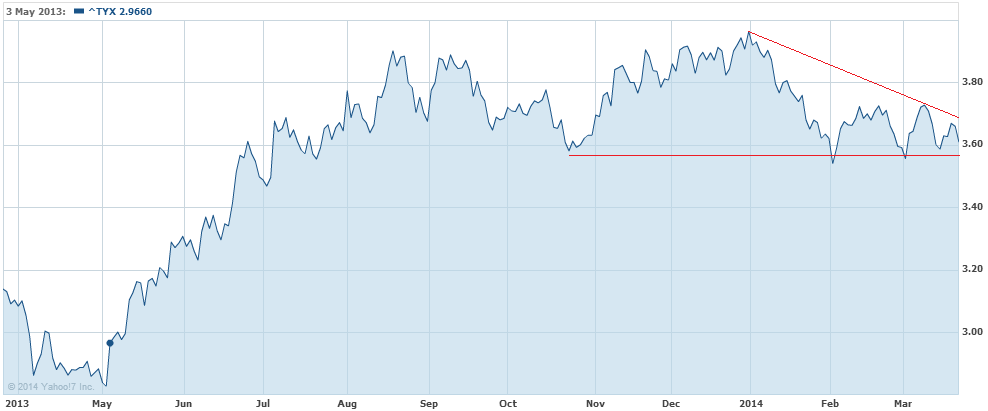

Yes, it is but only at the short end. Long bond yields still look more likely to fall than rise, indeed the 10 and 30 year yields both fell 1% and more Friday. The 30 year especially has a bearish chart:

Advertisement

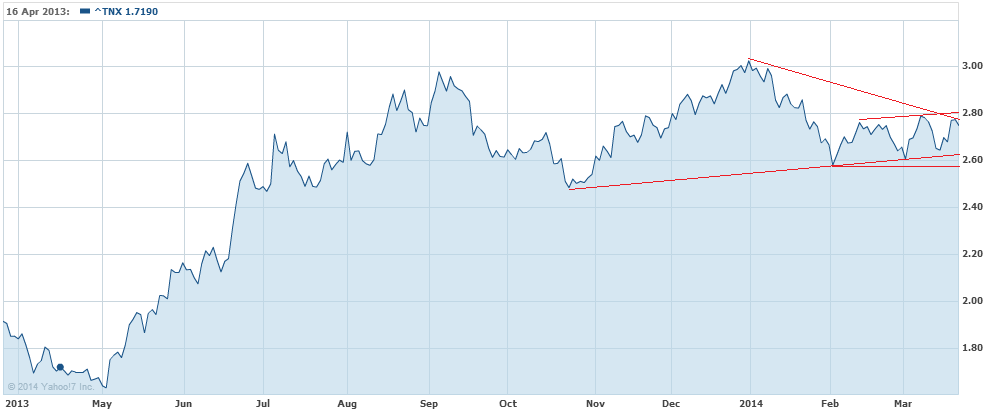

The 10 year not quite so much:

I would interpret this as the US bond market paying attention to a hawkish Fed but dismissing its long term forecasts. The Fed raised its 2016 year end forecast for the cash rate to 2.25%. The last time the US cash rate was at that level was in March 2008 and the 10 and 30 year yield were at 4%. The time before that, in 2005, both were at 4.5%. In short, if the Fed is going to get to 2.25% on time, the long bond needs to be higher.

Advertisement

US bond markets are pricing the Fed’s attempt to reach its tightening targets but they’re also pricing the failure to get there.

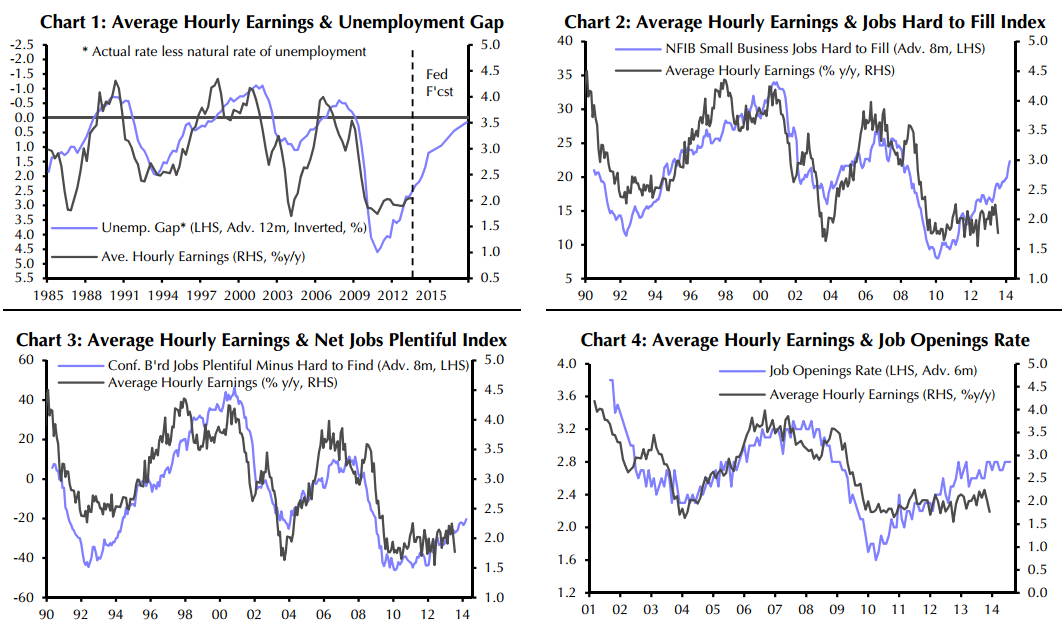

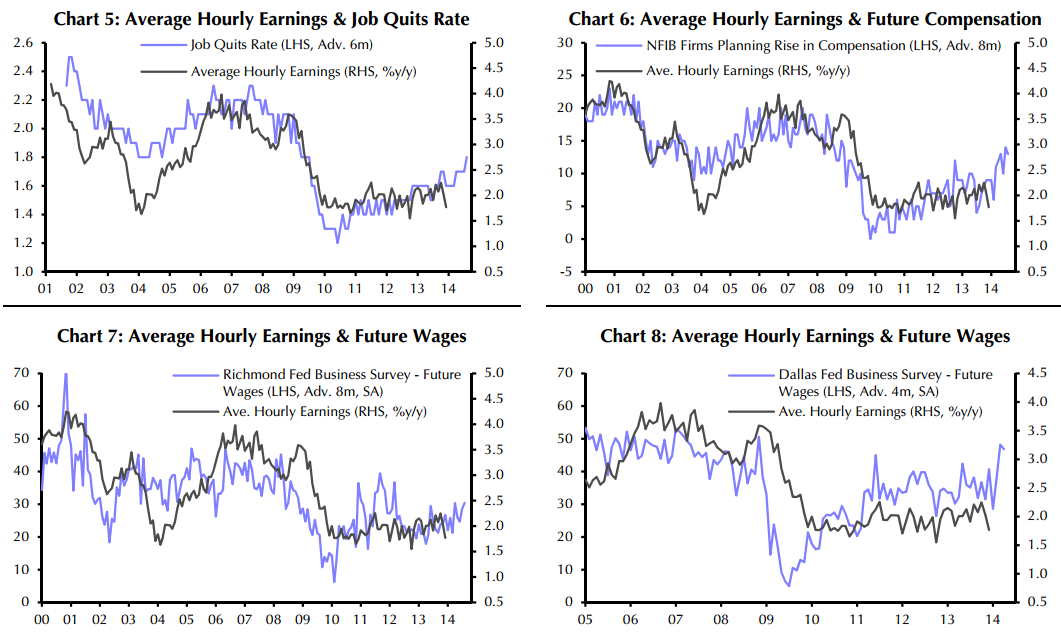

There are reasons to think that the Fed is right and that the bond market will follow. The following charts from Capital Economics show the incipient tightening in the US labour market that may precipitate higher interest rates:

Advertisement

But there is still considerable slack in the US economy to contain inflation and likely to be more dis-inflationary pressure from Chinese tightening and the steady deflation of the commodities complex.

Even if the recovery has enough momentum to reach the Fed’s growth targets there is unlikely to be much inflation. Hence the the yield curve may remain flat.

Advertisement

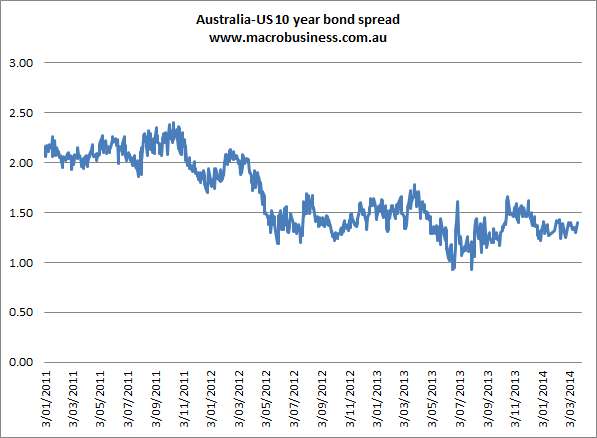

Given the yield spread on the 10 year bond is the dominant benchmark for carry trades, that is the worst of both world’s for Australia because, even though the US tightens, it’s recalcitrant bond market won’t allow any compression in the yield spread with Australia:

Meanwhile, in Australia, the RBA’s revitalised housing bubble has lots of folks looking “across the valley” of the capex cliff to rate hikes. They’re probably wrong, not least because the expectation is self-defeating in that without a lower dollar there’ll be no sustained recovery, but that’s not the point right now.

Advertisement

So long as the US long bond market flips the bird at the Fed then the Australian dollar is going to be under upwards pressure.

If ever a country needed macroprudential tools to defend itself from speculators within and without it is Australia right now.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.