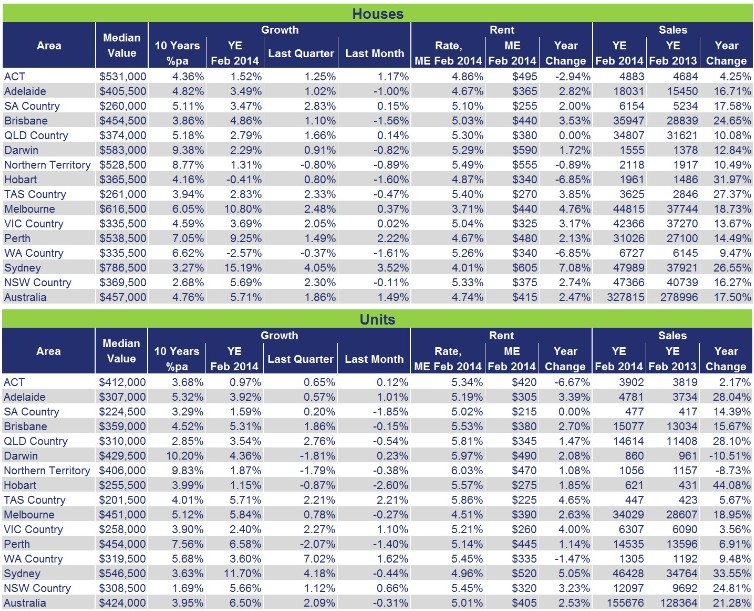

Residex has released its dwelling price results for February, which revealed a 1.49% national increase in house values over the month, but a 0.31% decline in unit values. In the year to February 2014, houses jumped in value by 5.71%, whereas units rose by 6.50%. A breakdown of the various markets is provided in the below tables, with Sydney leading the way:

In this month’s commentary, Residex founder, John Edwards, explains why he believes that Sydney house price growth has peaked, with the other capitals likely to follow suit later on:

Advertisement

So, what does 2014 have install for our property markets?

Without strong consumer sentiment, the property market is unlikely to stretch much beyond its current level as it will be getting far too unaffordable for the masses.

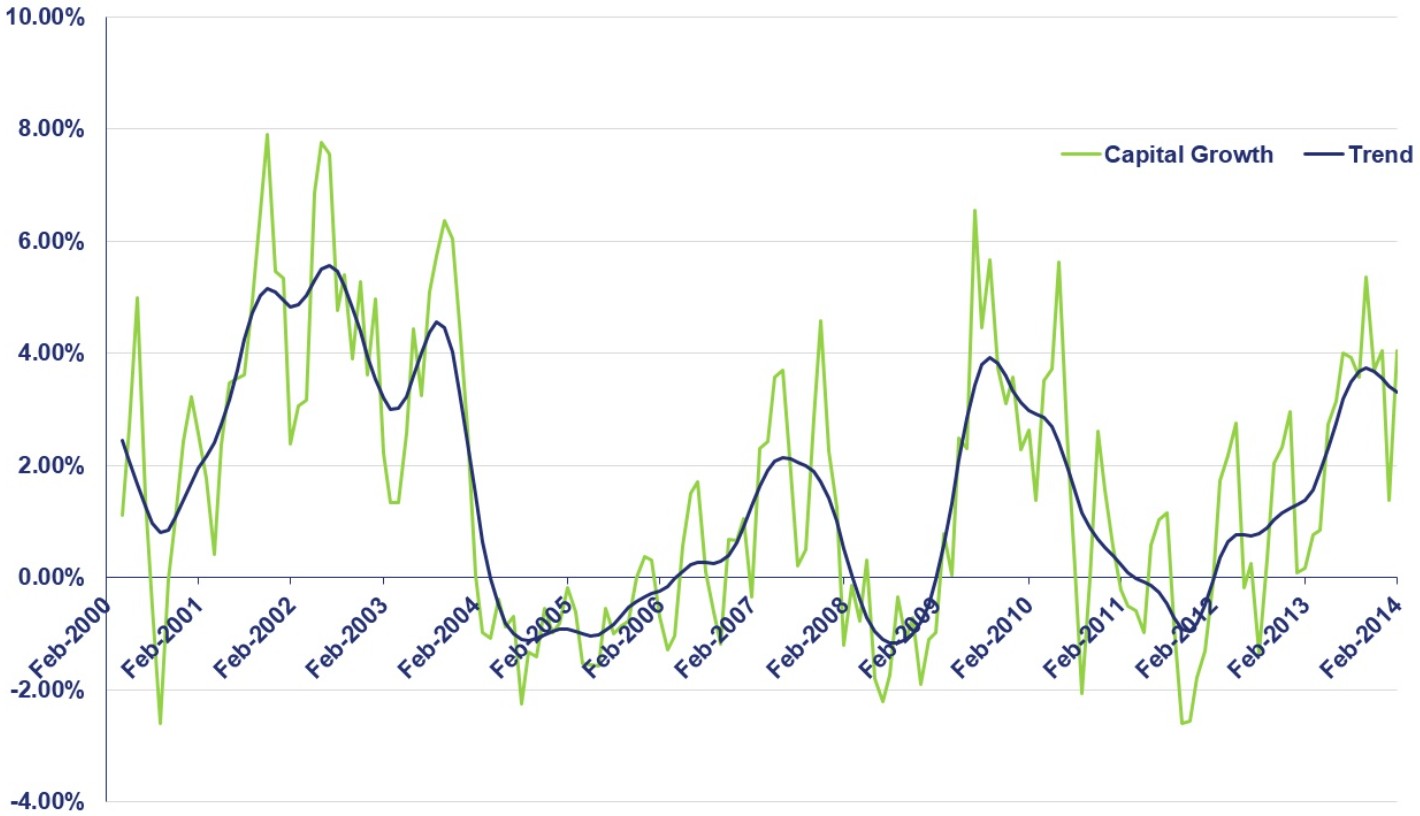

Historically, Sydney has been the lead indicator for other markets around Australia. Graph 1 presents Sydney’s growth pattern over the short term.

Graph 1

There are a number of interesting points evident in the graph:

The market seems to have peaked and is now presenting as if it is going to revert to a period of much lower growth.

The data indicates that the high points in growth are reducing with each growth period.

I believe both points correct.

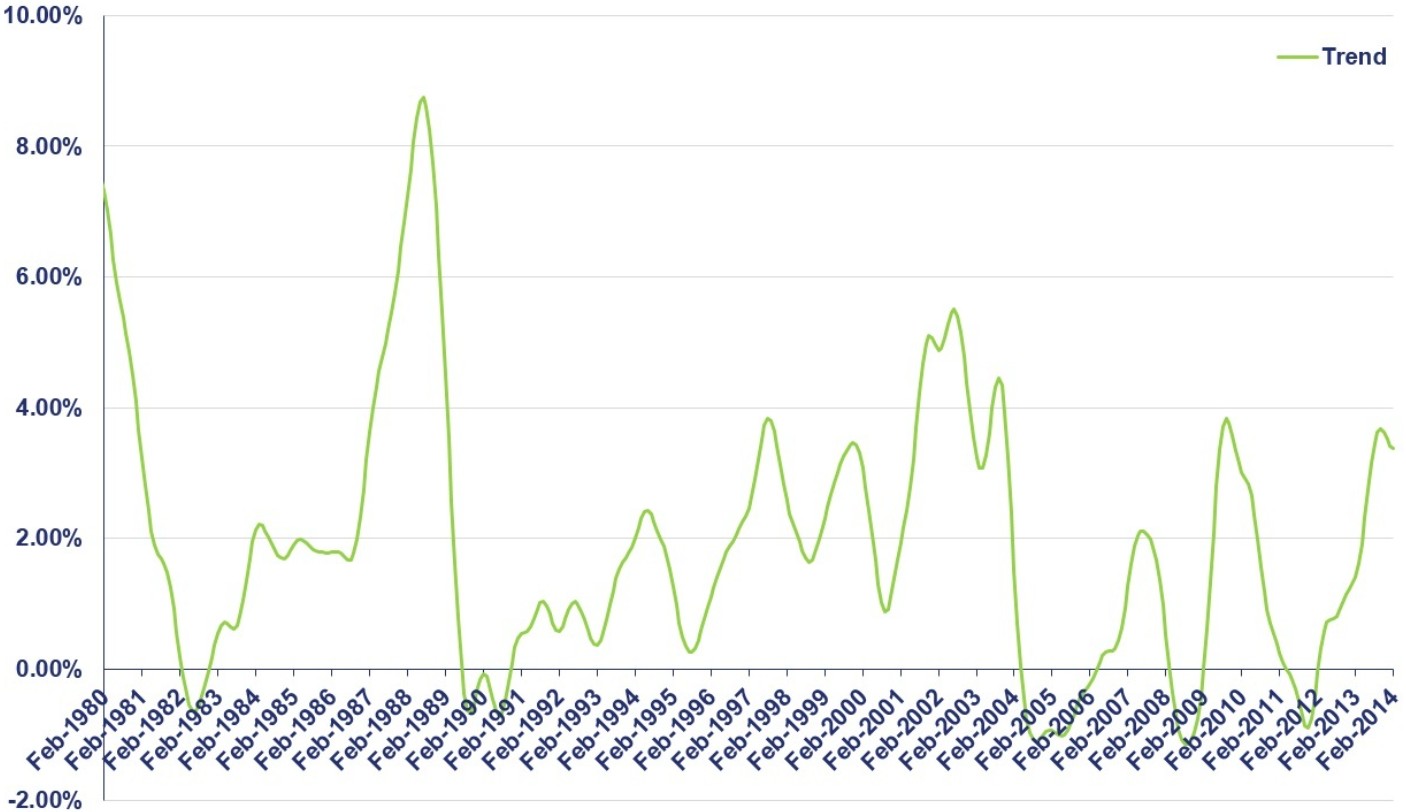

Graph 2 presents Sydney’s growth pattern since 1980. The downward growth trend over the longer term is clearly evident.

In fact, going back to the 1950′s when the highest period of growth in Australia’s history was recorded, the downward growth pattern is even more evident.

The logical reason for this pattern is, growth in any asset value will at some point reach a level that is unaffordable for the masses, particularly where there is some type of limit on supply. When this happens competition for the asset diminishes, as does the bidding war, and hence the extra amount that one party is prepared to pay to secure the asset above another also decreases.

While most people have a tendency to measure a market’s performance in capital growth percentages, this does not provide the necessary understanding on cost limitations. It simply encourages the market to believe that, as a market historically grew at a particular rate, it will do it again. However, this is an incorrect assumption as the dollar cost is always the limitation. Yes, the assumption would have a chance of being right if house price growth and household income grew at similar rates, but historically this has not been the case.

If you don’t accept that the limitation is cost and growth rates can just keep repeating themselves, consider a situation where wages are not increasing but houses are growing by 5% per annum. Assume a house a few years ago was worth $300,000 and grows by our 5%. The house increases in value by $15,000. As time passes, the house grows to be worth $700,000 and again grows 5%. Its value now increases by $35,000. Clearly, as wages have not grown, the house is going to be far more difficult to purchase and the annual uplift as it grows makes the problem larger each year. The market cannot keep increasing at the historical growth rate unless wages growth is equal to or better than house price growth, which has not been the case.

Given the above, the trend in Sydney’s growth pattern is not abnormal. It is simply a function of an asset that is increasing in value and constantly outperforming wage growth. This coupled with current levels of low affordability leads me to believe that Sydney house prices, in dollar terms, are reaching their peak value in this growth cycle.

The silver lining in this situation is that while house price growth in Sydney will probably slow for the remainder of the year, other states and capital cities still have some growth to achieve before reaching their peak value for this growth cycle.

I guess what Edwards is effectively saying is that house price growth cannot outpace incomes indefinitely, and eventually an affordability ceiling has to be reached. And with values approaching their all-time highs in relation to incomes, inflation, and GDP, this ceiling will be hit soon.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.