In political economist Mancur Olson’s pathbreaking book, The Rise and Decline of Nations, published in 1982, he argued that a country’s economic stability ultimately leads to decline as it becomes increasingly dominated by organised interest groups, each seeking to advance their interests at the expense of others.

By contrast, countries that have a collapse of the political regime, and the interest groups that have coalesced around it, can radically improve productivity and increase national income because they start with a clean slate in the aftermath of the collapse. Examples are the rapid growth of postwar Germany and Japan, as Wikipedia reminds us.

…What these days passes for the political debate seems to be dominated by ”distributional coalitions”, in Olson’s phrase, arguing for ”reforms” from which the chief beneficiaries would be their good selves, or desperately opposing government reforms that would impose even the most modest sacrifice on their members.

What gets me is how blatantly self-seeking our lobby groups have become. It is as if the era of economic rationalism – with its belief that the economy is driven by self-interest – has sanctified selfishness and refusal to co-operate for the common good.

This is one of those occasional pieces by Ross Gittins that rescues him from regular light-weight ruminations about confidence and the triumph of the services economy. I very much agree with Mr Gittins about the problem he describes. Trouble is, I see him as one of the worst rent-seekers of all.

Advertisement

How so, you cry?!

Fundamentally it is this: if rent-seeking prevents the most efficient flow of capital for productive purposes, and thus the rise of national wealth and with it the common good, then why does Mr Gittins spend so much of his time defending an economic model in which services and mining are seen as the natural evolution of the economy? Above all else, it is the embrace of this model of growth that is killing the productivity that Mr Gittins’ purports to champion.

There are three legs to the argument that Mr Gittins is as bad a rent-seeker (perhaps worse) than those he criticises. The first leg is that the services economy is largely non-tradable. As such, it doesn’t tend to generate capital in and of itself. It relies instead upon debt to grow. In Australia that debt is largely expressed through mortgages. Such a system can run successfully for a long time, especially if it is underpinned by another export sector that is producing traded capital – like mining.

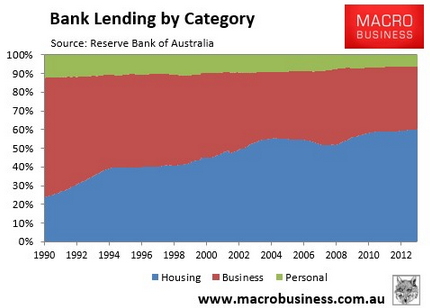

But at a certain point, Minskian dynamics start of overwhelm the system as more and more capital is sucked into the unproductive venture of mortgages and productivity starts to fall. That, I submit to you, is where the Australian economy is today, with our banks pouring far larger proportions of the nation’s capital into mortgages than at time since records were kept:

Advertisement

Indeed, my fellow blogger, Cameron Murray, has estimated that a considerable slice of Australia’s declining multi-factor productivity has resulted directly from escalating land prices:

The ABS explains that they take the balance sheet value of land from the national accounts to include as the land component of capital stock. We can observe in the chart below the rise in the value of the land balance sheet value against the estimate of MFP, and indeed against an estimate of the land balance if land values simply tracked inflation. Quite clearly, from about 2002 onwards the abnormal increase in the value of land lead to a flattening and falling estimate of MFP. More telling is that fall in all land asset values in 2009 lead immediately to an increase in the MFP measure, only for the next wave of land price escalation, especially FHOB stimulated residential land, to cause a deterioration in MFP during 2011.

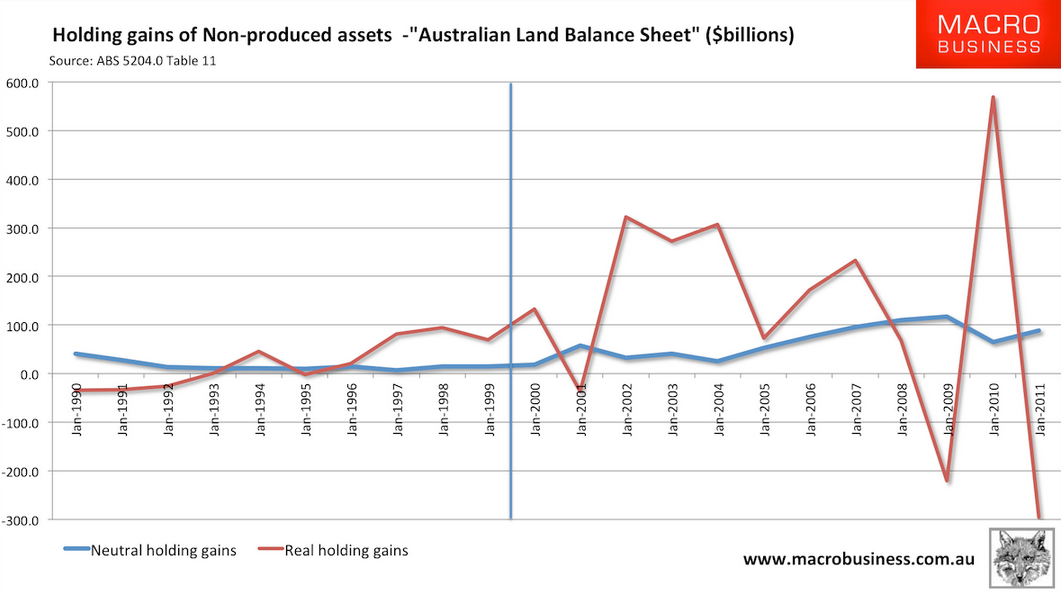

We can dig a little deeper into the ‘land balance sheet’ in the system of national accounts, and look closely at the type of increases in land value estimated. The chart below shows in blue the neutral holding gains – that is, the change in the value of land expected if prices tracked inflation. This measure is the result of In red we see the real holding gains, which are market-based increases in land values. As the ABS notes“Holding gains and losses accrue to the owners of assets and liabilities purely as a result of holding the assets or liabilities over time, without transforming them in any way”. In economic terms, they are pure rents.

When red is greater than blue, we find a significant downward bias in the MFP estimate. It is really that simple. And we are not alone in this either. Spain’s land price boom resulted similar pattern of declining MFP during their land price boom in the early 2000s.

Advertisement

Notice the terminology: untransformed gains from holding assets and liabilities are pure rents.

The second leg of the argument is that Gittins is a key defender of both sides of politics and the policy executive in the shedding of the manufacturing sector of the economy. Again, if you believe productivity is the best and brightest path to greater prosperity (which is what Gittins’ argument is all about) then you cannot ignore the fact that manufacturing is the single greatest contributing sector to productivity gains in any economy. As I’ve pointed out before:

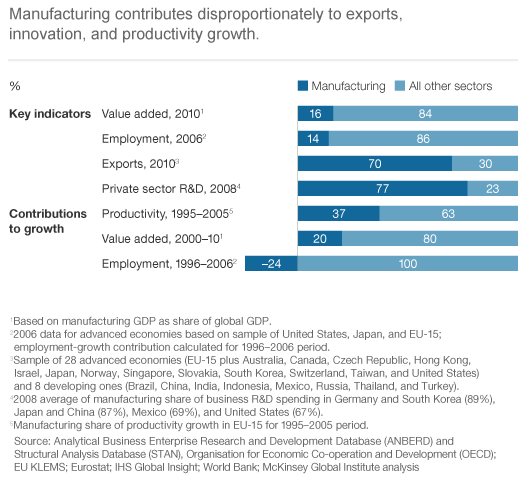

The following chart from McKinsey makes the point. Manufacturing contributes disproportionately to productivity, innovation and exports:

These out-sized gains make a country richer more quickly which is why every example of successful catch-up development – North Asia in this century or the US in the last – has focused very heavily on growing a dynamic manufacturing sector. Of course the manufacturing changes as an economy gets more expensive but the economic rationale doesn’t change.

Advertisement

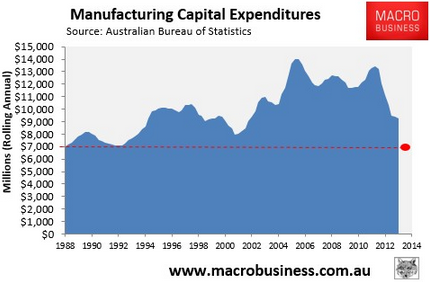

Quite! So as Australian manufacturing investment plunges toward extinction in the recent capex report, why is Mr Gittins cheering it along:

Now, don’t get me wrong. Defending rent-seekers within manufacturing isn’t going to help. Manufacturing needs competitive pressures as much as any other sector to remain innovative and lean. But completely shedding your manufacturing sector in pursuit of productivity that has been destroyed by the debt-driven cost-input inflation of the services sector doesn’t make much sense either!

Advertisement

The final leg of this argument is that although Mr Gittins is absolutely right about the proliferation of professional lobbyists, they are at least visible if one looks closely. On the other hand, Mr Gittins occupies a reified communal space defined intrinsically as objective. He is the clear-thinker atop a soap box in the town square delivering truth to compromised power, captured most eloquently in his masthead’s sub-title “Independent. Always”.

But as Fairfax Media dies its slow death, it is being eaten by its own real estate businesses, which now constitute almost half the firm’s value. In short, the box that Mr Gittins is standing upon is stamped all over with “bought to you by the Australian real estate sector”; the same sector that is at the centre of the services economy and productivity bog into which the Australian economy is sinking.

That is not to say that Mr Gittins is deliberately misleading anyone. But such systems tend to self-perpetuate, more by inertia than design.

Advertisement

So! When I read Mr Gittins opine about the rise of the rent-seekers, my own analytical framework – which is part Minsky, part Keynes, part Schumpeter and part Hamilton (Alexander that is) – sees a jewel-encrusted and supine emperor gesturing lazily at baby elephants from atop a giant mammoth crushing all else in the room.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.