The Adelaide Bank/Real Estate Institute of Australia (REIA) has today released its quarterly mortgage affordability report, which conveyed the simple message: “Housing is not affordable for first home buyers”:

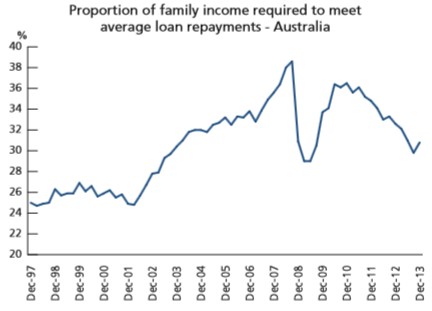

The December quarter of 2013 recorded a fall in housing affordability with the proportion of income required to meet loan repayments increasing 1.0 percentage point to 30.8%…

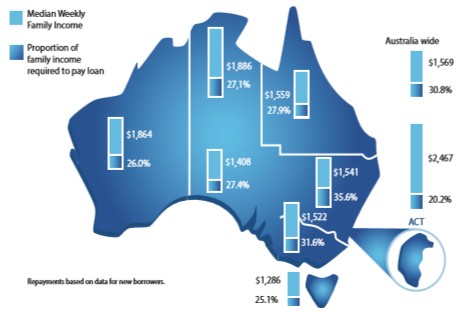

With the exception of the Northern Territory, all states and territories recorded a downturn in affordability over the quarter with the largest in New South Wales, where the proportion of income required to meet loan repayments rose by 1.8 percentage points to 35.6%…

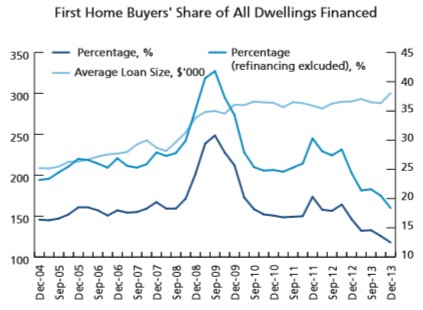

First home buyers made up 12.5% of the owner-occupier market compared to 13.6% in the September quarter of 2013. The figure is the lowest since the Australian Bureau of Statistics started to collect data on the activity of first home buyers and is also persistently low compared to the long-run average proportion of 19.9%, despite eight interest rate cuts since November 2011…

There is anecdotal evidence that younger Australians are opting for living in rental accommodation or with their parents longer and investing in property rather than becoming first home buyers.

With the removal of assistance (First Home Owner Grant, stamp duty concessions) to first home buyers of established homes in the majority of states and territories, younger Australians may be realising that there are better incentives to becoming investors rather than home owners. For some, this is the only way to get a foot in the door…

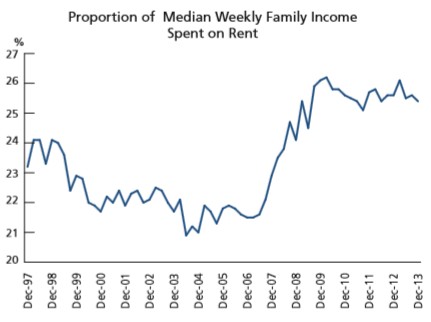

Over the December quarter 2013, rental affordability improved slightly with the proportion of income required to meet rent payments decreasing 0.2 percentage point to 25.4%. Compared to the same quarter of 2012, the difference was identical.

In a welcome development, the REIA has also abandoned earlier calls for demand-side policy measures, such as stamp duty reforms, access to superannuation and first home buyers’ assistance, and instead called to “ease the supply side problems that are putting pressure on housing affordability”.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.