The AFR’s David Bassanese has written an interesting article today arguing that Australian housing valuations are not too stretched and should not illicit too much concern:

While there are a few red flags emerging, the good news is that compared to late 2003, housing market valuations and the supply-demand balance are still less stretched.

…affordability measures and rental market indicators are not yet flashing red…

The current house price to income ratio is already somewhat above average, but not yet at recent cyclical peaks. Mortgage interest rates, meanwhile, are still well below the average for this period… So in terms of mortgage affordability, house prices are even further from red flag territory…

The rental market also provides some comfort that housing conditions have not yet become too frothy…

All up, market conditions seem to favour further house prices gains, at least over the next year, while interest rates stay low without necessarily fearing a return to bubble conditions.

I agree with Bassanese on some aspects, but disagree on others.

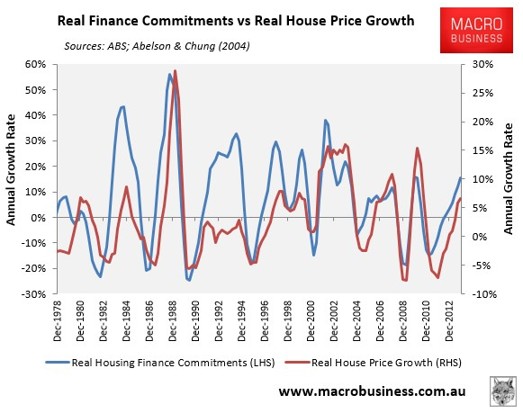

As argued in my latest MB Member’s report, the single best short-term indicator for house price growth – housing finance commitments (excluding refinancings) – continues to grow strongly which, given past strong correlations, suggests that prices nationally will increase throughout the year (see next chart).

It is also true that relative to incomes, inflation, and GDP, Australian housing valuations are just below their peak; although at the current pace of growth they are likely to hit an all-time high later this year.

That said, comparisons with a decade ago aren’t necessarily valid in my opinion, and I am far more concerned about the risks of a future correction.

A decade ago, Australia’s economy was about to embark on the biggest commodity price and mining investment boom in the nation’s history – a boom that would significantly boost Australian incomes and employment. So, while the housing market was just as inflated a decade ago, values were at least supported by strong employment growth and falling unemployment, followed by strongly rising incomes.

However, the situation today is the polar opposite, with the labour market weakening and income growth anaemic as the terms-of-trade declines. These headwinds will obviously make it increasingly difficult for house price growth to be maintained, while at the same time raising the real prospect that prices could correct in the event that unemployment rises significantly from current levels.

The medium-term outlook for the economy is also worrying. The once-in-a-century mining investment boom is set to decline sharply over the next few years as large mining projects finish, leading to the loss of a large number of jobs. To add insult to injury, the unwinding of the mining investment boom is likely to coincide with the closure of the Australian automotive assembly industry by 2017, which is expected to lead to the loss of up to 50,000 manufacturing jobs.

Finally, population ageing will see a continued contraction in the share of workers in the economy, creating headwinds for the economy and asset valuations into the future.

Given Australian housing valuations are likely to hit their highest level on record later this year just as the economy embarks on its biggest structural adjustment since the early-1990s recession, the risk of a correction sometime in the near future is arguably greater now than at any other time in living memory.