Well…I am sorry to be the bearer of bad new on Ukraine but it appears, well and truly, that markets have cast it aside like chaff blown across the steppe. In the world of money all that matters is real politik and Vladimir Putin has it in spades (with the usual caveat that the human being can always be a free radical).

Vladimir Putin on Tuesday appeared to step back from the brink of confrontation with the west when he told a televised news conference that tensions that could have led to military intervention in Ukraine had “dissipated”.

Speaking about the possible use of Russia’s armed forces, Mr Putin said: “The tense situation in the Crimea, associated with the possible use of the armed forces, just dissipated, the need for that did not arise. The only thing which was necessary, and which we did, was to strengthen the protection of our military installations . . .

“Therefore I believe that it will not be necessary for us to do anything like that in eastern Ukraine.”

Advertisement

Indeed, why bother. Putin now has Europe where he wants it, Ukraine where he wants it, the US where he wants it, and to underline the fact a few little gas price rises appeared:

Gazprom will raise gas prices for Ukraine from the start of next month because the country has failed to pay its debts, said Alexei Miller, the Russian gas company chief executive, on Tuesday.

A rise in prices has been widely expected since the fall of the Yanukovich government and Russia’s military escalation in Ukraine.

As part of a bailout deal in December, Vladimir Putin, Russian president, gave Ukraine a hefty discount on Russian gas supplies. However, the deal stipulated that the price must be renegotiated every three months.

In his televised news conference on Tuesday Mr Putin said Ukraine had not paid its Gazprom debt: “They failed to pay off the debt, I think it’s $1.5bn as of today, and if they don’t pay for February it’s going to be $2bn. So if you don’t pay, then let’s go back to regular prices. This makes perfect commercial sense. This has nothing to do with [the] situation in Ukraine. We gave them money, they failed to deliver. So it’s only natural . . .

Just sign here and all your troubles will be behind you! Putin really seemed to be enjoying himself when he briefly interrupted the party by test firing one of these:

Advertisement

Only Ukraine itself can now upset the new order, if it decides to fight, but it will be doing so alone.

And so, our amoral money machine accepted reality far quicker than our political leaders or polity (though maybe not the latter, or former!). Gold plunged 1%. Stocks strapped themselves to Putin’s intercontinental missile with a 1.3% rise into a new record close. Long bonds plunged further than they rallied yesterday with the 30 and 10 year yields up 1.5% and 2.5% respectively. Forex markets saw the unwind of the yen flight to safety, the US dollar strengthened marginally in ironic salute to the fading empire, and the Australian dollar was flat. The Russian sell-off reversed spectacularly with stocks up 5% and the rouble jumping 1.3%.

Advertisement

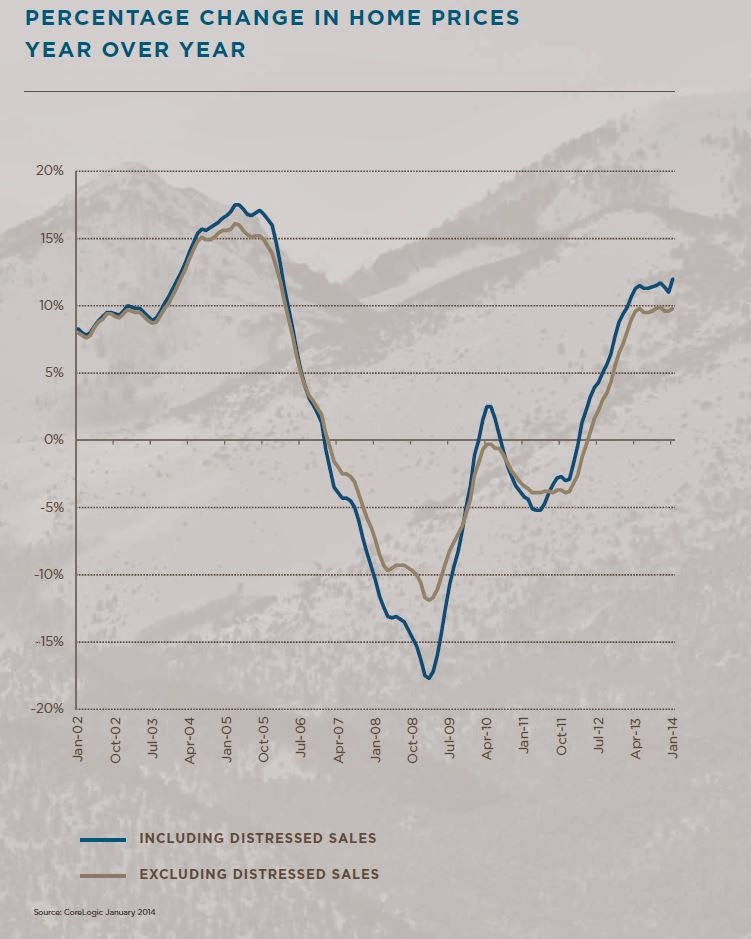

In the US, where all that matters these days is the Fed, the data flow was decent as well with Core Logic house prices still rising strongly despite the slowing in mortgages. From Calculated Risk:

Home prices, including distressed sales, increased by 12.0 percent in January 2014 compared to December 2013. January marks the 23nd consecutive month of year-over-year home price gains.Excluding distressed sales, home prices increased by 9.8 percent year over year. … Despite gains in December, home prices nationwide remain 17.3 percent below their peak, which was set in April 2006.“Polar vortices and a string of snow storms did not manage to weaken house price appreciation in January. The last time January month-over-month and year-over-year price appreciation was this strong was at the height of the housing bubble in 2006.” [said Dr. Mark Fleming, chief economist for CoreLogic].

Goldman pointed out that it’s been a hideous start to the year for the world:

Advertisement

Only two of the ten underlying components improved in February. On the positive side, the Global PMI aggregate increased after last month’s drop, and the Japan Inventory/Sales ratio also showed significant improvement.

On the negative side, the S&P GSCI Industrial Metals Index® fell marginally and US Initial Jobless claims ticked up slightly. The Belgian and Netherlands Manufacturing Survey and the Baltic Dry Index were also softer. The Consumer Confidence aggregate, which climbed back to its highest level in six years last month, retreated marginally, while the Global New Orders less Inventories (NOIN) aggregate continued to decline, driven in part by strong inventory accumulation in the US. Finally, Korean exports were again a bit weaker but at decent levels, and the AUD & CAD TWI aggregate was only slightly lower after a sharp fall over the previous three months.

But that, as we know, is all to the good for the Yellen put! All aboard the good missile S&P500!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.