Mid-last year, I wrote an article arguing that Australia’s retail sector must get used to a lower growth future, due to slower growth in household debt and lower income growth as the once-in-a-century commodity price (terms-of-trade) boom unwinds:

There are strong reasons to believe that retail sales growth will remain soft going forward, irrespective of whether the Reserve Bank cuts interest rates further.

First, one of the key drivers of the strong growth in retail sales over the 1990s and 2000s was the inexorable rise in household debt and the run-down of household savings…

Household debt levels stabilised from 2006, whereas household savings rates have returned to long-run historical norms, suggesting that sales growth can only grow in line with disposable incomes going forward.

On this front, the news is also bad for the retail industry… As the terms-of-trade retraces back towards its longer-run average, it will detract from income growth, pulling down consumption and retail sales in the process.

…the prior decade’s retail sales growth was extraordinary, driven by the huge surge in household debt and the once-in-a-century boom in incomes. The situation was unsustainable and the retail industry should not expect growth to return to anywhere near these levels in the decade ahead.

Yesterday, the Reserve Bank of Australia (RBA) released research on The distribution of household spending in Australia, which explained how both overall spending, and spending on goods in particular, declines as households age:

Advertisement

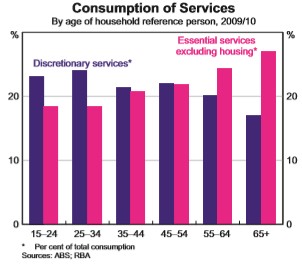

Older households tend to allocate a smaller proportion of their spending to durable goods than do younger households, perhaps because they have already accumulated such goods over their lifetime. On the other hand, older households tend to spend proportionately more on essential services, such as health care, than younger households. In contrast, younger households spend proportionately more on discretionary services such as travel, hotels and restaurants, and recreational services (Graph 3).

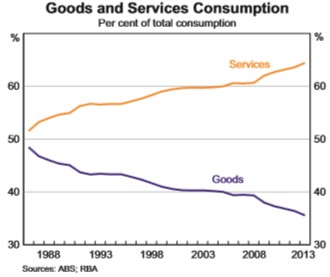

Concentrating first on the distribution of spending across different categories of goods and services, the most prominent trend over recent decades has been the reallocation of nominal spending away from goods (mostly durable) and towards services (mostly dwelling and other essential services, such as education). Between 1986 and 2013, household spending on goods decreased from around half to one-third of total spending, while the share spent on services increased from around half to two-thirds (Graph 5).

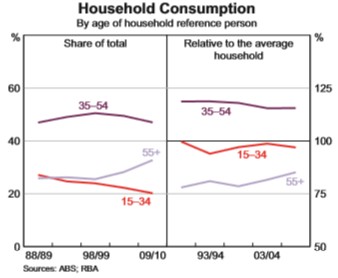

Turning to the distribution of spending across different household types, the data suggest that, on average, older households spend less than other households. For example, in 2009/10 households headed by a person aged 55 years and above consumed goods and services to the value of $57 000 on average, compared with $67 000 for all households, a ratio of around 85 per cent…

The increase in the importance of older households – who tend to spend less on goods and more on services than other households – has contributed to the aggregate shift in consumption away from goods and towards services, although the size of this effect has been small…

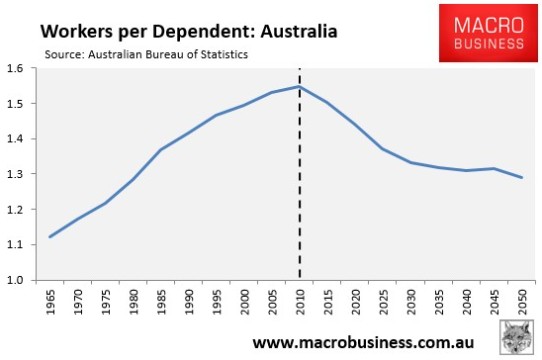

Given that projected shift in Australia’s population towards retirees (see next chart), along with lower debt accumulation and income growth as the commodity boom unwinds, the Australian retail sector is going to find it increasingly difficult to achieve the types of sales and profit growth that it was accustomed to in the 2000s, when all three factors – credit growth, income growth, and demographics – were working in the sector’s favour.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.